Notice to Reader Report

A compilation of financial statements using financial data provided by the management

What is the Notice to Reader Report?

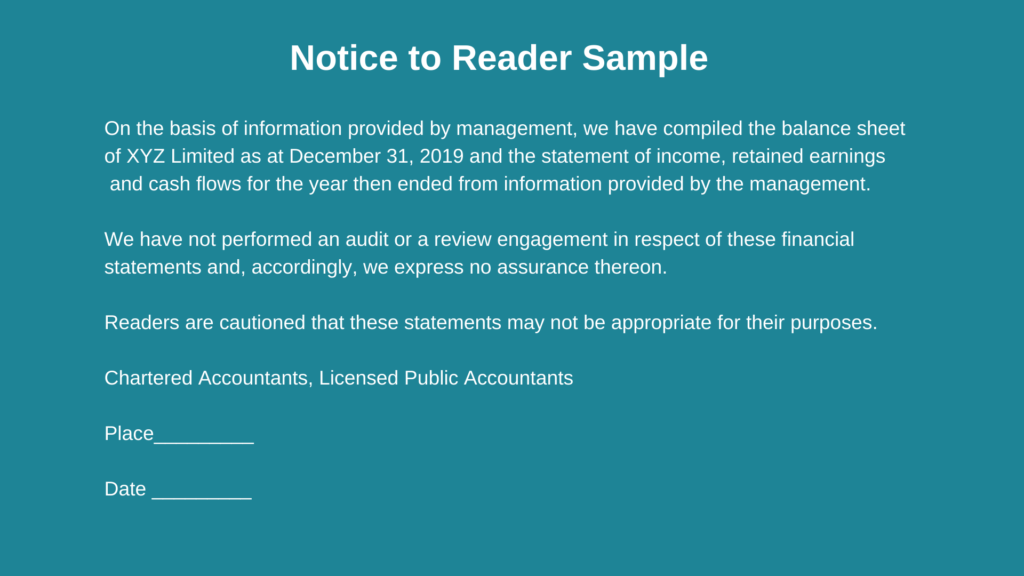

The notice to reader report is a compilation of financial statements using financial data provided by the management. The report is prepared by an external chartered accountant, and it does not provide assurance on the correctness of the financial statements.

The notice means that the prepared financial statements have not been audited or reviewed, and therefore, the accountant offers no assurance on the accuracy of the financial statement. However, the report gives confidence to certain users, such as directors and shareholders of the company.

The goal of the notice to reader is to use the information provided by the management or owners and prepare and present financial statements that are correct and not misleading in the opinion of the management.

The main financial statements prepared in the report include the income statement, balance sheet, cash flow statement, and statement of retained earnings. Each page of the notice to reader report should include a “notice to reader” note at the top of the page to denote the level of usefulness of the report. It cautions users that the report may not be appropriate for their use since it is prepared for a specific purpose.

Key Components of the Notice to Reader Report

The following are some of the elements included in the notice to reader report:

1. Nature of assignment

The report explicitly states the nature of work that the accountant is required to perform. The accountant should state that compiled financial statements were prepared based on the information provided by the management or owners of the company, and that that he/she did not conduct an audit or review of the statements. It cautions users of the financial statement from interpreting the report as a vote of confidence on the correctness of the financial statements.

2. Scope limitation

The report also discloses the scope of limitation of the accountant’s work. The limitation informs users of the report that there is no form of assurance that is expressed on the financial statements.

3. Caution to reader

The compiled financial statements should include a “notice to reader” heading to denote that it is not appropriate for the user’s purposes. The management furnishes the accountant with information to be used in compiling financial statements, and it is necessary to caution readers on the level of reliability they should place on the report.

Qualities of the Notice to Reader Report

1. Prepared by an external chartered accountant

Notice to reader financial statements are prepared by a licensed external chartered accountant or a CPA. The financial statements cannot be prepared by the in-house accountant or bookkeeper using the company’s accounting systems. However, if the company uses an external accountant to prepare year-end tax returns, it can use the same accountant to prepare the notice to reader financial statements.

2. Financial statements are not audited

Although notice to reader reports are prepared by an external professional accountant, the accountant only prepares the financial statements based on the information provided by management and does not audit the numbers to verify their accuracy.

The compiled financial statements should be clearly marked “unaudited” to inform readers that the prepared reports have not been audited and should not be interpreted as an assurance on the correctness of the compiled statements.

3. Purpose of financial statements

The notice to reader financial statements should include a note that cautions readers that the compiled statements may not be appropriate for their purpose. Usually, the statement is prepared for specific purposes, such as obtaining bank financing from a financial institution or when selling the business. Such financial statements may not be appropriate for other types of users.

4. Nature of work

The purpose of the notice to reader is to compile financial statements based on the raw financial data provided by the management. The external accountant is provided with data, and they are not required to verify the authenticity of the information provided.

While licensed accountants are required to maintain their independence from their client, the standards that guide notice to reader financial statements are usually less strict on the expected performance of the practitioner.

Uses of the Notice to Reader Report

Here are some of the reasons why notice to reader report may be prepared:

1. Investors

When investing in small companies or startups, investors may require key financial statements to analyze the companies’ assets vs. liabilities, profitability, and future growth potential. The accountant will be required to prepare financial statements that provide specific information that the investors require.

2. Selling a business

During a merger or acquisition transaction, prospective buyers may require financial statements for the past three to five years to help in their due diligence. The management may engage an external accountant to prepare the notice to reader financial statements that provide the information required by prospective buyers.

A review or audit engagement may only be required in complex M&A transactions or in the case of large companies with substantial annual revenues.

3. Creditors

Banks may require clients to furnish them with the latest financial statement during the assessment of credit applications or routine evaluation of the creditworthiness of existing borrowers. The company may require the external accountant to prepare specific financial statements that provide the information required by the creditor.

Related Readings

CFI is the official provider of the global Commercial Banking & Credit Analyst (CBCA)™ certification program, designed to help anyone become a world-class financial analyst. To keep advancing your career, the additional resources below will be useful:

Additional Resources

CFI is a global provider of financial modeling courses and of the FMVA Certification. CFI’s mission is to help all professionals improve their technical skills. If you are a student or looking for a career change, the CFI website has many free resources to help you jumpstart your Career in Finance. If you are seeking to improve your technical skills, check out some of our most popular courses. Below are some additional resources for you to further explore:

The Financial Modeling Certification

Analyst Certification FMVA® Program

CFI is a global provider of financial modeling courses and of the FMVA Certification. CFI’s mission is to help all professionals improve their technical skills. If you are a student or looking for a career change, the CFI website has many free resources to help you jumpstart your Career in Finance. If you are seeking to improve your technical skills, check out some of our most popular courses. Below are some additional resources for you to further explore:

The Financial Modeling Certification

Below is a break down of subject weightings in the FMVA® financial analyst program. As you can see there is a heavy focus on financial modeling, finance, Excel, business valuation, budgeting/forecasting, PowerPoint presentations, accounting and business strategy.

A well rounded financial analyst possesses all of the above skills!

Additional Questions & Answers

CFI is the global institution behind the financial modeling and valuation analyst FMVA® Designation. CFI is on a mission to enable anyone to be a great financial analyst and have a great career path. In order to help you advance your career, CFI has compiled many resources to assist you along the path.

In order to become a great financial analyst, here are some more questions and answers for you to discover:

- What is Financial Modeling?

- How Do You Build a DCF Model?

- What is Sensitivity Analysis?

- How Do You Value a Business?

Accounting Crash Courses

CFI is a global provider of financial modeling courses and of the FMVA Certification. CFI’s mission is to help all professionals improve their technical skills. If you are a student or looking for a career change, the CFI website has many free resources to help you jumpstart your Career in Finance. If you are seeking to improve your technical skills, check out some of our most popular courses. Below are some additional resources for you to further explore:

The Financial Modeling Certification

Boost your confidence and master accounting skills effortlessly with CFI’s expert-led courses! Choose CFI for unparalleled industry expertise and hands-on learning that prepares you for real-world success.