Get In-Demand Finance Certifications

Counterparty credit risk (CCR) is a major concern in financial markets, affecting transactions in trading, derivatives, and securities. It represents the likelihood that the other party in a financial transaction will default or fail to fulfill financial obligations before the contract is settled. If one party defaults, the other may face significant financial losses, making effective risk management essential.

Unlike traditional borrower credit risk, which only affects the lender if the borrower fails to repay, CCR is often bilateral, meaning both parties in the transaction face potential exposure. This means that if one party defaults, the other may suffer financial losses, making risk management more complex.

CCR plays a crucial role in maintaining financial market stability. If not managed properly, it can lead to systemic disruptions, as seen during the 2008 financial crisis when widespread impact of counterparty failures triggered massive losses in derivatives markets, leading to the collapse of Lehman Brothers. Financial institutions with significant exposure to Lehman were unable to collect on obligations, leading to widespread market instability.

This event underscored the importance of managing counterparty credit risk effectively and implementing stronger regulatory measures.

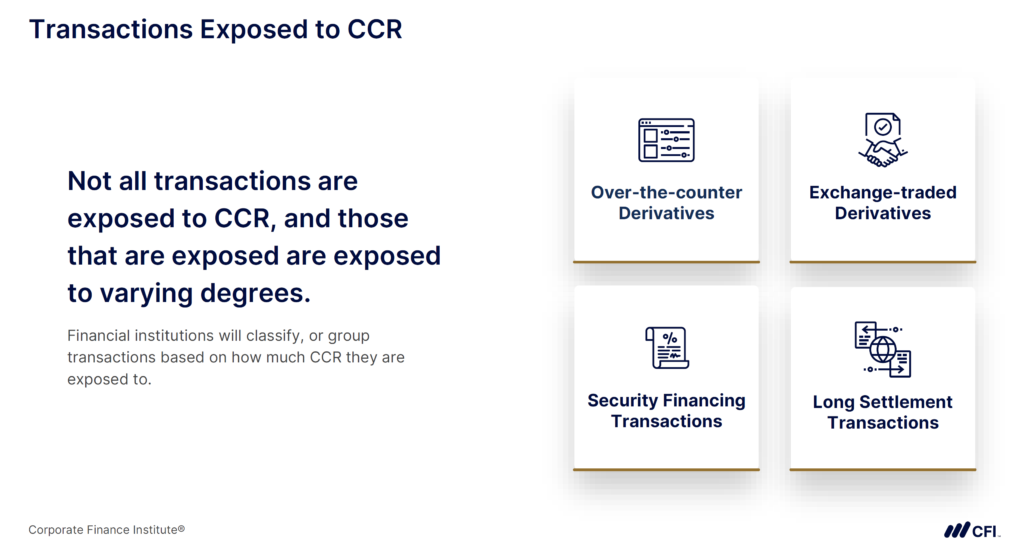

Counterparty credit risk can occur differently across various financial instruments and markets, including trading, investment, and derivatives.

OTC derivatives are financial contracts privately negotiated between two parties rather than traded on a centralized exchange. An interest rate swap, where two parties exchange interest payments on a notional amount, is a common example. These derivatives pose higher counterparty risk since no central clearinghouse guarantees settlement.

Securities lending is a process where one party temporarily lends securities to another, usually to facilitate short selling. The borrower provides collateral, but if they fail to return the securities, the lender faces counterparty credit risk.

A form of short-term borrowing, Repos allow one party to sell securities with an agreement to repurchase them later at a higher price. The risk arises if the borrower fails to buy back the securities, leaving the lender exposed to losses.

Agreements to exchange one currency for another at a predetermined rate. These contracts expose parties to counterparty credit risk if one party fails to deliver the agreed currency at settlement.

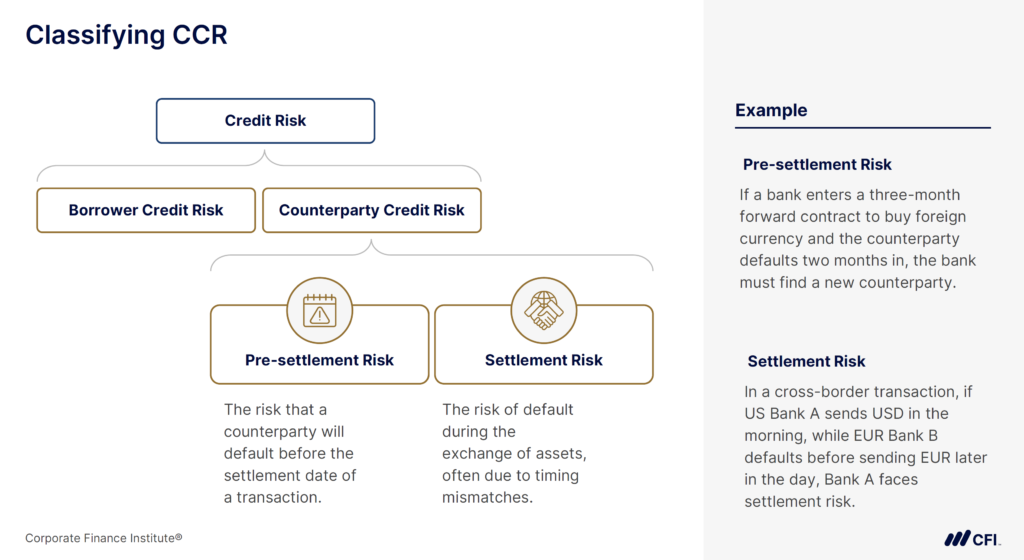

Understanding the two distinct types of CCR — pre-settlement risk and settlement risk — helps financial professionals develop targeted risk mitigation strategies:

Pre-settlement risk, also called replacement risk, occurs when a counterparty defaults before the settlement date. As a result, the other party must replace the contract, potentially at unfavorable market prices.

Settlement risk occurs during the actual exchange of assets, often due to timing mismatches in payments between parties.

Financial institutions employ sophisticated metrics to quantify and manage CCR effectively:

Effective CCR management requires a comprehensive, multi-layered approach:

Counterparty credit risk is a constant factor in financial markets. Managing CCR risk is crucial for market stability and preventing financial disruptions. For finance and risk management professionals, building expertise in counterparty credit risk enhances technical skills, sharpens decision-making, and strengthens risk assessment.

Want to build a deeper understanding of risk management strategies in banking? CFI’s Risk Management Specialization provides a hands-on program equipping you with the practical skills needed to create effective risk strategies and navigate complex regulatory environments.

Explore the Risk Management Specialization!

Credit Risk Analyst Career Profile