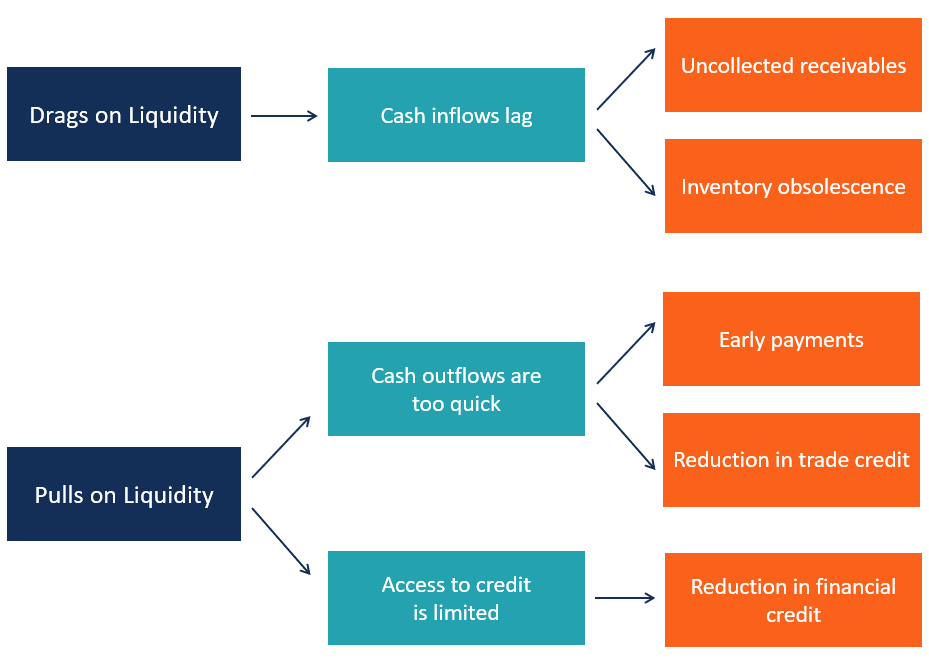

Drags and Pulls on Liquidity

Factors that negatively affect a company’s cash inflows and outflows

What are the Drags and Pulls on Liquidity?

The drags and pulls on liquidity are the factors that negatively affect a company’s cash inflows and outflows by determining a deterioration in its liquidity position.

A drag on liquidity exists when cash inflows lag, for example, because a company is facing trouble with the collection of its commercial credits. A pull on liquidity is generated when cash outflows happen too quickly or when a company’s access to commercial or financial credit is limited.

Drags on Liquidity from Uncollected Receivables

It often happens that a company is willing to sell goods and services while accepting a delayed payment. However, sometimes companies face issues with the collection of their commercial credit, for example, because one or more customers are experiencing deterioration in their business.

For an analyst, the drags are often visible from an analysis of balance sheet trends and ratios. For example, a deterioration in days sales outstanding (DSO) is often an indication of negative developments acting as drags on liquidity.

Increasing levels of bad debt expenses are also a useful indicator to identify issues in the collection of receivables.

Drags on Liquidity from Inventory Obsolescence

If a company’s inventory is turning obsolete, it will experience a drag on liquidity as the value of such inventory declines, turning into lower cash inflows than planned. Sometimes, such inventory can’t be sold or used at all, while in other cases, the company may need to sell it at significant discounts to the usual price.

Moreover, obsolete inventory may still occupy space, require labor, and generate storage costs that can be avoided. A good indication of increasing inventory obsolescence is often given by slowing inventory turnover ratios.

Drags on Liquidity from Tighter Credit

If access to capital worsens or becomes more expensive, a company’s liquidity may worsen. Credit conditions vary due to the action of several factors, including:

1. Changes in business fundamentals

Deteriorating fundamental trends, such as declining sales, falling margins, or poorer cash flow generation, are factors that would worsen a company’s creditworthiness. As a result, tighter conditions may negatively affect the company’s liquidity position.

2. Industry trends

Sometimes, whole industries suffer, or are exposed to, unfavorable trends. As a result, credit conditions granted to the companies operating in such industries can worsen, triggering a deterioration in liquidity.

3. Overall macroeconomic conditions

Bad trends in capital markets, rising interest rates, or recessionary environments are examples of macroeconomic factors that can negatively impact a company’s access to credit and worsen its liquidity position.

Pulls on Liquidity from Early Payments

Granting commercial credit is common in many industries. It often implies that a customer is allowed to pay 30, 60, or 90 days after a purchase is made.

A company that pays its suppliers, creditors, or employees before the payment is due is creating a pull on liquidity. It is a commonplace among companies to hold payments until the due date without any anticipation of payments.

Pulls on Liquidity from Trade Credit

There are other events related to commercial credit that can act as pulls on a company’s liquidity. Let’s take the case of a company that fails to pay its obligations to its suppliers on a timely basis or one that willingly takes advantage of its suppliers by paying after a long delay. In such cases, suppliers may decide to reduce the amount of trade credit to the customer – impacting its liquidity.

Pulls from Reduced Lines of Credit

As a supplier can reduce the amount of credit to a customer, banks can also reduce the amount of credit available to their customers.

Banks may decide to reduce the lines of credit to a company for many reasons:

- Company-specific reasons, such as deteriorating business trends in the company or in the bank itself. In other cases, it can be a response to a customer’s poor track record of debt repayment.

- The reductions may be mandated by governments or may be due to conditions in the credit markets, such as tighter access to funds from central banks.

Solutions to Drags and Pulls on Liquidity

The drags and pulls on liquidity should be identified and corrected promptly, especially when significant. The measures that are taken obviously depend on the specific type of drag and pull involved.

For example:

- Failure in collecting receivables can make it necessary to involve debt collection agencies and to make changes in the payment terms given to customers. In some cases, companies may stop allowing delayed payments to certain types of customers.

- If obsolescence is becoming a problem, the company should find a way to monetize the obsolete inventory before it becomes a significant drag on liquidity. It may also need to rethink or refine its inventory management system or strategy if it contributes to the issue.

- If a company expects credit-line restrictions in the future, i.e., as a result of worsening market conditions, it may try to open credit lines well above the actual current needs.

More Resources

CFI is the official provider of the global Commercial Banking & Credit Analyst (CBCA)™ certification program, designed to help anyone become a world-class financial analyst. To keep advancing your career, the additional resources below will be useful:

Additional Resources

CFI is a global provider of financial modeling courses and of the FMVA Certification. CFI’s mission is to help all professionals improve their technical skills. If you are a student or looking for a career change, the CFI website has many free resources to help you jumpstart your Career in Finance. If you are seeking to improve your technical skills, check out some of our most popular courses. Below are some additional resources for you to further explore:

The Financial Modeling Certification

Analyst Certification FMVA® Program

CFI is a global provider of financial modeling courses and of the FMVA Certification. CFI’s mission is to help all professionals improve their technical skills. If you are a student or looking for a career change, the CFI website has many free resources to help you jumpstart your Career in Finance. If you are seeking to improve your technical skills, check out some of our most popular courses. Below are some additional resources for you to further explore:

The Financial Modeling Certification

Below is a break down of subject weightings in the FMVA® financial analyst program. As you can see there is a heavy focus on financial modeling, finance, Excel, business valuation, budgeting/forecasting, PowerPoint presentations, accounting and business strategy.

A well rounded financial analyst possesses all of the above skills!

Additional Questions & Answers

CFI is the global institution behind the financial modeling and valuation analyst FMVA® Designation. CFI is on a mission to enable anyone to be a great financial analyst and have a great career path. In order to help you advance your career, CFI has compiled many resources to assist you along the path.

In order to become a great financial analyst, here are some more questions and answers for you to discover:

- What is Financial Modeling?

- How Do You Build a DCF Model?

- What is Sensitivity Analysis?

- How Do You Value a Business?

Accounting Crash Courses

CFI is a global provider of financial modeling courses and of the FMVA Certification. CFI’s mission is to help all professionals improve their technical skills. If you are a student or looking for a career change, the CFI website has many free resources to help you jumpstart your Career in Finance. If you are seeking to improve your technical skills, check out some of our most popular courses. Below are some additional resources for you to further explore:

The Financial Modeling Certification

Boost your confidence and master accounting skills effortlessly with CFI’s expert-led courses! Choose CFI for unparalleled industry expertise and hands-on learning that prepares you for real-world success.