Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

The ups and downs of the discounted cash flow method

Discounted cash flow DCF analysis determines the present value of a company or asset based on the value of money it can make in the future. The assumption is that the company or asset is expected to generate cash flows in this time frame. In other words, the value of money today will be worth more in the future. The DCF analysis is also useful in estimating a company’s intrinsic value. This article breaks down the most important DCF Analysis pros & cons.

Using DCF analysis can be advantageous and disadvantageous depending on the situation it is used for. The two succeeding sections discuss the main DCF analysis pros and cons.

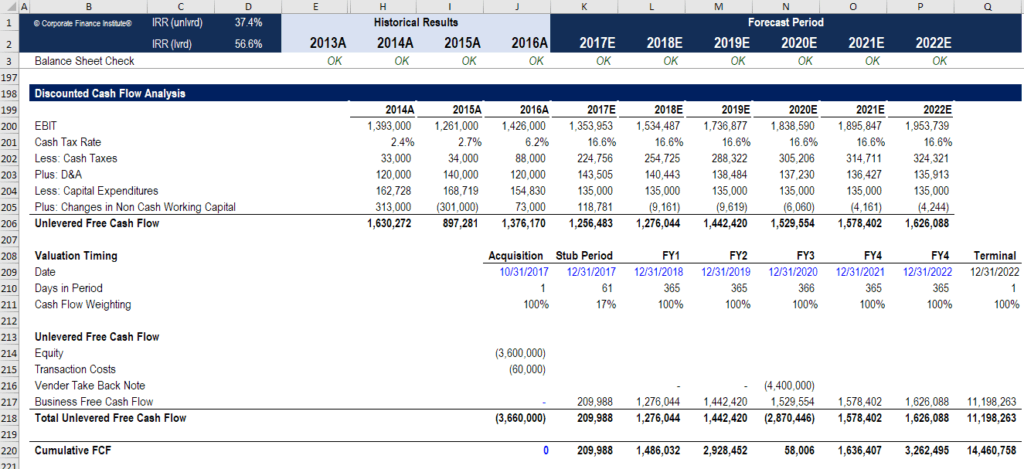

Source: CFI financial modeling courses.

It would be best for a financial analyst to use the DCF analysis if they are confident about the assumptions being made. A discounted cash flow model requires a lot of detail to make an estimate of the intrinsic value of a stock, and each of those details requires an assumption.

Despite the advantages of the DCF analysis, it is also exposed to some disadvantages. The main drawback of DCF analysis is that it’s easily prone to errors, bad assumptions, and overconfidence in knowing what a company is actually “worth”.

A financial analyst should be aware of the advantages and disadvantages of the DCF analysis as mentioned above. It also takes repeated practice for an analyst to become proficient or even skilled at building financial models.

DCF analysis is best used with other tools in order to have a check and balance mechanism to validate the results.

Other valuation methods commonly include:

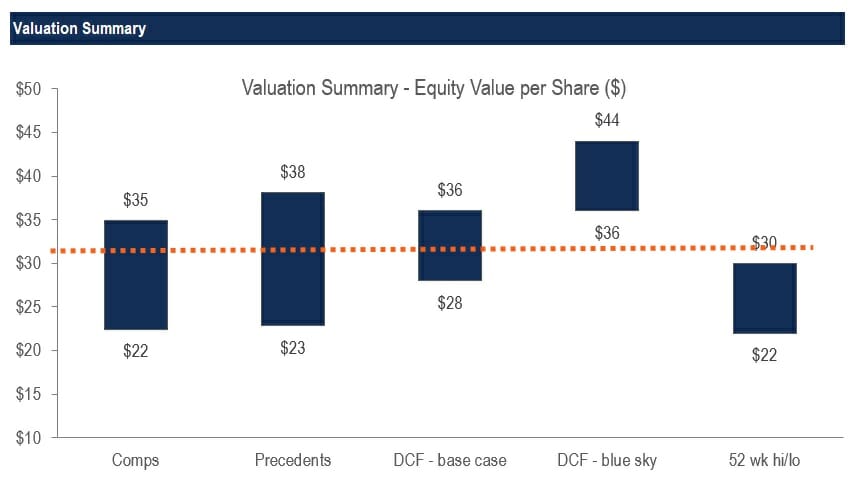

The above methods, combined with a DCF model, can be displayed in a Football Field Chart (as shown below).

To learn how to build a DCF model, launch CFI’s financial modeling courses.

Connect what you just learned to a clear career path with CFI’s role‑based courses and certification programs.

Thank you for reading CFI’s guide to DCF Analysis Pros & Cons. To continue learning about company valuation, check out these valuable resources: