Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

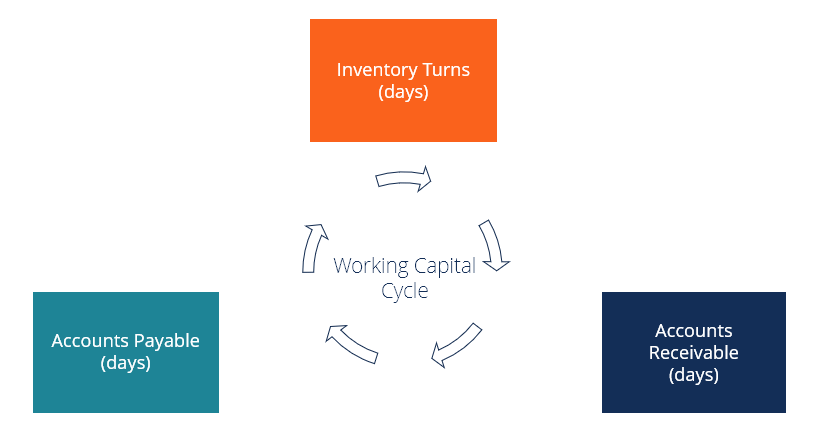

The length of time to convert net working capital into cash

The working capital cycle for a business is the length of time it takes to convert the total net working capital (current assets less current liabilities) into cash. Businesses typically try to manage this cycle by selling inventory quickly, collecting revenue from customers quickly, and paying bills slowly to optimize cash flow.

For most companies, the working capital cycle works as follows:

In the first step of the process, the company gets the materials it needs to produce inventory but doesn’t initially dispense any cash (purchased on credit under accounts payable). In 90 days’ time, it will have to pay for those materials.

Eighty-five (85) days after buying the materials, the finished goods are made and sold, but the company doesn’t receive cash for them immediately, as they are sold on credit (recorded under accounts receivable). Twenty (20) days after selling the goods, the company receives cash, and the working capital cycle is complete.

Based on the above steps, we can see that the working capital cycle formula is:

![]()

Now that we know the steps in the cycle and the formula, let’s calculate an example using the information above.

Working Capital Cycle = 85 + 20 – 90 = 15

It means the company is out of pocket for only 15 days before receiving full payment.

Download CFI’s Excel template to advance your finance knowledge and perform better financial analysis.

In the above example, we saw a business with a positive, or normal, cycle of working capital. Sometimes, however, businesses enjoy a negative working capital cycle where they collect money faster than they pay off bills.

Sticking with the above example, imagine now that the company decides to become a “cash only” business with its customers. By only accepting cash (no credit cards or payment terms), its accounts receivable days become 0.

Let’s use the same formula again and calculate their new cycle time.

Working Capital Cycle = 85 + 0 – 90 = –5

This means the company receives payment from customers 5 days before it has to pay its suppliers.

Negative working capital is common in some industries, such as grocery retail and the restaurant business. For a grocery store, customers pay upfront, inventory moves relatively quickly, but suppliers often give 30 days (or more) credit. This means that the company receives cash from customers before it needs the cash to pay suppliers.

Negative working capital is a sign of efficiency in businesses with low inventory and accounts receivable. In other situations, negative working capital may signal a company is facing financial trouble if it doesn’t have enough cash to pay its current liabilities.

Businesses with normal/positive cycles often require financing to cover the period of time before they receive payment from customers and clients. This is especially true for rapidly growing companies. A common warning axiom regarding growth and working capital is to be careful not to “grow the company out of money.”

To deal with this potential problem, companies often arrange to have financing provided by a bank or other financial institution. Banks will often lend money against inventory and will also finance accounts receivable.

For example, if a bank believes the company is capable of liquidating its inventory at 70 cents on the dollar, it may be willing to provide a loan equal to 50% of the value of the inventory (the 20% difference between 70% and 50% gives the bank a buffer, or financing cushion, in case the inventory has to be liquidated).

Additionally, if a company sells products to businesses that have high creditworthiness, the bank may finance those receivables (called “factoring”) by providing early payment of a percentage of the total revenue.

By combining one or both of the above financing solutions, a company can successfully bridge the gap of time required for it to conclude its working capital cycle.

In financial modeling and valuation, one of the key sets of assumptions about a company concerns its accounts receivable days, inventory days, and accounts payable days.

When building a financial model, it is important to clearly lay out these assumptions and understand their impact on the business.

To learn more, check out CFI’s online financial modeling courses.

Analysis of Financial Statements