Get Certified for

Commercial Banking (CBCA®)

Stand out and gain a competitive edge as a commercial banker, loan officer, or credit analyst with advanced knowledge, real-world analysis skills, and career confidence.

A financial metric that indicates how a company can potentially settle its debts by selling its tangible assets

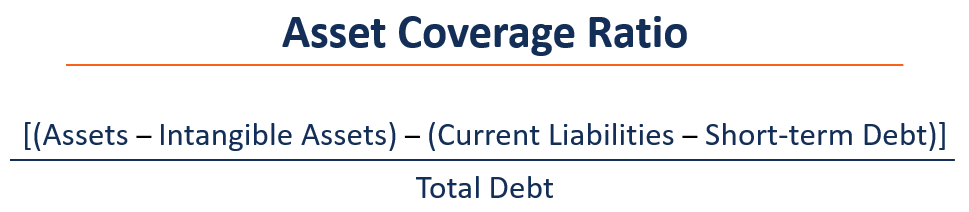

The asset coverage ratio is a financial metric that indicates how a company can potentially settle its debts by selling its tangible assets. The ratio is used to evaluate the solvency of a company and helps lenders, investors, management, regulatory bodies, etc. determine how risky a particular company is. The asset coverage ratio is calculated as follows:

The higher the asset coverage ratio is, the lower the risk of the evaluated company. The ratio can be used in comparable company analysis to compare companies within the same industry.

Going back to the formula above, the first portion of the numerator is assets less intangible assets, and it refers to physical assets and excludes non-physical assets such as franchises, trademarks, copyrights, goodwill, securities, contracts, and patents. The reason for leaving intangible assets out is that they cannot be easily valued or sold.

The second portion of the numerator is current liabilities less short-term debt. Current liabilities are short-term financial obligations that are typically owed to suppliers but are not considered debt since they are not interest-bearing liabilities. The reason for leaving short-term debt out of the numerator is that short-term debt is included in total debt in the denominator.

The denominator includes total debt, which includes both short-term and long-term interest-bearing debt.

Assets are funded with two main sources of capital: debt and equity. Debt investors need to be paid interest and principal on a scheduled basis. Equity investors are the owners of the company and receive residual earnings after debt holders are paid.

Companies funded with less equity and more debt can achieve higher returns on equity due to fewer claimants on earnings. However, high debt levels lead to increased agency risk and bankruptcy risk.

Agency risk involves the conflict of interest between equity holders and debt holders. Management is obligated to act in the best interest of equity holders, and what is in the best interest of equity holders may not always be optimal for debt holders.

Bankruptcy risk is the risk that a company will not be able to meet its debt obligations and will be forced to liquidate assets or sell some assets in order to meet the obligations. It usually occurs because a company is unprofitable or with poorly managed capital.

Companies funded with less debt and more equity face reduced bankruptcy risk, but also provide a lower return to individual equity holders since earnings are spread out between more equity claimants.

The asset coverage ratio is very useful to determine how exposed a company is to the risk of bankruptcy. The asset coverage ratio is a solvency ratio – which means it measures the ability to cover debt obligations in the future.

Investors, debtholders, analysts, and other stakeholders use the asset coverage ratio to assess the financial stability, capital management, overall capital structure, and level of risk of a company. A high ratio from an investor or debtholder’s perspective is beneficial because it shows that the assets are greater than debt liabilities, and that the company is less exposed to bankruptcy risk.

On the other hand, a company does not want the ratio to be too high, since it may indicate that it is not taking on enough debt and are not maximizing the returns to shareholders.

There is no optimal asset coverage ratio. The ratio should be used in context; it should be compared to relevant comparable companies and evaluated on a case-by-case basis.

The asset coverage ratio is useful for quickly evaluating the solvency of a company. However, it comes with the following limitations:

The asset coverage ratio can be used to compare companies and their associated riskiness. However, companies in different industries or at different stages of their lifecycle may adopt drastically different capital structures that make a comparison not feasible.

The components of the asset coverage ratio are items from the balance sheet of a company. In most cases, the items are measured at book value and may not reflect the actual current market value or liquidation value of these items.

The market value or liquidation value may be either higher or lower than what the book value indicates. In the event of liquidation, assets are usually worth less than they normally would be, since they need to be disposed of immediately. Thus, the asset coverage ratio may not be entirely accurate.

Connect what you just learned to a clear career path with CFI’s role‑based courses and certification programs.

CFI offers the Commercial Banking & Credit Analyst (CBCA)™ certification program for those looking to take their careers to the next level. To keep learning and advancing your career, the following resources will be helpful: