Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

Download our free Investment Banking Pitchbook Template

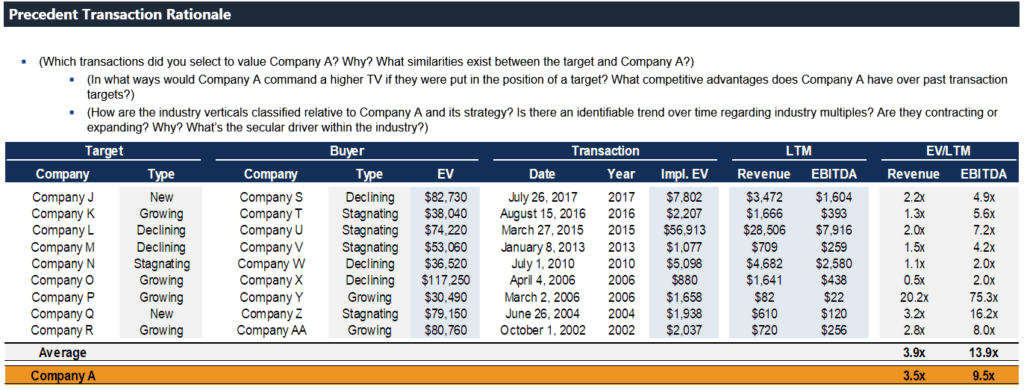

Precedent Transactions Analysis is based on the premise that a company’s valuation can be assessed using the prices paid by acquirers of companies that are similar to the client company. The method is similar to the comparable company’s valuation method in that both are relative valuation methods whereby the target valuation is a product of a market multiple and your company’s selected financial or operating metric.

The key difference is that a total deal value (TV) multiple is used instead of enterprise value multiple as done in the comparable companies analysis. The implication here is that deals will often involve control premiums that inflate the valuation of the target companies. It generally results in a valuation range that is higher than those of intrinsic and public comparables valuation methods.

Download CFI’s customizable template to create your own professional presentations.

Finding a perfect comparable company is rare, and logically, finding a precedent transaction involving a perfect comparable company is even rarer. Much in the same way as we would select peers for a comparable spread, we employ a top-down approach to screen for transactions.

First, we must identify the relevant industry and sub-industries that apply to the company we are trying to value. Second, we want to identify the size of the deal, which is analogous to selecting similar-sized companies for the comparables analysis. Then, we must consider additional factors that will influence our selection of transactions, such as the deal type, buyer characteristics, strategic rationale for the transaction, and financing mix. And lastly, it is best practice to screen for the timing of the deal, as more recent transactions contain the most relevant information regarding underlying economic conditions and serves as a better proxy for current valuations compared to older transactions.

The standard in investment banking is to utilize only public announcement data to determine the value of the transaction. Therefore, we use the purchase price as of the announcement date rather than the closing date. The valuation as of the announcement date reflects the financial and operating information available to the acquirer when it makes the decision to purchase.

When considering the financing mix, if any share consideration is used in the offer price, it is industry best practice to use the acquirer’s closing share price one day prior to the announcement date. In press releases documenting the details of an acquisition, if stock consideration is used, the company will release the share exchange ratio that should be used in the transaction. We multiply this share exchange ratio by the day prior’s closing stock price of the acquirer to find the value of the total stock consideration.

The target’s equity value is calculated with the target’s diluted shares outstanding as of the announcement date. When accounting for dilution, the industry standard is to use total options outstanding, and not the options exercisable. Diluted shares outstanding is equal to the product of basic shares outstanding and offer price per share, then adding the product of the target’s options/warrants outstanding and the difference between the offer price per share and the exercise prices.

The transaction multiples that investment bankers typically use are implied enterprise value as a multiple of sales, EBITDA, EBIT or market/book value of equity as a multiple of net income (P/E or P/B). Following the same logic, as we saw in the comparable companies analysis, there may be certain industry-specific multiples that are more appropriate to use, such as P/NAV or P/DACF in the natural resources industries.

Finding the pertinent data for comparable companies is relatively easy, but screening for past transactions is significantly more complicated. A web-based platform such as Bloomberg, Pitchbook, SDC, CapIQ, or FactSet speeds up the screening process, but transaction information can be found in public company documents as well. Company press releases, Form S-4 (merger proxies), Form 8-K, and various trade publications will contain the information needed to perform a precedent transactions analysis. In the investment banking industry, it is best practice to not only become familiar with the web-based tools at your disposal but also to maintain a record of all transactions related to your industry group in a living document for future use.

Thank you for downloading CFI’s free pitchbook template. To keep learning and advancing your career, the following resources will be helpful:

Below is a break down of subject weightings in the FMVA® financial analyst program. As you can see there is a heavy focus on financial modeling, finance, Excel, business valuation, budgeting/forecasting, PowerPoint presentations, accounting and business strategy.

A well rounded financial analyst possesses all of the above skills!

CFI is the global institution behind the financial modeling and valuation analyst FMVA® Designation. CFI is on a mission to enable anyone to be a great financial analyst and have a great career path. In order to help you advance your career, CFI has compiled many resources to assist you along the path.

In order to become a great financial analyst, here are some more questions and answers for you to discover: