Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

How cash is tracked for a transaction

A Sources and Uses of Cash schedule gives a summary of where capital will come from (the “Sources”) and what the capital will be spent on (the “Uses”) in a corporate finance transaction. When computing their total amounts, the sources and uses accounts should equal each other.

The sources and uses schedule becomes very important and useful when creating a model for situations such as Recapitalization, Restructuring, and Mergers & Acquisitions. Therefore, it is commonly used in investment banking.

This guide will teach you all you need to know about a Sources and Uses Cash Schedule and how to build one yourself…an important step in becoming a world-class financial analyst.

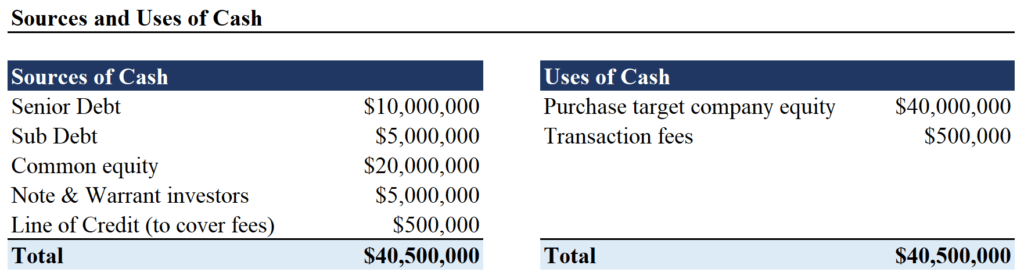

Here is an example of a sources and uses schedule. The table illustrates the sources and uses of cash in a transaction. The two sides must equal each other. This is commonly performed in the financial modeling of a deal.

Calculating the Purchase Price to acquire a target business or asset is the first step in determining how much cash is needed and where it can be obtained from. The source of financing may be either known or assumed.

Working Capital: Working capital is found in the closing balance sheet of the target company. A successful business must have sufficient, ready reserves of working capital on hand when it needs to use it. When a company experiences a shortfall in liquid assets, it will need to draw cash from somewhere to fund its day-to-day operations, meet its current liabilities, and continue earning more revenues. See the working capital formula here.

Fixed Assets: This is calculated by taking the Purchase Price minus the Working Capital Assets. Fixed assets are tangible, long-term assets that take more time to be converted into cash and are used in the production of a company’s income. They can take the form of buildings, machinery, vehicles, land, software, and computer equipment. The largest group of these is referred to as Property, Plant & Equipment (PP&E).

Fees: The fees must have their own schedule. They have to be known or assumed for the calculation of the total uses of cash. These are fees incurred during an acquisition.

Total Uses: This is the sum of the purchase price of the asset and the fees.

Debt: This is usually expressed as a multiple of EBITDA (Debt/EBITDA). Examples of corporate debt are bonds, debentures, commercial paper, and loans.

Preferred Equity: The value of this type of equity is typically assumed in aggregate. It sits in-between senior debt and common equity and combines features of both debt and equity.

Common Equity: This is determined by subtracting both debt and preferred equity from the total sources of cash. Its amount is the total investment that common shareholders have in a company. It’s held by founders, employees, and outside investors.

Total Sources: This should equal the Total Uses of Cash.

A recapitalization aims to achieve a more stable or optimal mix of both debt and equity. The change is in the capital structure of a company. Recapitalization may be done for a number of reasons, such as minimizing the taxes paid by the company, preventing a hostile takeover, or as part of executing an exit strategy for Venture Capital investors.

If a company swaps debt for equity, that means it will issue shares to pay down debt, thereby increasing the share of equity capital and maintaining more cash in the business. In contrast, issuing more debt gives the company cash to buy back shares or pay out dividends. One of the benefits of debt financing is that interest paid is tax-deductible.

To learn more, check out our financial modeling and valuation courses.

Restructuring happens when a company wants to improve its business profitability and steer clear of financial difficulties. It involves changing the structure, operations, and debt of a company. For instance, a company may not be generating enough revenue to cover its expenses because its below-par products aren’t selling enough.

To meet debt obligations and make payroll payments, the company may have to reduce its size through the sale of assets. Furthermore, it may restructure the terms of its debt to possibly reduce interest payments over time.

To learn more, check out our financial modeling and valuation courses.

An acquisition means that an acquiring company will have more than 50% ownership of a target company. The company may buy all of the ownership stakes and assume total control of the target. An acquisition involves purchasing stocks and assets of the target company. The acquisition can be paid for with cash, stocks, or a combination of both.

The common motive behind this corporate action is to drive more growth for the acquirer. With an acquisition, growth can be achieved through economies of scale, greater synergy, cost reductions, or new product or service offerings in a new market. Read more about the M&A process here.

In planning for an acquisition, the Sources and Uses of Cash Table is very important, as it helps to ensure that the transaction is properly funded.

The above screenshot is from CFI’s M&A Modeling Course.

Connect what you just learned to a clear career path with CFI’s role‑based courses and certification programs.

We hope this guide to creating a “Sources and Uses of Cash Schedule” has been helpful and we encourage you to check out the additional free CFI resources below: