Get In-Demand Finance Certifications

Assessing a business' use of its capital structure

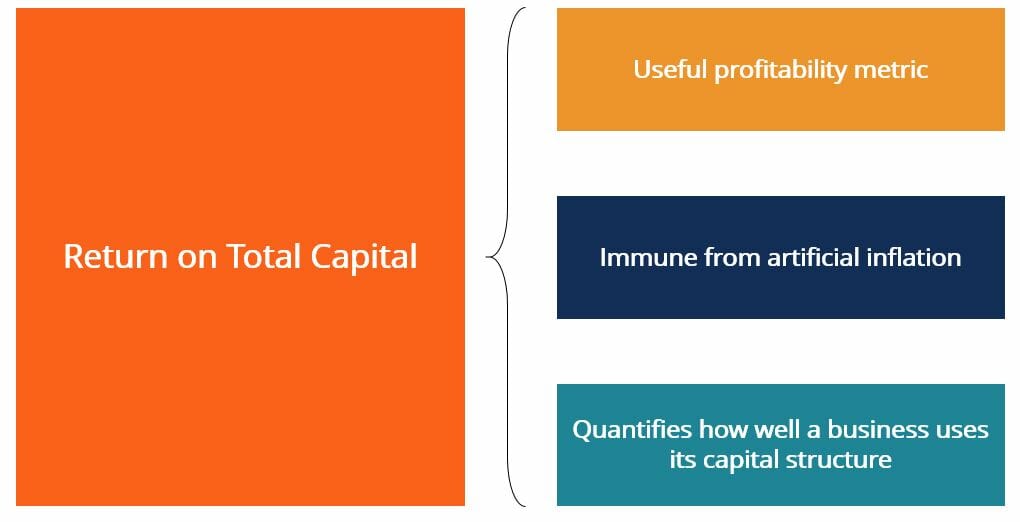

Return on Total Capital (ROTC) is a return on investment ratio that quantifies how much return a company has generated through the use of its capital structure. The ROTC ratio is different from return on common equity (ROCE), as the former quantifies the return a company has made on its common equity investment. The ROCE figure can be misleading as it does not take into account a company’s use of debt. A company that employs a large amount of debt in its capital structure will have a high ROCE.

ROTC gives a fairer assessment of a company’s use of funds to finance its projects and functions better as an overall profitability metric. This ratio is immune from artificial inflation induced by a capital structure that employs a significantly higher or lower amount of debt capital than equity capital.

Return on Total Capital can be used to evaluate how well a company’s management has utilized its capital structure to generate value for both equity and debt holders. ROTC is a better measure to assess management’s abilities than the ROCE ratio since the latter only monitors management’s use of common equity capital.

Return on Total Capital can be calculated using the formula below:

Where:

Earnings Before Interest & Taxes (EBIT) – Represents profit that the business has realized, without consideration of interest or tax payments

Total Capital – Refers to the business’ total available capital, calculated as Total Capital = Short Term Debt + Long Term Debt + Shareholder’s Equity

In the case of a business that has no liabilities outside of short-term debt, long-term debt, and total equity, return on total capital is virtually identical to the return on assets (ROA) ratio. iT is because the business’ capital structure would make up the entirety of the business’ liability section on its balance sheet. That figure would be equal to the business’ total assets. (Assets = Liabilities + Equity).

While ROA is also a useful profitability metric, it takes a more reactive approach to computing a business’ use of capital. ROA measures the value a business is able to generate based on the assets it employs rather than on capital allocation decisions.

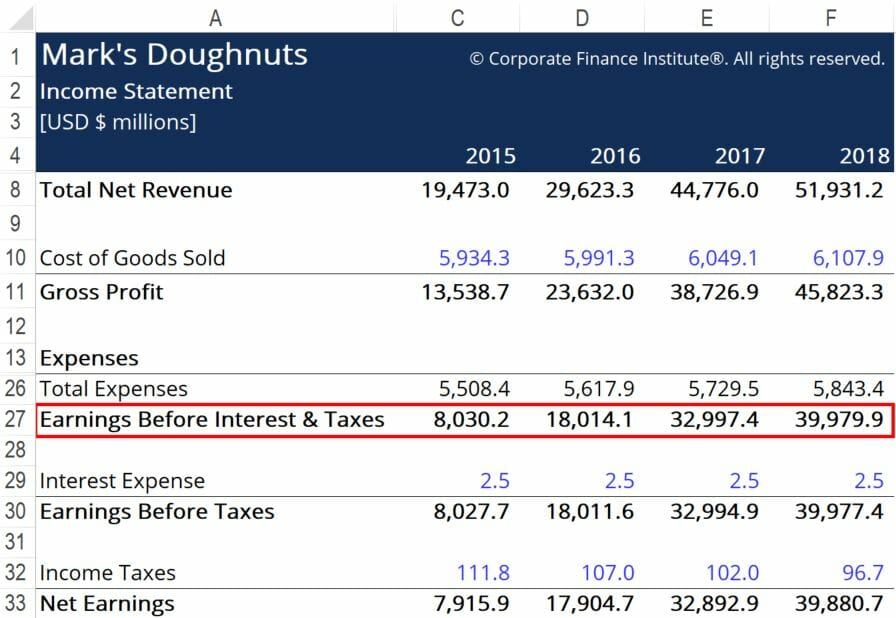

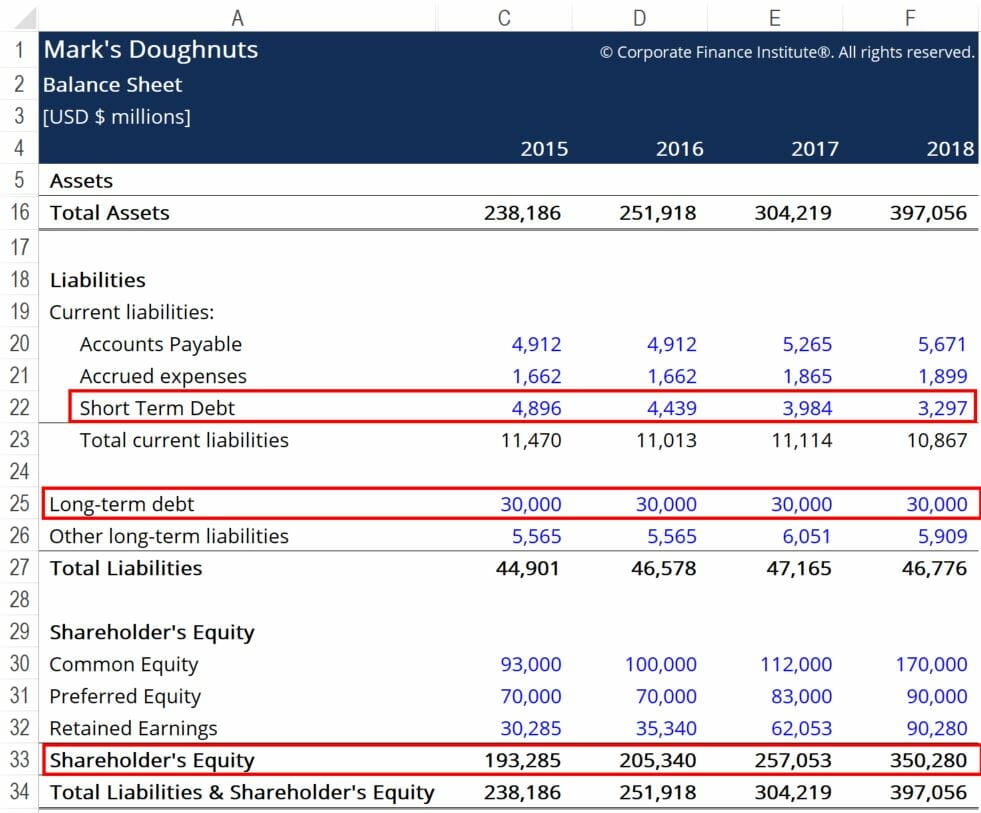

Mark’s Doughnuts wants to assess how well it has deployed its capital structure by calculating the ROTC of the business for the past few years. Below are the business’ financial statements for the past few years:

The red boxes highlight the important information we need to calculate ROTC, namely EBIT and the capital structure. Using the formula provided above, we arrive at the following figures:

ROTC more than tripled from 2015 to 2017. It indicates the company is making good use of its capital structure and pursuing NPV-positive projects.

Thank you for reading this CFI article on the Return on Total Capital ratio! To learn more about related topics, check out the following CFI resources:

Below is a break down of subject weightings in the FMVA® financial analyst program. As you can see there is a heavy focus on financial modeling, finance, Excel, business valuation, budgeting/forecasting, PowerPoint presentations, accounting and business strategy.

A well rounded financial analyst possesses all of the above skills!

CFI is the global institution behind the financial modeling and valuation analyst FMVA® Designation. CFI is on a mission to enable anyone to be a great financial analyst and have a great career path. In order to help you advance your career, CFI has compiled many resources to assist you along the path.

In order to become a great financial analyst, here are some more questions and answers for you to discover: