Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

Additional value created above the cost of capital

Economic Value Added (EVA), sometimes known as Economic Profit, is a measure based on the Residual Income technique, which measures the return generated over and above investors’ required rate of return (hurdle rate).

EVA serves as an indicator of the profitability of projects in which a company invests. Its underlying premise consists of the idea that 1) real profitability occurs when additional wealth is created for investors and 2) that projects should generate returns above their cost of capital.

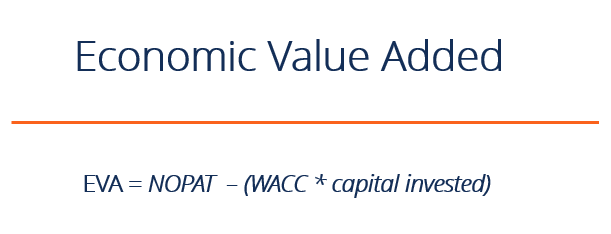

EVA adopts almost the same form as residual income, and the EVA formula can be expressed as follows:

Where:

(WACC * Invested Capital) is also known as the Finance Charge

One key consideration for this item is the adjustment of the cost of debt. The cost of debt is implicitly included in the Finance Charge (WACC * Invested Capital) since WACC includes the cost of debt. Therefore, we need to make sure that we do not deduct interest expense when calculating NOPAT. We can adjust for this in two ways:

When calculating EVA, the typical practice is to make several accounting adjustments. Among the most common and important are:

Cash Taxes = Tax Charge per Income Statement – Increase (or + if Reduction) in Deferred Tax Provision + Tax Benefit of Interest Charge

Finance Charge = WACC * Invested Capital

WACC = [Ke * E / (E+D)] + [Kd * (1-t) * D / (E+D)]

Where: Ke = Cost of Equity and Kd * (1-t) = After-Tax Cost of Debt

Thus, given the adjusted taxes, we can write the economic value-added formula as follows:

When EVA is a positive value, the company is creating value for investors. If EVA is a negative value, the company is destroying value.

The properties of using economic value added can be compared with other approaches in the following table:

| Valuation Model | Measure | Discount Factor | Comments |

|---|---|---|---|

| Enterprise discounted cash flow | Free cash flow | WACC | Works best for projects, business units, and companies that manage their capital structure to a target level |

| Discounted economic profit | EVA | WACC | Explicitly highlights when a company creates value |

| Adjusted present value | Free cash flow | Unlevered cost of equity | Highlights changing capital structure more easily than WACC-based models |

| 2014 | 2015 | 2016 | |

|---|---|---|---|

| Capital invested (beginning of year) | $54,236 | $50,323 | $55,979 |

| WACC | 8.22% | 8.28% | 8.37% |

| Finance Charge | $4,460 | $4,167 | $4,682 |

| NOPAT | $7,265 | $5,356 | $4,336 |

| Finance Charge | $4,460 | $4,169 | $4,683 |

| Economic Value Added | $2,805 | $1,187 | -$347 |

Click the button below to download CFI’s free Economic Value Added template!

Financial analysts typically rely on various methods of measuring value. Return on invested capital (ROIC) is a common method.

Ultimately, the truest measure of value is the cash flow that’s generated by a business, which can be measured by the internal rate of return (IRR). IRR is used in financial modeling and valuation to determine whether a company is creating value in its investments.

If the IRR is greater than the cost of capital, the company is usually adding value. If IRR is less than the cost of capital, the company is destroying value.

Watch this short video to quickly understand the main concepts covered in this guide, including the definition of Economic Value Added, the formula for EVA, and an example of EVA calculation.

Connect what you just learned to a clear career path with CFI’s role‑based courses and certification programs.

In conclusion, economic value added (EVA) highlights when a company creates value (or destroys value) and is helpful in understanding the company’s performance in a given year. For more resources to help advance your corporate finance career as a Financial Modeling & Valuation Analyst (FMVA), these additional resources will be helpful: