Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

What is a Risk-Free Rate and why is it important?

The risk-free rate of return is the interest rate an investor can expect to earn on an investment that carries zero risk. In practice, the risk-free rate is commonly considered to be equal to the interest paid on a 10-year highly rated government Treasury note, generally the safest investment an investor can make.

The risk-free rate is a theoretical number since technically all investments carry some form of risk, as explained here. Nonetheless, it is common practice to refer to the T-note rate as the risk-free rate. While it is possible for a highly rated government to default on its securities, the probability of this happening is considered very low.

The security with the risk-free rate may differ from investor to investor. The general rule of thumb is to consider the most stable government body offering T-notes in a certain currency. For example, an investor investing in securities that trade in USD should use the U.S. T-note rate, whereas an investor investing in securities traded in Euros or Francs should use the equivalent Swiss or German note.

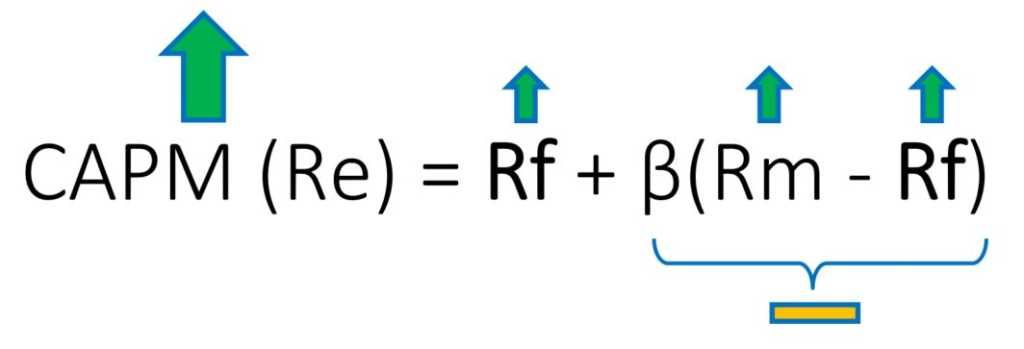

The risk-free rate is used in the calculation of the cost of equity (as calculated using the CAPM), which influences a business’s weighted average cost of capital. The graphic below illustrates how changes in the risk-free rate can affect a business’ cost of equity:

Where:

CAPM (Re) – Cost of Equity

Rf – Risk-Free Rate

β – Beta

Rm – Market Risk Premium

A rise in Rf will pressure the market risk premium to increase. This is because as investors are able to get a higher risk-free return, riskier assets will need to perform better than before in order to meet investors’ new standards for required returns. In other words, investors will perceive other securities as relatively higher risk compared to the risk-free rate. Thus, they will demand a higher rate of return to compensate them for the higher risk.

Assuming the market risk premium rises by the same amount as the risk-free rate does, the second term in the CAPM equation will remain the same. However, the first term will increase, thus increasing CAPM. The chain reaction would occur in the opposite direction if risk-free rates were to decrease.

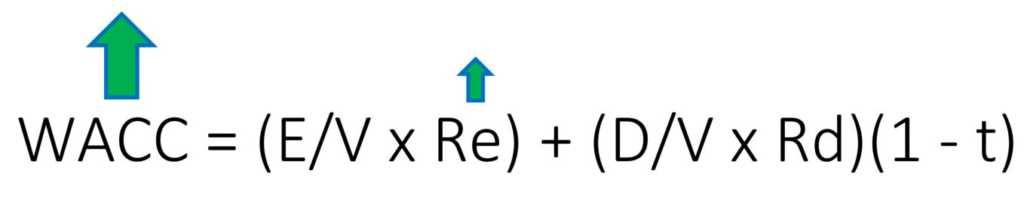

Here’s how the increase in Re would increase WACC:

Holding the business’ cost of debt, capital structure, and tax rate the same, we see that WACC would increase. The opposite is also true (i.e., a decreasing Re would cause WACC to decrease).

From a business’s perspective, rising risk-free rates can be problematic. The company might have to adjust its internal investment policies to meet higher required rates of return demanded by investors.

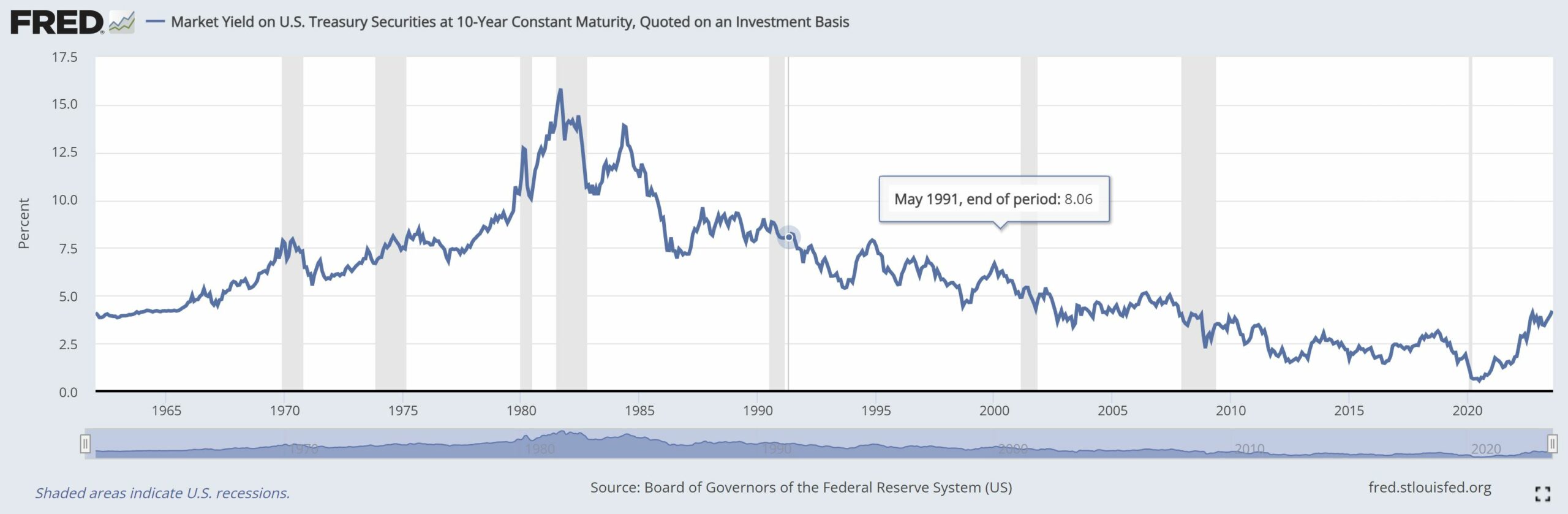

Below is a chart of historical U.S. 10-year T-note rates:

Source: St. Louis Fed

T-notes fell as low as 0.52% during the Covid pandemic and rose as high as 15.84% during the early 1980s. High T-notes rates usually signal prosperous economic times when private sector companies are performing well, meeting earnings targets, and increasing stock prices over time.

Thank you for reading CFI’s guide on Risk-Free Rate. To learn more about related topics, check out the following CFI resources:

CFI is a global provider of financial modeling courses and of the FMVA Certification. CFI’s mission is to help all professionals improve their technical skills. If you are a student or looking for a career change, the CFI website has many free resources to help you jumpstart your Career in Finance. If you are seeking to improve your technical skills, check out some of our most popular courses. Below are some additional resources for you to further explore:

CFI is a global provider of financial modeling courses and of the FMVA Certification. CFI’s mission is to help all professionals improve their technical skills. If you are a student or looking for a career change, the CFI website has many free resources to help you jumpstart your Career in Finance. If you are seeking to improve your technical skills, check out some of our most popular courses. Below are some additional resources for you to further explore:

Below is a break down of subject weightings in the FMVA® financial analyst program. As you can see there is a heavy focus on financial modeling, finance, Excel, business valuation, budgeting/forecasting, PowerPoint presentations, accounting and business strategy.

A well rounded financial analyst possesses all of the above skills!

CFI is the global institution behind the financial modeling and valuation analyst FMVA® Designation. CFI is on a mission to enable anyone to be a great financial analyst and have a great career path. In order to help you advance your career, CFI has compiled many resources to assist you along the path.

In order to become a great financial analyst, here are some more questions and answers for you to discover: