Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

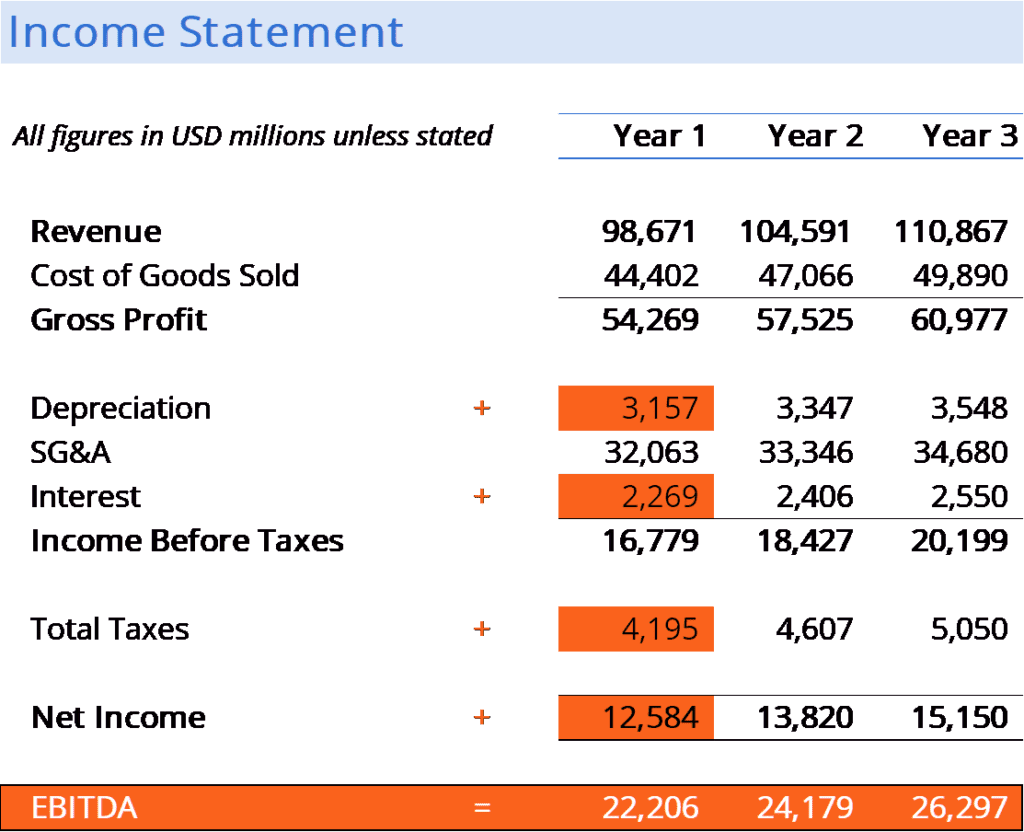

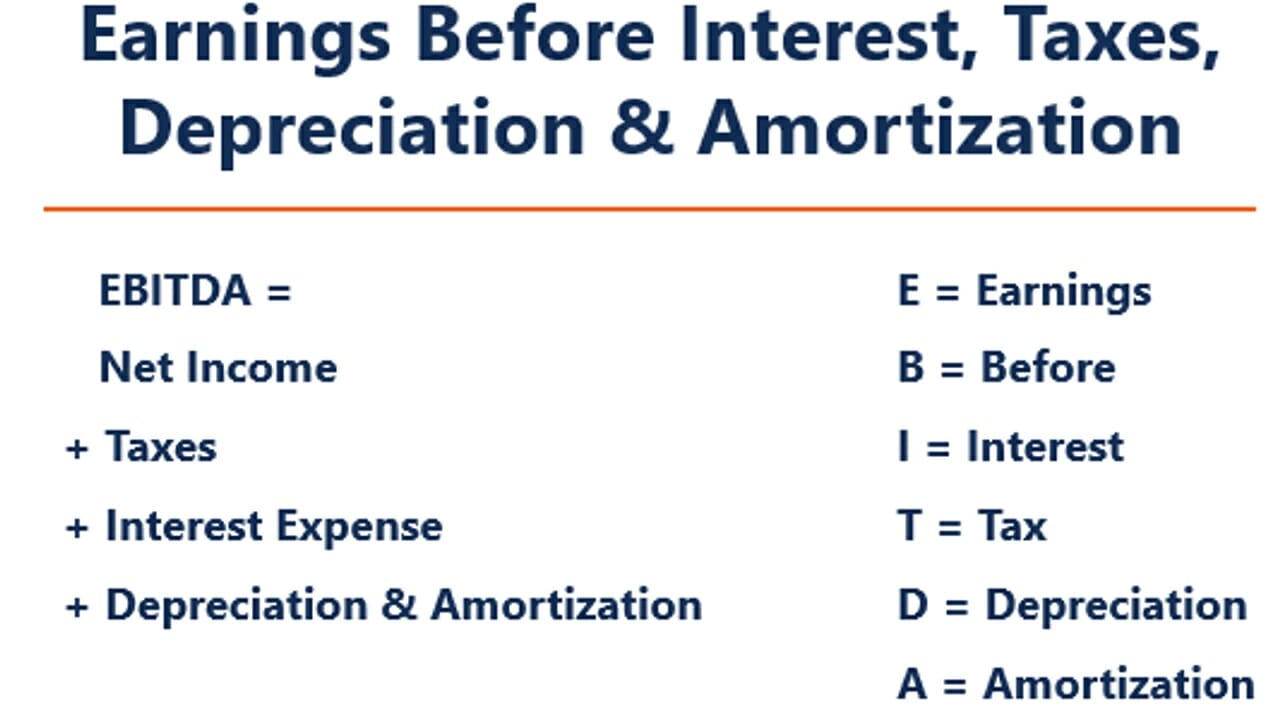

Earnings Before Interest, Tax, Depreciation and Amortization

EBITDA stands for Earnings Before Interest, Taxes, Depreciation, and Amortization and is a metric used to evaluate a company’s operating performance. It can be seen as a loose proxy for cash flow from the entire company’s operations.

The EBITDA metric is a variation of operating income (EBIT) that excludes certain non-cash expenses. The purpose of these deductions is to remove the factors that business owners have discretion over, such as debt financing, capital structure, methods of depreciation, and taxes (to some extent). It can be used to showcase a firm’s financial performance without the impact of its capital structure.

EBITDA is not a recognized metric in use by IFRS or US GAAP. In fact, certain investors like Warren Buffet have a particular disdain for this metric, as it does not account for the depreciation of a company’s assets.

For example, if a company has a large amount of depreciable equipment (and thus a high amount of depreciation expense), then the cost of maintaining and sustaining these capital assets is not captured.

Here is the formula for calculating EBITDA:

EBITDA = Net Income + Interest + Taxes + Depreciation + Amortization

or

EBITDA = Operating Profit + Depreciation + Amortization

Below is an explanation of each component of the formula:

Interest expense is excluded from EBITDA, as this expense depends on the financing structure of a company. Interest expense comes from the money a company has borrowed to fund its business activities.

Different companies have different capital structures, resulting in different interest expenses. Hence, it is easier to compare the relative performance of companies by adding back interest and ignoring the impact of capital structure on the business. Note that interest payments are tax-deductible, meaning corporations can take advantage of this benefit in what is called a corporate tax shield.

Taxes vary and depend on the region where the business is operating. They are a function of a jurisdiction’s tax rules, which are not really part of assessing a management team’s performance, and, thus, many financial analysts prefer to add them back when comparing businesses.

Depreciation and amortization (D&A) depend on the historical investments the company has made and not on the current operating performance of the business. Companies invest in long-term fixed assets (such as buildings or vehicles) that lose value due to wear and tear.

The depreciation expense is based on a portion of the company’s tangible fixed assets deteriorating over time. Amortization expense is incurred if the asset is intangible. Intangible assets such as patents are amortized because they have a limited useful life (competitive protection) before expiration.

D&A is heavily influenced by assumptions regarding useful economic life, salvage value, and the depreciation method used. Because of this, analysts may find that operating income is different than what they think the number should be, and therefore, D&A is backed out of the EBITDA calculation.

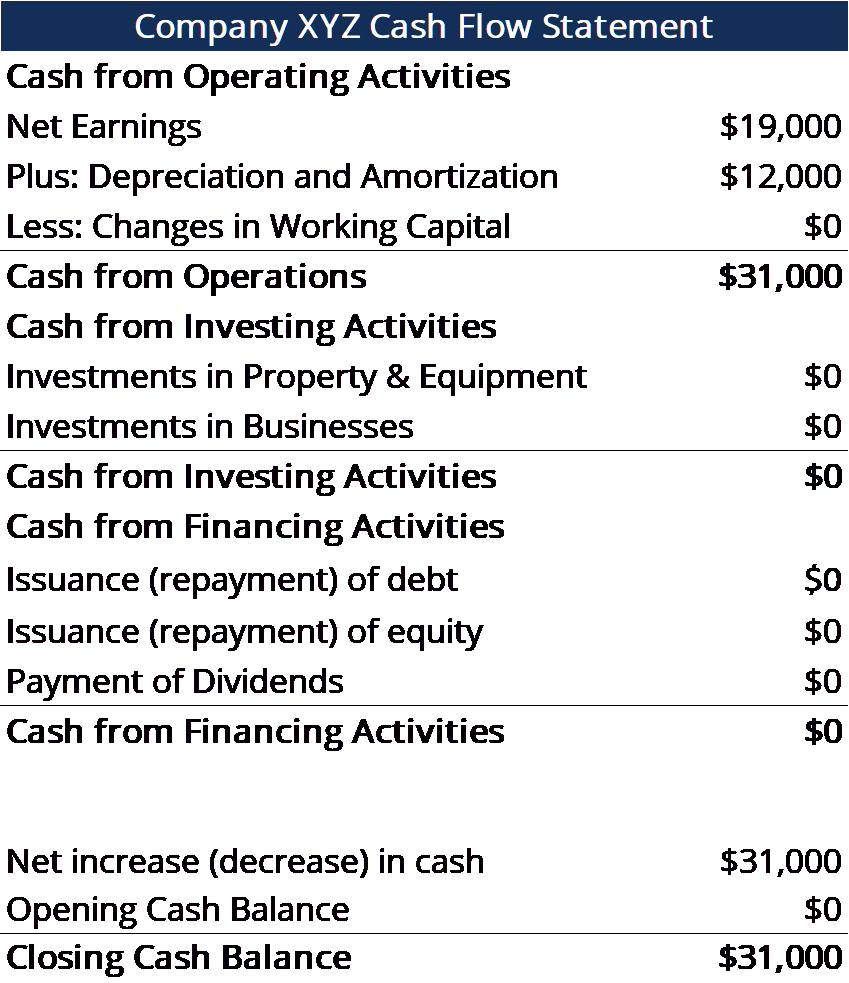

The D&A expense can be located in the firm’s cash flow statement under the cash from operating activities section. Since depreciation and amortization is a non-cash expense, it is added back (the expense is usually a positive number for this reason) while on the cash flow statement.

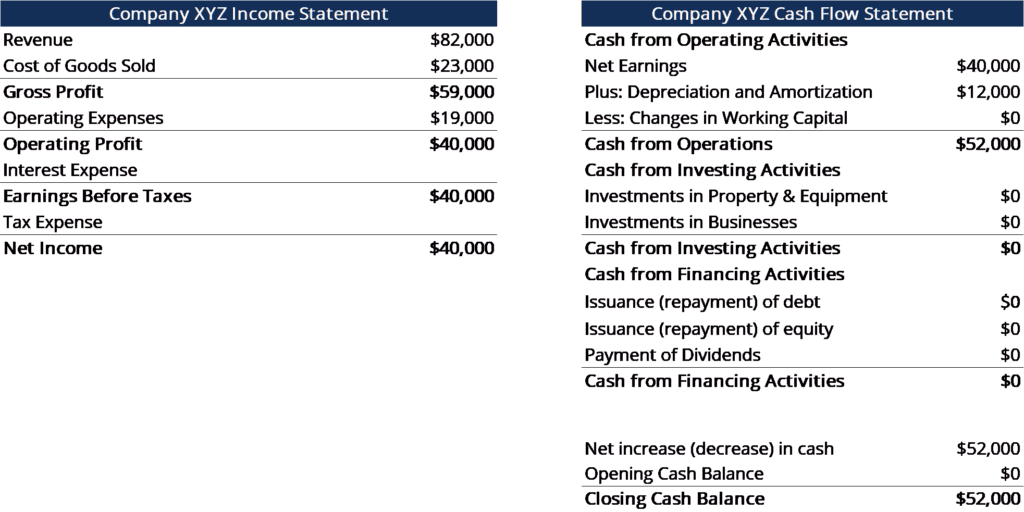

Example: The depreciation and amortization expense for XYZ is $12,000.

The EBITDA metric is commonly used as a loose proxy for cash flow. It can give an analyst a quick estimate of the value of the company, as well as a valuation range by multiplying it by a valuation multiple obtained from equity research reports, publicly traded peers, and industry transactions, or M&A.

In addition, when a company is not making a net profit, investors can turn to EBITDA to evaluate a company. Many private equity firms use this metric because it is very good for comparing similar companies in the same industry. Business owners use it to compare their performance against their competitors.

EBITDA is not recognized by GAAP or IFRS. Some are skeptical (like Warren Buffett) of using it because it presents the company as if it has never paid any interest or taxes, and it shows assets as having never lost their natural value over time (no depreciation or capital expenditures are deducted).

For example, a fast-growing manufacturing company may present increasing sales and EBITDA year-over-year (YoY). To expand rapidly, it acquired many fixed assets over time and all were funded with debt. Although it may seem that the company has strong top-line growth, investors should look at other metrics as well, such as capital expenditures, cash flow, and net income.

Below is a short video tutorial on Earnings Before Interest, Taxes, Depreciation, and Amortization. The short lesson will cover various ways to calculate it and provide some simple examples to work through.

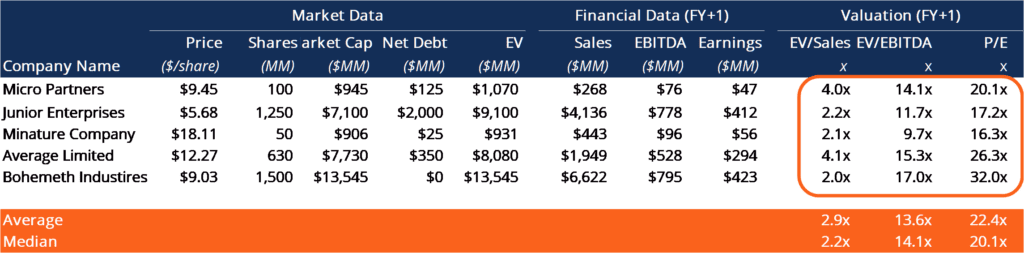

When comparing two companies, the Enterprise Value/EBITDA ratio can be used to give investors a general idea of whether a company is overvalued (high ratio) or undervalued (low ratio). It’s important to compare companies that are similar in nature (same industry, operations, customers, margins, growth rate, etc.), as different industries have vastly different average ratios (high ratios for high-growth industries, low ratios for low-growth industries).

The metric is widely used in business valuation and is found by dividing a company’s enterprise value by EBITDA.

Company ABC and Company XYZ are competing grocery stores that operate in New York. ABC has an enterprise value of $200M and an EBITDA of $10M, while firm XYZ has an enterprise value of $300M and an EBITDA of $30M. Which company is undervalued on an EV/EBITDA basis?

Company ABC: Company XYZ:

EV = $200M EV = $300M

EBITDA = $10M EBITDA = $30M

EV/EBITDA = $200M/$10M = 20x EV/EBITDA = $300M/$30M = 10x

On an EV/EBITDA basis, company XYZ is undervalued because it has a lower ratio.

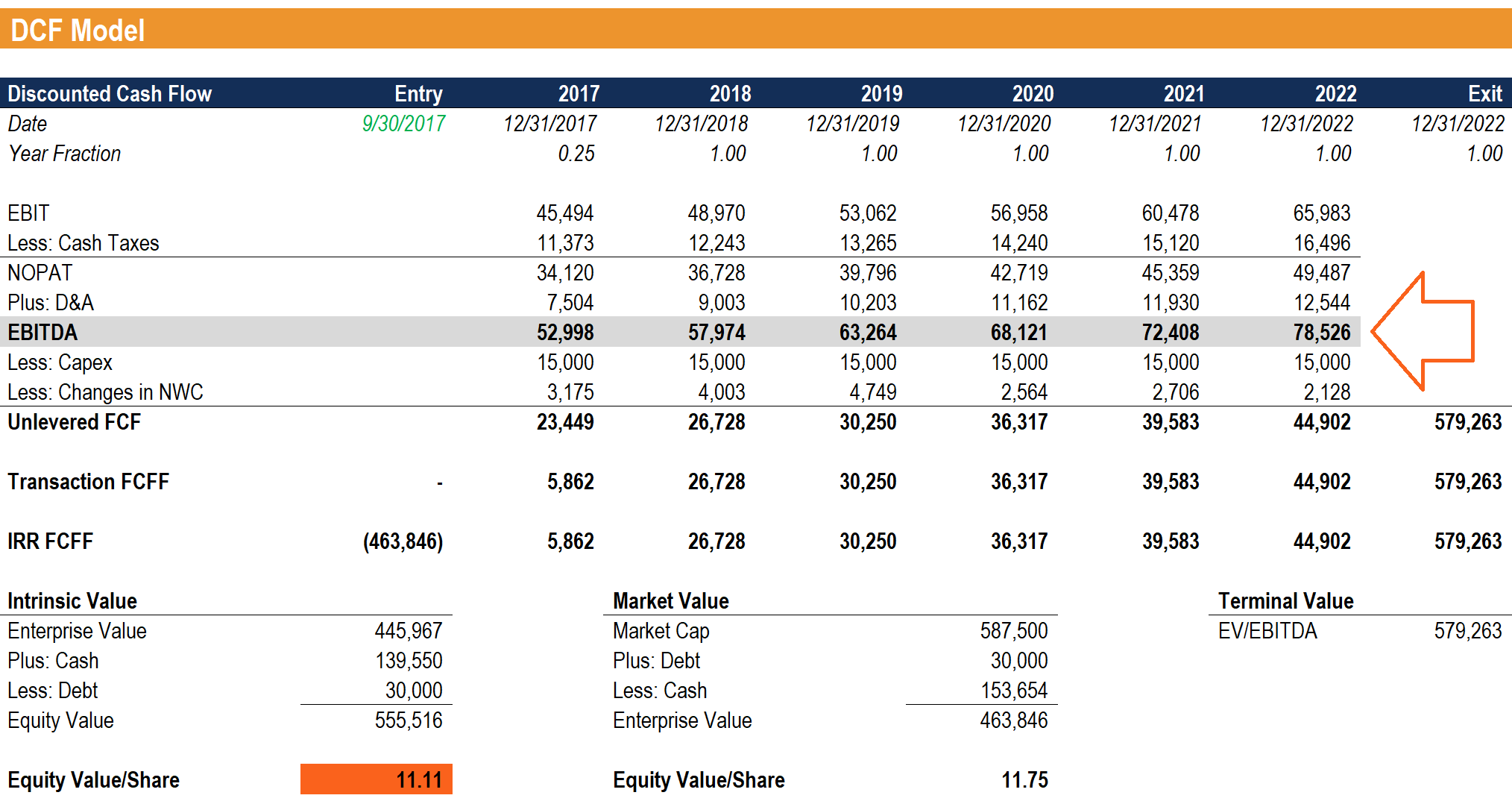

EBITDA is used frequently in financial modeling as a starting point for calculating unlevered free cash flow. Earnings before interest, taxes, depreciation, and amortization is such a frequently referenced metric in finance that it’s helpful to use it as a reference point, even though a discounted cash flow (DCF) model only values the business based on its free cash flow.

Image: CFI’s Video-based financial modeling courses.

Company XYZ accounts for their $12,000 depreciation and amortization expense as a part of their operating expenses. Calculate their Earnings Before Interest Taxes Depreciation and Amortization:

EBITDA = Net Income + Tax Expense + Interest Expense + Depreciation & Amortization Expense

= $19,000 + $19,000 + $2,000 + $12,000

= $52,000

EBITDA = Revenue – Cost of Goods Sold – Operating Expenses + Depreciation & Amortization Expense

= $82,000 – $23,000 – $19,000 + $12,000

= $52,000

Download CFI’s free Excel template now to advance your finance knowledge and perform better financial analysis.

Company XYZ’s depreciation and amortization expense are incurred from using its machine that packages the candy the company sells. It pays 5% interest to debtholders and has a tax rate of 50%. What is XYZ’s Earnings Before Interest Taxes Depreciation and Amortization?

Interest expense = 5% * $40,000 (operating profit) = $2,000

Earnings Before Taxes = $40,000 (operating profit) – $2,000 (interest expense) = $38,000

Tax Expense = $38,000 (earnings before taxes) * 50% = $19,000

Net Income = $38,000 (earnings before taxes) – $19,000 (tax expense) = $19,000

Second Step: Find the depreciation and amortization expense

In the Statement of Cash Flows, the expense is listed as $12,000.

Since the expense is attributed to the machines that package the company’s candy (the depreciating asset directly helps with producing inventory), the expense will be a part of their cost of goods sold (COGS).

Third Step: Calculate Earnings Before Interest Taxes Depreciation and Amortization

EBITDA = Net Income + Tax Expense + Interest Expense + Depreciation & Amortization Expense

= $19,000 + $19,000 + $2,000 + $12,000

= $52,000

EBITDA = Revenue – Cost of Goods Sold – Operating Expenses + Depreciation & Amortization Expense

= $82,000 – $23,000 – $19,000 + $12,000

= $52,000

We hope this has been a helpful guide to EBITDA – Earnings Before Interest Taxes Depreciation and Amortization. If you are looking for a career in corporate finance, this is a metric you’ll hear a lot about. To keep learning more, we highly recommend these additional CFI resources: