Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

Report of cash generated and spent for a certain period

A statement of cash flows shows how cash moves in and out of a business over a period and links the income statement and balance sheet. The statement of cash flows (also referred to as the cash flow statement) is one of the three key financial statements. The cash flow statement reports the cash generated and spent during a specific period of time (e.g., a month, quarter, or year). The statement of cash flows acts as a bridge between the income statement and balance sheet by showing how cash moved in and out of the business.

Download CFI’s free Excel template and start practicing today.

“Cash is king” is an old saying about business. Since the income statement and balance sheet are based on accrual accounting, those financials don’t directly measure what happens to cash over a period. Therefore, companies typically provide a cash flow statement for management, analysts, and investors to review.

Another useful aspect of the cash flow statement is to compare operating cash flow to net income. This comparison measures how well a company is running its operations. The cash flow statement reflects the actual amount of cash the company receives from its operations.

Cash flow: Inflows and outflows of cash and cash equivalents (learn more in CFI’s Ultimate Cash Flow Guide).

Cash balance: Cash on hand and demand deposits (cash balance on the balance sheet).

Cash equivalents: Cash equivalents include cash held as bank deposits, short-term investments, and any very easily cash-convertible assets — includes overdrafts and cash equivalents with short-term maturities (less than three months).

Below is a breakdown of each section in a statement of cash flows. …This breakdown helps you see where cash is generated and how it is used across the business. While each company will have its own unique line items, the general setup is usually the same.

Operating activities are the principal revenue-producing activities of the entity. Cash flow from operations typically includes the cash flows associated with sales, purchases, and other expenses.

The company’s chief financial officer (CFO) chooses between the direct and indirect presentation of operating cash flow:

The items in the operating cash flow section are not all actual cash flows but include non-cash items and other adjustments to reconcile profit with cash flow. Analysts often focus on whether cash from operating activities consistently exceeds net income, a sign of high-quality earnings.

The value of various assets declines over time when used in a business. As a result, D&A are expenses that allocate the cost of an asset over its useful life. Depreciation involves tangible assets such as buildings, machinery, and equipment, whereas amortization involves intangible assets such as patents, copyrights, goodwill, and software.

D&A reduces net income in the income statement. However, we add this back into the cash flow statement to adjust net income because these are non-cash expenses. In other words, no cash transactions are involved.

Working capital represents the difference between a company’s current assets and current liabilities. Any changes in current assets (other than cash) and current liabilities (other than debt) affect the cash balance in operating activities.

For instance, when a company buys more inventory, current assets increase. This positive change in inventory is subtracted from net income because it is a cash outflow. It’s the same case for accounts receivable. When it increases, it means the company sold their goods on credit. There was no cash transaction even though revenue was recognized, so an increase in accounts receivable is also subtracted from net income.

Conversely, if a current liability, like accounts payable, increases this is considered a cash inflow. This is because the company has yet to pay cash for something it purchased on credit. This increase is then added to net income (a decrease would be subtracted).

Cash flow from investing activities includes the acquisition and disposal of non-current assets and other investments not included in cash equivalents. Investing cash flows typically include the cash flows associated with buying or selling property, plant, and equipment (PP&E), other non-current assets, and other financial assets.

Cash spent on purchasing PP&E is called capital expenditures (CapEx). CapEx investments might mean purchases of new office equipment such as computers and printers for a growing number of employees, or the purchase of new land and a building to house business operations and logistics of the company. These items are necessary to keep the company running. These investments are a cash outflow, and therefore will have a negative impact when we calculate the net increase in cash from all activities. Learn how to calculate CapEx with the CapEx formula.

Cash flow from financing activities results from changes in a company’s capital structure. Financing cash flows include cash flows associated with borrowing and repaying bank loans or bonds and issuing and buying back shares. The payment of a dividend is also treated as a financing cash flow.

A company issues debt as a way to finance its operations. The issuance of debt is a cash inflow, because a company finds investors willing to act as lenders. However, when these debt investors are paid back, then the repayment is a cash outflow.

This is another way of financing a company’s operations. Issuance of equity is an additional source of cash, so it’s a cash inflow. Conversely, an equity repurchase is a cash outflow. This is buying back, through cash payment, the equity from its investors.

We sum up the three sections of the cash flow statement to find the net cash increase or decrease for the given time period. This amount is then added to the opening cash balance to derive the closing cash balance. This amount will be reported in the balance sheet statement under the current assets section. This is the final piece of the puzzle when linking the three financial statements.

The opening cash balance is last year’s closing cash balance. We can find this amount from last year’s cash flow statement and balance sheet statement.

Learn how to analyze a statement of cash flows in CFI’s Financial Analysis Fundamentals course.

Below is an example from Amazon’s 2022 annual report, which breaks down the cash flow generated from operations, investing, and financing activities. Learn how to analyze Amazon’s consolidated statement of cash flows in CFI’s Amazon Advanced Financial Modeling course.

Earlier, we discussed how the cash from operating activities can use either the direct or indirect method. Most companies report using the indirect method, although some will use the direct method (see CVS’s 2022 annual report here).

Remember that the indirect method begins with a measure of profit, and some companies may have discretion regarding which profit metric to use. While many companies use net income, others may use operating profit/EBIT or earnings before tax.

If the starting point profit is above interest and tax in the income statement, then interest and tax cash flows will need to be deducted if they are to be treated as operating cash flows. Clearly, the exact starting point for the reconciliation will determine the exact adjustments made to get down to an operating cash flow number.

| Profit | P |

| Depreciation | D |

| Amortization | A |

| Impairment expense | I |

| Change in working capital | ΔWC |

| Change in provisions | ΔP |

| Interest Tax | (I) |

| Tax | (T) |

| Operating cash flow | OCF |

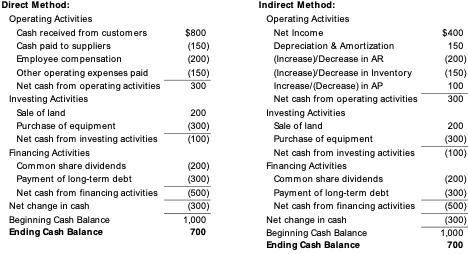

As we discussed, the operating section of the statement of cash flows can be presented using either the direct or indirect method. With either method, the investing and financing sections are identical; the only difference is in the operating section. The direct method shows the major classes of gross cash receipts and gross cash payments.

Regardless of the method, the cash flows from the operating section will give the same result. However, the presentation will differ. Below is an illustrative comparison of the two approaches.

Under IFRS, there are two allowable ways of presenting interest expense or income in the cash flow statement. Many companies present both the interest received and interest paid as operating cash flows. Others treat interest received as investing cash flow and interest paid as a financing cash flow. The method used is the company’s choice.

Under U.S. GAAP, interest paid and received are always treated as operating cash flows.

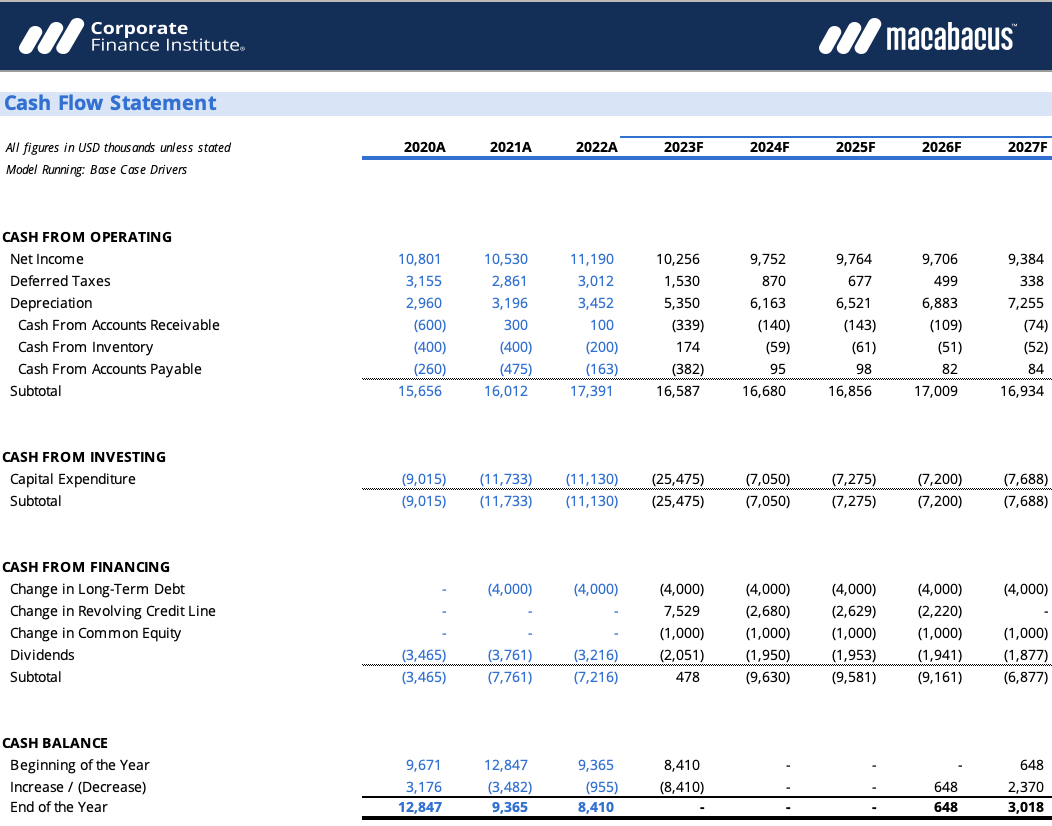

A cash flow statement in a financial model in Excel displays both historical and projected data. Before this model can be created, we first need to have the income statement and balance sheet built in Excel, since that data will ultimately drive the cash flow statement calculations.

As shown in our financial model example above, historical data appears in blue font, while forecasted data appears in black font. The table below serves as a general guideline for where to find historical data to hardcode for the line items.

Additionally, it shows where we find the calculated or referenced data to fill in the forecast period section. When all three statements are built in Excel, we now have what we call a “Three-Statement Model”.

| Line Items | Historical Results (Annual Report) | Forecast Periods (Model) |

|---|---|---|

| Net Earnings | Income Statement | Income Statement |

| Depreciation & Amortization | Income Statement | PP&E Schedule |

| Changes in Working Capital | Balance Sheet | Working Capital Schedule |

| Capital Expenditures | Balance Sheet | PP&E Schedule |

| Debt Issuance | Balance Sheet | Debt Schedule |

| Equity Issuance | Balance Sheet | Equity Schedule |

| Opening Cash Balance | Prior Period Balance Sheet | Prior Period Balance Sheet |

Below is a helpful video explanation of what the statement of cash flows is, how it works, and why it’s important. Check out the video, and you’ll learn a lot in just a few minutes!

Connect what you just learned to a clear career path with CFI’s role‑based courses and certification programs.