Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

The process of writing off acquisition costs over the tenure of the contract

In the insurance industry, deferred acquisition costs are the accumulated costs of acquiring new insurance contracts and amortizing them over the duration of the contracts. The portion of unrecoverable costs from premium receipts is capitalized as intangible assets on the balance sheet. Amortizing over the contract term aligns with GAAP’s matching principle.

Insurance companies incur expenditures to acquire new clients or to renew a particular contract. These costs include commissions paid to brokers and underwriters, underwriting costs, and costs of issuing the policy. They are known as acquisition costs since they are incurred by the company while acquiring new business.

Often, acquisition costs exceed the insurance company’s revenues through the premium received in the first year. The Federal Accounting Standards Board (FASB) allows insurance companies to write off acquisition costs over the duration of the contract, instead of all at once. The FASB is the organization that establishes rules for accounting and financial reporting for companies and non-profit entities in the U.S.

The organization setting a country’s accounting standards establishes certain principles on the accounting of economic transactions. The principles are known as Financial Accounting Standards (FAS). The FAS classifies financial and insurance products based on their tenure and terms. The accounting treatment of DACs associated with each of the classes of products is different.

The FAS classifies insurance products in the following categories:

The FAS-60 category includes short-duration and long-duration contracts. The FAS 60 short-duration contract includes insurance covers for a specific short duration, the provisions of which can be adjusted by the user. An example is property insurance.

The FAS 60 long-duration contract extends over a longer period of time, and the user cannot adjust its provisions. Some examples are endowment contracts, title insurance contracts, and annuity contracts.

The FAS 97 category includes long-term insurance policies that were not covered under FAS 60. The contracts are termed as universal life-type insurance contracts. They are similar to term-life policies but are more flexible since they allow adjustment of their provisions. Most of the contracts developed and gained popularity after the FAS 60 standards were established.

The FAS 120 category extends the accounting practices associated with FAS 60 and FAS 97 contracts to mutual life insurance enterprises. Policyholders own the enterprises; that is, the latter nominate and elect the board of directors. All profits are shared among the policyholders in a predetermined ratio.

The FASB sets distinct rules on accounting for DACs for each of the above categories. The differences depend on the proportion of commissions that can be capitalized and the estimation of future cash flows. However, the basic accounting treatment of DACs is similar across all categories.

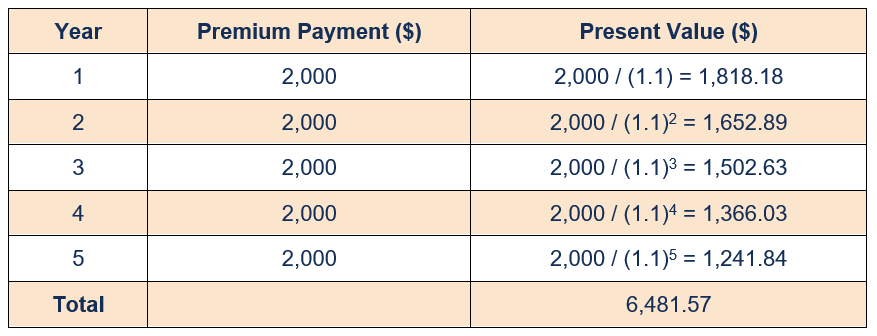

The working principle of the contract requires insurance companies to ensure that the present value of all future premium payments must be equal to the present value of all acquisition costs. It can be understood through the following simplified example.

Consider an insurance policy where the policyholder pays a yearly premium of $2,000 for the next five years. The annual market interest rate is 10%. The present value of all premium payments is computed in the following manner:

For the acquisition cost to be recoverable, its value must be less than $6,481.57. Assume the acquisition cost for the insurance company is $5,000. Then, the amount can be written off throughout the policy, that is, five years. The part of the cost not written off will be recorded as an asset in the balance sheet.

CFI offers the Financial Modeling & Valuation Analyst (FMVA®) certification program for those looking to take their careers to the next level. To keep learning and advancing your career, the following resources will be helpful:

Below is a break down of subject weightings in the FMVA® financial analyst program. As you can see there is a heavy focus on financial modeling, finance, Excel, business valuation, budgeting/forecasting, PowerPoint presentations, accounting and business strategy.

A well rounded financial analyst possesses all of the above skills!

CFI is the global institution behind the financial modeling and valuation analyst FMVA® Designation. CFI is on a mission to enable anyone to be a great financial analyst and have a great career path. In order to help you advance your career, CFI has compiled many resources to assist you along the path.

In order to become a great financial analyst, here are some more questions and answers for you to discover: