Get In-Demand Finance Certifications

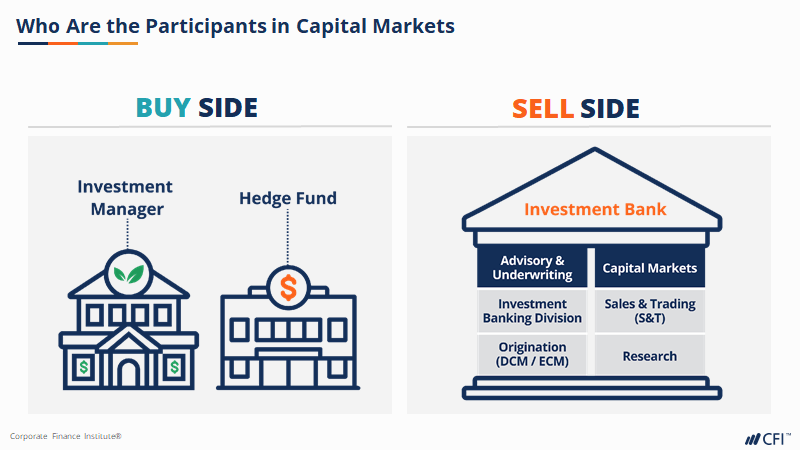

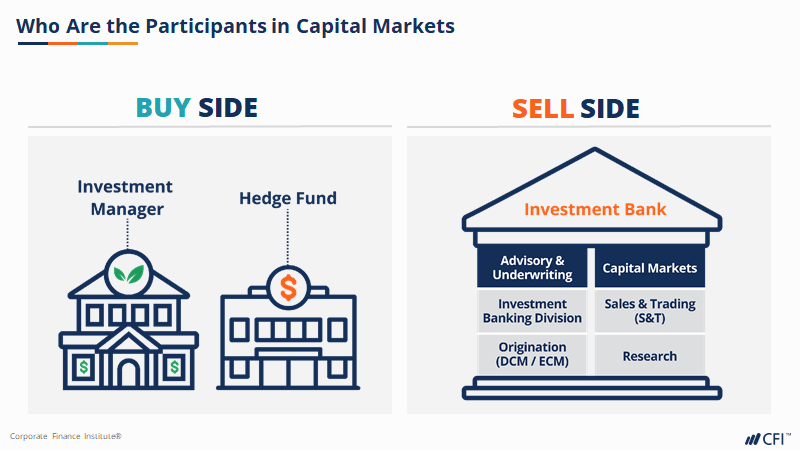

Investment banking and private equity are both industries found within the finance sector. Private equity engages in investment management activities (the buy side), while investment banks are involved in securities intermediation and brokerage (the sell side).

Private equity (PE) and venture capital invest in assets that are not publicly traded or listed. Private equity firms can work with investment banks to take publicly traded companies private (i.e., leveraged buyout) and acquire private businesses from venture capital firms and other owners. A private equity firm may also focus on other business interests, such as real estate investment.

Private equity typically requires a controlling interest and employs strategies such as improving operations, restructuring, or making strategic changes. Private equity aims to improve the performance and enhance the enterprise value of potential investments to generate a higher return on investment. The fund performance depends on exit opportunities such as an initial public offering (IPO), or a sale to another PE firm or strategic buyer.

Private equity firms tend to invest in profitable ventures with known cash flow in the mid to late stage of growth. Firms evaluate investment opportunities on a longer horizon than hedge funds, and call on private investors who share similar business interests and investment thesis when deploying the committed capital.

Private equity funds vary widely in size; rather than using their own money, they raise capital from a diverse group of investors, including institutional investors (such as pension funds) to high-net-worth individuals.

Private equity, alongside hedge funds and other buy side roles, are common exit opportunities for an investment banker. More information can be found in our buyout equity career profile.

Investment banking is the division of a bank or financial institution that serves governments, corporations, and institutions by providing underwriting (capital raising) and mergers and acquisitions (M&A) advisory services. Investment banks act as intermediaries between investors (who have money to invest) and corporations (who require capital to grow and run their businesses).

An investment bank is a natural sell-side partner to private equity firms on financial transactions, whether by connecting with PE firms looking to invest or by raising capital in capital markets (like debt in the fixed income market).

Bulge bracket investment banks and bulge bracket banks are terms describing large banks that operate globally and are leaders in investment banking, such as JPMorgan, Goldman Sachs and Bank of America Securities (formerly Merrill Lynch). Typical clients are large, multi-national corporations. Investment banks bring the experience and network to successfully execute deals for publicly traded companies looking to raise money.

For more information on investment banking services, careers, and skills of an investment banking analyst, see our investment banking overview.

Investment banking and private equity are industries that operate within the financial sector, their core functions, objectives, and methods of operation are distinct. To read more on the differences in roles of the industries, see our buy side vs. sell side overview.

Private equity firms invest in private companies or take public companies private. They raise funds from institutional investors and wealthy individuals to acquire ownership stakes in companies.

Private equity firms typically acquire a significant ownership stake in the companies they invest in and often take an active role in managing and improving those companies. They may bring in operational expertise, implement strategic changes, and work towards increasing the value of the businesses.

Private equity firms aim to improve the performance of their portfolio companies over a specific period, typically 3-7 years, before exiting the investments to realize a return. This could involve selling the companies, taking them public through an IPO, or other strategic transactions.

Investment bankers advise corporations, governments, and other institutions. This includes mergers and acquisitions (M&A), capital raising (such as issuing stocks or bonds), restructuring, and other financial services.

Investment banks facilitate the buying and selling of securities in the capital markets. They underwrite and distribute new securities, trade equities, bonds, and other financial instruments on behalf of clients, or for the banks’ own accounts.

Any investment bank may engage in risk management activities, including trading, hedging, and providing risk management solutions to clients to mitigate financial risks.

The work-life balance at an investment bank and a private equity firm can significantly differ due to the nature of the roles and the demands of each profession:

Investment bankers are notorious for their demanding workload, often requiring long hours, including late nights and weekends, especially during deal closings or busy periods. Investment banking analysts and associates commonly work 80-100 hours per week or more, handling financial modeling, due diligence, and client presentations.

The fast-paced environment and high-pressure situations in investment banking can lead to intense work schedules, tight deadlines, and a constant need to meet client demands.

Investment bankers work closely with clients on financial transactions, mergers, acquisitions, and capital raising, which can involve frequent travel and irregular hours based on deal timelines.

While private equity can also be demanding, it generally offers a comparatively better work-life balance than investment banking. Private equity associates and other professionals might work long hours during certain phases of deals or while conducting due diligence, but the workload tends to be more predictable and structured.

Private equity associates and professionals experience variations in workload based on deal cycles. During the acquisition phase or when actively managing companies, the workload might increase, but it’s often less intense and more predictable compared to investment banking.

Private equity professionals spend time not only on deal sourcing and execution but also on actively managing and adding value to their portfolio, which can result in a more balanced work schedule compared to the deal-focused nature of investment banking.

The differences in work-life balance diminish for senior roles, such as managing director, senior vice president, and other senior management, as most senior roles take on leadership and relationship management and have less direct involvement in deal execution.

Compensation in private equity firms and investment banks can differ based on several factors, like seniority, firm size, location, and performance. Generally, both fields offer high compensation, but they have distinct structures.

Investment banking tends to offer substantial bonuses, particularly for junior analysts and associates, alongside base salaries. These bonuses can often be a significant multiple of the base salary, especially in top-tier firms. As individuals move up the hierarchy to vice president, director, and perhaps managing director roles, the proportion of compensation shifted toward bonuses may change, but the overall compensation remains high.

In private equity, compensation also consists of base salary and bonuses, but the bonus structure can be significantly different. PE firms typically offer carried interest or a share in the profits from investments as a major component of compensation, especially as a private equity associate progresses to a more senior professional. This means that successful deals and investment performance can result in substantial rewards, often surpassing what’s seen in investment banking.

Overall, while investment banking might offer larger upfront bonuses, the potential for higher earnings over time, especially at senior levels, is typically greater in private equity (and venture capital) due to carried interest and profit-sharing arrangements. But both industries are known for offering lucrative compensation packages.

Private equity firms make money through a combination of strategies and mechanisms associated with their investments in private companies. Here are some primary ways they generate returns:

Firms aim to buy companies at a certain valuation, improve their operations, growth prospects, and overall value over a period, and then sell them at a higher valuation, generating capital gains. This increase in value is often achieved through operational improvements, cost reductions, revenue growth, and strategic initiatives.

PE firms often use leverage or borrowed money to finance a significant portion of the acquisition price of a company. If the company’s value increases, the returns on the equity invested are amplified due to the use of leverage. However, this also increases the risk.

Firms charge management fees (a percentage of assets under management) to their investors. They also earn performance fees, commonly referred to as carried interest, which is a percentage of the profits generated by the investments. This carried interest is typically around 20% and serves as a substantial source of revenue for the private equity firm once they exceed a certain level of returns for their investors, known as the hurdle rate.

During the holding period of their investments, private equity firms may influence the portfolio companies to distribute dividends, allowing them to recoup a portion of their initial investment while still retaining ownership.

Private equity investors realize their gains primarily through exit strategies. This includes selling assets through initial public offerings (IPOs), selling to other companies (strategic sales), selling to other private equity firms, or management buyouts.

Successful private equity investments depend on the ability of the firm to identify undervalued companies, implement strategies to enhance their value, and execute profitable exits. The returns generated for investors are a combination of capital appreciation, distributions, and carried interest earned upon successful exits.

Investment banks generate revenue through various streams, including:

Investment bankers earn fees by advising companies on mergers and acquisitions (M&A), restructuring, and other transactions. This includes providing strategic advice, valuations, and negotiation assistance.

Investment bankers help companies in raising capital through debt or equity offerings (IPOs, secondary offerings, bonds, etc.). They may buy securities from the issuer at a discount (via a bought deal) and then sell them to investors at a higher price, earning the difference (underwriting spread).

Investment banks facilitate the buying and selling of financial instruments such as stocks, bonds, derivatives, and commodities for clients. They earn money through commissions, bid-ask spreads, and market-making activities.

Some investment banks have asset management divisions that manage client investments in various financial products, earning fees based on assets under management (AUM).

Investment banks provide research reports and analyses on companies, industries, and market trends. While this may or may not directly generate revenue, it can attract clients to other fee-based services.

Investment banks assist in arranging and syndicating loans for corporations and governments, earning fees for this service.

These revenue streams can fluctuate based on market conditions, regulatory changes, and the overall economic environment. Investment banks often have diverse operations that allow them to adapt and generate revenue from different areas of the financial markets.

Internships, networking, and gaining relevant work experience through entry-level positions in finance-related roles (like analyst positions in banks, consulting firms, or corporate finance) can significantly enhance one’s prospects of breaking into investment banking or private equity.

A track record of deal experience, strong quantitative abilities, and a demonstrated passion for finance and investing are highly valued by both industries.

Connect what you just learned to a clear career path with CFI’s role‑based courses and certification programs.

Thank you for reading this article on the differences between private equity and investment banking. CFI is the official provider of the global Financial Modeling & Valuation Analyst (FMVA)™ certification program, designed to help anyone become a world-class financial analyst.

To learn more, see these additional relevant resources below:

Investment Banking Interview Questions