Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

Cash Flows available to Funding Providers

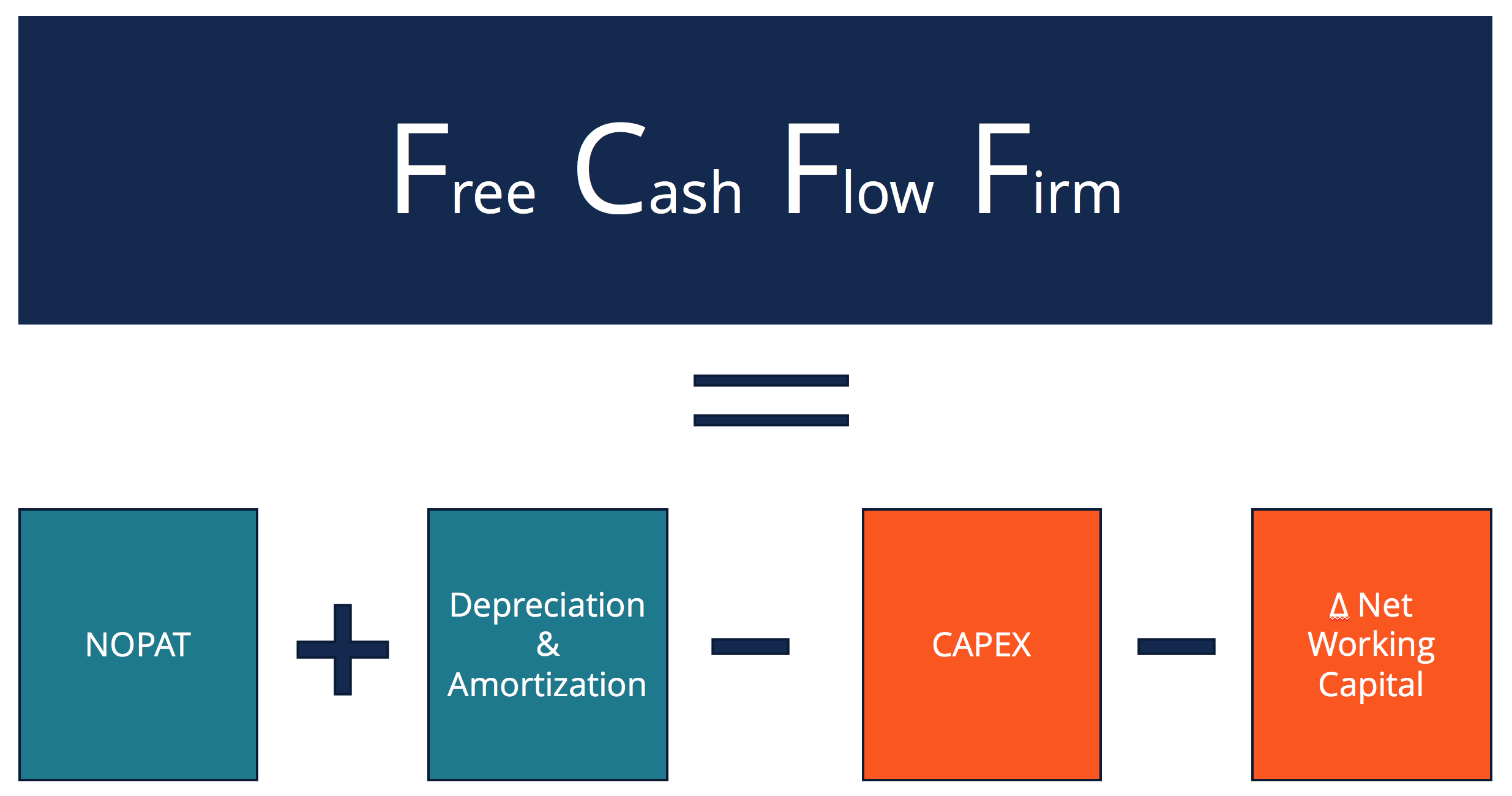

FCFF, or Free Cash Flow to Firm, is the cash flow available to all funding providers (debt holders, preferred stockholders, common stockholders, convertible bond investors, etc.). It is also known as unlevered free cash flow and represents the surplus cash flow available to a business if it were debt-free.

A common starting point for calculating it is Net Operating Profit After Tax (NOPAT), which can be obtained by multiplying Earnings Before Interest and Taxes (EBIT) by (1-Tax Rate). From that, we remove all non-cash expenses and the effects of CapEx and changes in Net Working Capital, as core operations are the focus.

To arrive at the FCFF figure, a Financial Analyst will need to undo the work that the accountants have done. The objective is to get the true cash inflows and outflows of the business.

FCFF is an important part of the Two-Step DCF Model, which is an intrinsic valuation method. The second step, where we calculate the terminal value of the business, may use the FCFF with a terminal growth rate, or more commonly, we may use an exit multiple and assume the business is sold.

DCF Analysis is a valuable Business Valuation technique, as it evaluates the intrinsic value of the business by looking at the cash-generating ability of the business. Conversely, Comps and Precedent Transactions both use a Relative Valuation approach, which is common in Private Equity, due to restricted access to information.

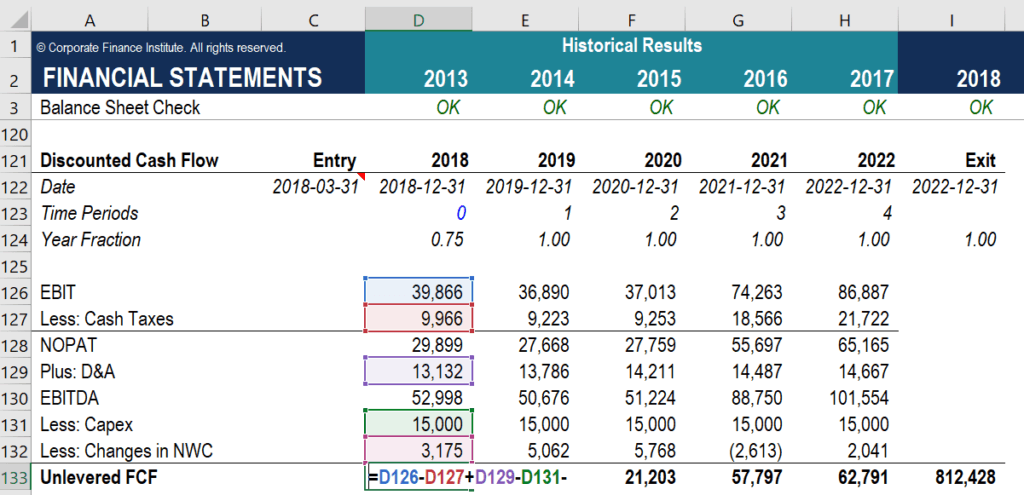

Below is a quick snippet from our Business Valuation Modeling Course, which includes a step-by-step guide to building a DCF Model. Part of the two-step DCF Model is to calculate the FCFF for projected years.

Image: Business Valuation Modeling Course

FCFF = NOPAT + D&A – CAPEX – Δ Net WC

Where:

So, using the numbers from 2018 on the image above, we have NOPAT, which is equivalent to EBIT less the cash taxes, equal to 29,899. We add D&A, which are non-cash expenses to NOPAT, and get a total of 43,031.

We then subtract any changes to CAPEX, in this case, 15,000, and get to a subtotal of 28,031. Lastly, we subtract all the changes to net working capital, in this case, 3,175, and get an FCFF value of 24,856.

When a Financial Analyst is modeling a business, they might only have access to partial information from certain sources. This is particularly true in Private Equity, as private companies do not have the rigorous reporting requirements that public companies do. Here are some other equivalent formulas for calculating the FCFF.

FCFF = NI + D&A +INT(1 – TAX RATE) – CAPEX – Δ Net WC

FCFF = CFO + INT(1-Tax Rate) – CAPEX

Where:

EBIT*(1 – Tax Rate) + D&A – Δ Net WC – CAPEX

Where:

FCFF vs FCFE or Unlevered Free Cash Flow vs Levered Free Cash Flow. The difference between the two stems from the fact that Free Cash Flow to Firm excludes the impact of interest payments and net increases/decreases in debt, whereas these items are included in FCFE.

Free Cash Flow to Equity is also a popular way to assess a business’s performance and cash-generating ability, specifically for equity investors. It is especially used in Leveraged Buyout (LBO) models.

Watch this short video to quickly understand the different types of cash flow commonly seen in financial analysis, including Earnings Before Interest, Tax, Depreciation & Amortization (EBITDA), Cash Flow (CF), Free Cash Flow (FCF), Free Cash Flow to the Firm (FCFF), and Free Cash Flow to Equity (FCFE).

Connect what you just learned to a clear career path with CFI’s role‑based courses and certification programs.

Thank you for reading this guide to Free Cash Flow to Firm. CFI offers an industry-specific course that walks you through how to build a DCF valuation model for the Mining industry. Here are some other CFI resources: