Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

A measure of a company’s ability to pay its financial obligations

A Coverage Ratio is any one of a group of financial ratios used to measure a company’s ability to pay its financial obligations. A higher ratio indicates a greater ability of the company to meet its financial obligations while a lower ratio indicates a lesser ability. Coverage ratios are commonly used by creditors and lenders to determine the financial standing of a prospective borrower.

The most common coverage ratios are:

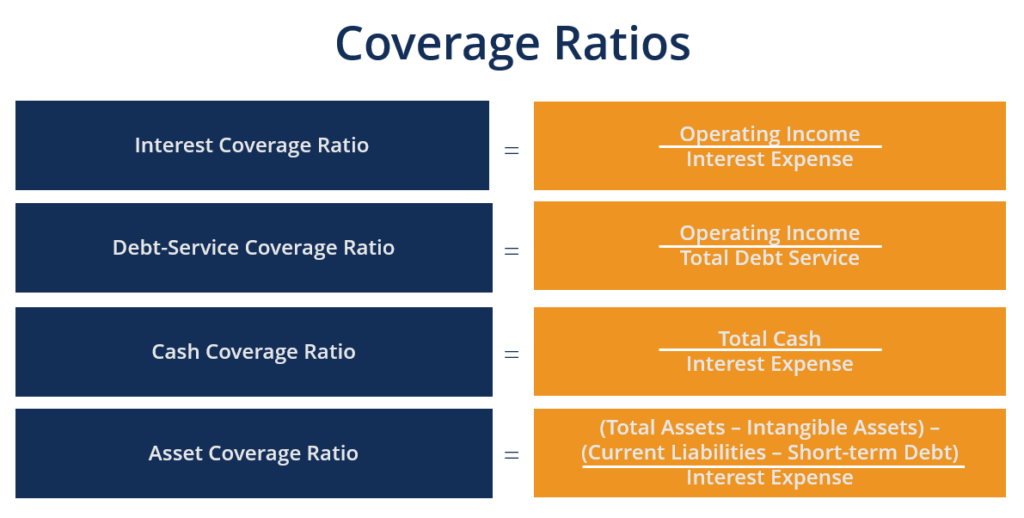

The interest coverage ratio (ICR), also called the “times interest earned”, evaluates the number of times a company is able to pay the interest expenses on its debt with its operating income. As a general benchmark, an interest coverage ratio of 1.5 is considered the minimum acceptable ratio. An ICR below 1.5 may signal default risk and the refusal of lenders to lend more money to the company.

Interest coverage ratio = Operating income / Interest expense

A company reports an operating income of $500,000. The company is liable for interest payments of $60,000.

Interest coverage = $500,000 / ($60,000) = 8.3x

Therefore, the company would be able to pay its interest payment 8.3x over with its operating income.

The debt service coverage ratio (DSCR) evaluates a company’s ability to use its operating income to repay its debt obligations including interest. The DSCR is often calculated when a company takes a loan from a bank, financial institution, or another loan provider. A DSCR of less than 1 suggests an inability to serve the company’s debt. For example, a DSCR of 0.9 means that there is only enough net operating income to cover 90% of annual debt and interest payments. As a general rule of thumb, an ideal debt service coverage ratio is 2 or higher.

Debt service coverage ratio = Operating Income / Total debt service

For example, a company’s financial statement showed the following figures:

Debt service coverage = $500,000 / ($100,000 + $150,000) = 2.0x

Therefore, the company would be able to cover its debt service 2x over with its operating income.

This is one more additional ratio, known as the cash coverage ratio, which is used to compare the company’s cash balance to its annual interest expense. This is a very conservative metric, as it compares only cash on hand (no other assets) to the interest expense the company has relative to its debt.

Cash coverage ratio = Total cash / Total interest expense

Consider a company with the following information:

Cash coverage = $50 million / $2.5 million = 20.0x

This means the company can cover its interest expense twenty times over. Since the cash balance is greater than the total debt balance, the company can also repay all the principal it owes with the cash on hand.

The asset coverage ratio (ACR) evaluates a company’s ability to repay its debt obligations by selling its assets. In other words, this ratio assesses a company’s ability to pay debt obligations with assets after satisfying liabilities. The acceptable level of asset coverage depends on the industry. An ASR of 1 means that the company would just be able to pay off all its debts by selling all its assets. An ASR above 1 means that the company would be able to pay off all debts without selling all its assets.

Asset coverage ratio = ((Total assets – Intangible assets) – (Current liabilities – Short-term debt)) / Total debt obligations

For example, a company’s financials include:

Asset coverage = (($170 million – $30 million) – ($30 million – $20 million)) / $100 million = 1.3x

Therefore, the company would be able to pay off all of its debts without selling all of its assets.

CFI is the global provider of the Financial Modeling and Valuation Analyst Program, a certification for financial analysts who want to perform world-class analysis. To continue learning and advancing your career, these additional CFI resources will be helpful: