Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

The capital used by a company to generate profits

Capital employed refers to the amount of capital investment a business uses to operate and provides an indication of how a company is investing its money. Although capital employed can be defined in different contexts, it generally refers to the capital utilized by the company to generate profits.

The figure is commonly used in the Return on Capital Employed (ROCE) ratio to measure a company’s profitability and efficiency of capital use.

The capital employed metric can be calculated in two ways:

Where:

or,

Where:

Note: The formula chosen should be consistently applied (do not switch between formulas when conducting trend analysis or peer comparisons) as the calculation differs depending on which formula is used. Generally, total assets minus current liabilities is the most commonly used formula.

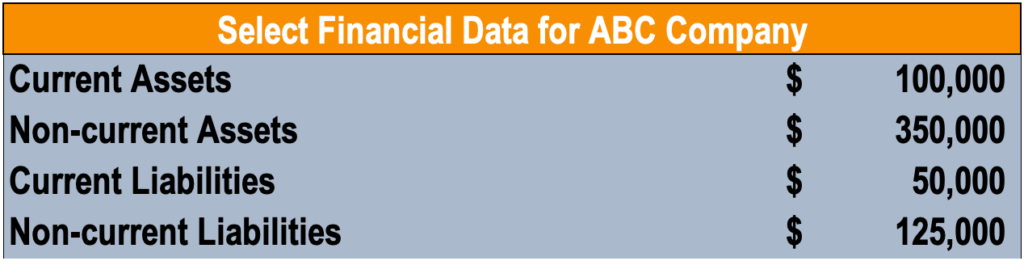

Mary is looking to calculate the capital employed of ABC Company, compiling the following information:

Using the first formula above, Mary calculates the amount as follows:

This metric provides an insight into how well a company is investing its money to generate profits. Although the figure varies depending on the formula used, the underlying idea remains the same.

The number in itself is seldom used by analysts. It is commonly used in conjunction with earnings before interest and tax (EBIT) in the return on capital employed (ROCE) ratio. As will be explained below, ROCE is a commonly used ratio by analysts for assessing the profitability of a company for the amount of capital used.

Return on capital employed (ROCE) is a profitability ratio that measures a company’s profitability and the efficiency with which it uses its capital. The ROCE is considered one of the best profitability ratios, as it shows the operating income generated per dollar of invested capital. The formula for ROCE is as follows:

Recall that the capital employed for ABC Company in our example above is $400,000. Assuming that the earnings before interest and taxes figure of ABC Company is $30,000, what is the ROCE?

For every dollar of invested capital, ABC Company generated 7.5 cents in operating income.

Connect what you just learned to a clear career path with CFI’s role‑based courses and certification programs.

Thank you for reading CFI’s guide to Capital Employed. To keep learning and advancing your career, the following CFI resources will be helpful: