Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

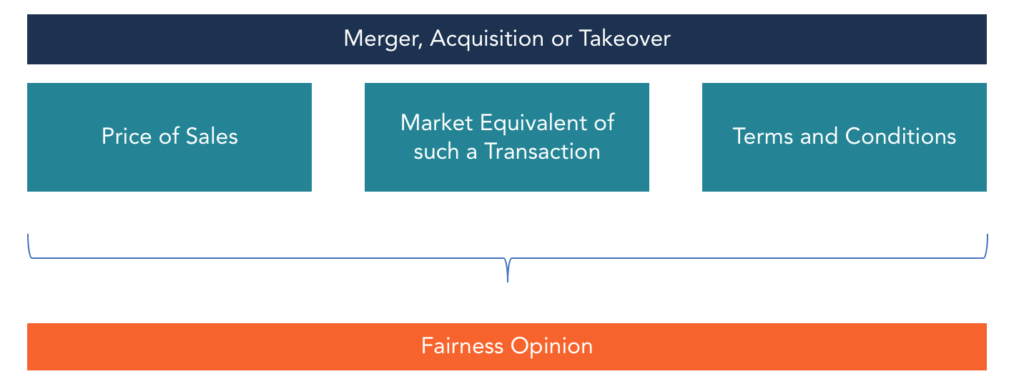

An assessment of the terms of a merger, takeover, or acquisition

A fairness opinion is a report compiled by a qualified investment banker or advisor that evaluates the fairness of the price offered during an acquisition, takeover, or merger. The opinion relates to the price offered by the buyer and the fairness of the terms to the company’s shareholders. It is used in both friendly and hostile transactions. During a friendly deal, the opinion is typically in favor of the transaction, however, during a hostile takeover or unsolicited bid to acquire all or part of a company, the directors often try to convince shareholders not to accept the offer with an inadequacy opinion.

The fairness opinion helps in decision-making, enhancing communication, and mitigating any risks that may arise after a deal. It also provides a defense in a court of law should a shareholder or any other stakeholder file a lawsuit against the company’s directors – either for accepting, or rejecting, a bid offer.

In preparing a fairness opinion, the investment advisors must look at the price, the terms of the sale, and the consideration to be received vis-a-vis the market rate for a similar transaction. When reviewing transactions, analysts try to look at the terms from the perspective of the company’s investors. The report is prepared late in the negotiations between the seller and the buyer when there is a high likelihood of the transaction being concluded. If the report was prepared before the two parties agreed to the terms, the transaction might be canceled midway, and the report would be of no importance.

The directors of a company have a fiduciary responsibility to shareholders, which is known as the business judgment rule. The rule requires that the management must represent the shareholders in good faith, like a reasonable person who is responsible for supervising the affairs of the business. Since shareholders do not take part in the day-to-day running of the business, the directors are responsible for overseeing the affairs of the company. The fairness opinion aims to demonstrate to the shareholders that the management or directors acted in the shareholders’ best interest and that a report by independent advisors hired by the company confirms that the terms were fair (or not, if the offer is being rejected). In the absence of a fairness opinion, there may be a section of shareholders who are dissatisfied with the value agreed upon by the seller and the buyer.

Some shareholders may seek information as to whether there were other alternatives to the deal, how the transaction could’ve achieved better terms, etc. An opinion prepared by a qualified advisor can help alleviate such concerns by affirming that the price is a fair valuation. In a situation where dissatisfied shareholders file a lawsuit against the company, the directors of the company can use the fair opinion report to show that they acted in good faith during the transaction.

These are some concerns that arise in the preparation of fair opinion reports. The first concern is the cost charged for the service by investment advisors. Since the report is prepared while negotiations between the buyer and the seller are ongoing, the advisor is under considerable time pressure to complete the fairness opinion. Also, the preparation requires a high level of skill to identify any areas in the agreement that require the attention of the stakeholders. The advisors charge a premium price for their services to compensate for the limited time (usually under a week), skills required, and the risk involved. The report may be used in a court of law and, therefore, the analyst must provide a high degree of accuracy and attention to detail. The opinion fee may run into six or seven figures, depending on the company.

Another concern in regard to the fairness opinion may arise when the work of preparing the report is assigned to an investment bank that is also involved in the acquisition transaction. Some critics say that the investment bank will be entangled in a conflict of interest since it receives payments from the opinion fee work as well as from facilitating the sale of the business. The investment bank must strike a balance in order to give a fair opinion on whether the price agreed upon is a fair amount for the shareholders of the company and also fair for the buyer. If a person or entity rendering an opinion stands to benefit from the transaction directly or indirectly, they should make such disclosures in the report.

When developing a fairness opinion, independent advisors must conduct due diligence to ensure that all the necessary information required in reaching a conclusion has been obtained. They achieve this by visiting the business premises of the selling company and reviewing documentation that will help in developing an opinion about the value of the selling company. They should examine the dividend-paying history and capacity of the company, past financial performance, factors affecting revenues, and the considerations for similar transactions. The advisors should also review the merger or acquisition agreement and its terms.

The due diligence should not be limited to the selling company alone. The advisors should perform a similar exercise in regard to the buying company. If the buyer is a publicly-traded company, the advisors should review their financial reports, past acquisitions and mergers, and any recent public disclosure documents. The advisors should also reach out to other advisors who have dealt with the company to get necessary information that may be material to the transaction.

Once the advisors have completed the review and compiled a report on their opinion, the report is forwarded to the directors for consideration. The management discussions of each factor indicated in the fairness report are summarized in a fairness memorandum. The advisors may participate in these discussions and respond to any concerns or questions that the management may have concerning the report.

In 2016, Monsanto retained Morgan Stanley to be its financial advisor for the proposed $66 billion merger with Bayer. Morgan Stanley determined that, based on the assumptions made, valuation methods used, and facts and information considered, the cash offer of $128.00 per share made to shareholders was a fair offer.

Read the full fairness opinion filed with the SEC.

It was reported that Morgan Stanley earned $120 million in fees for acting as Monsanto’s advisor in this transaction. That price tag should give you an idea of how important a fairness opinion is considered to be.

CFI is a leading provider of financial modeling courses for investment banking professionals. To help you advance your career, check out the additional CFI resources below: