Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

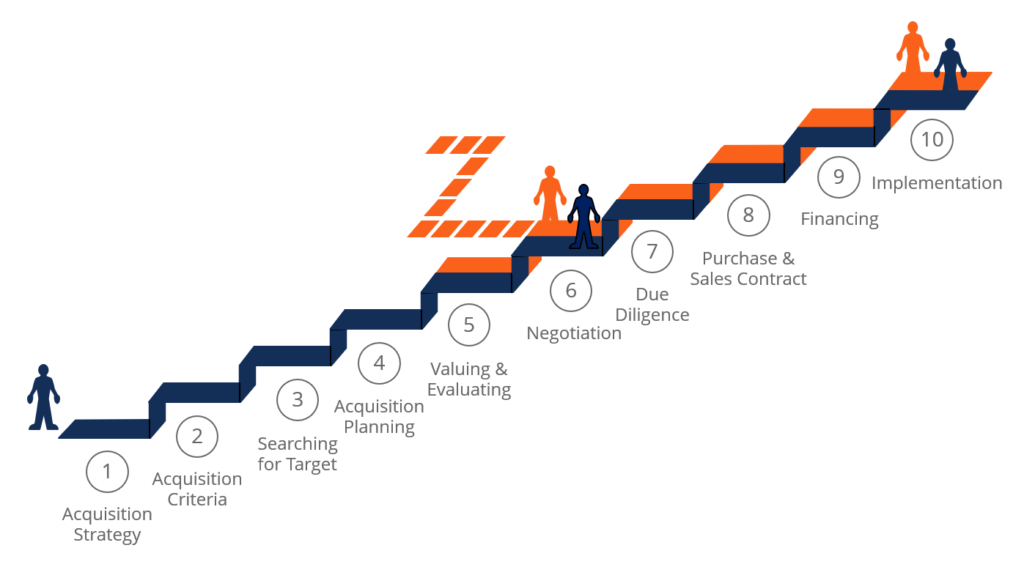

This guide outlines all the steps in the M&A process

The mergers and acquisitions (M&A) process has many steps and can often take anywhere from six months to several years to complete. In this guide, we’ll outline the acquisition process from start to finish, describe the various types of acquisitions (strategic vs. financial buys), discuss the importance of synergies (hard and soft synergies), and identify transaction costs. To learn all about the M&A process, watch our free video course on mergers and acquisitions.

If you work in either investment banking or corporate development, you’ll need to develop an M&A deal process to follow. Investment bankers advise their clients (the CEO, CFO, and corporate development professionals) on the various M&A steps in this process.

A typical 10-step M&A deal process includes:

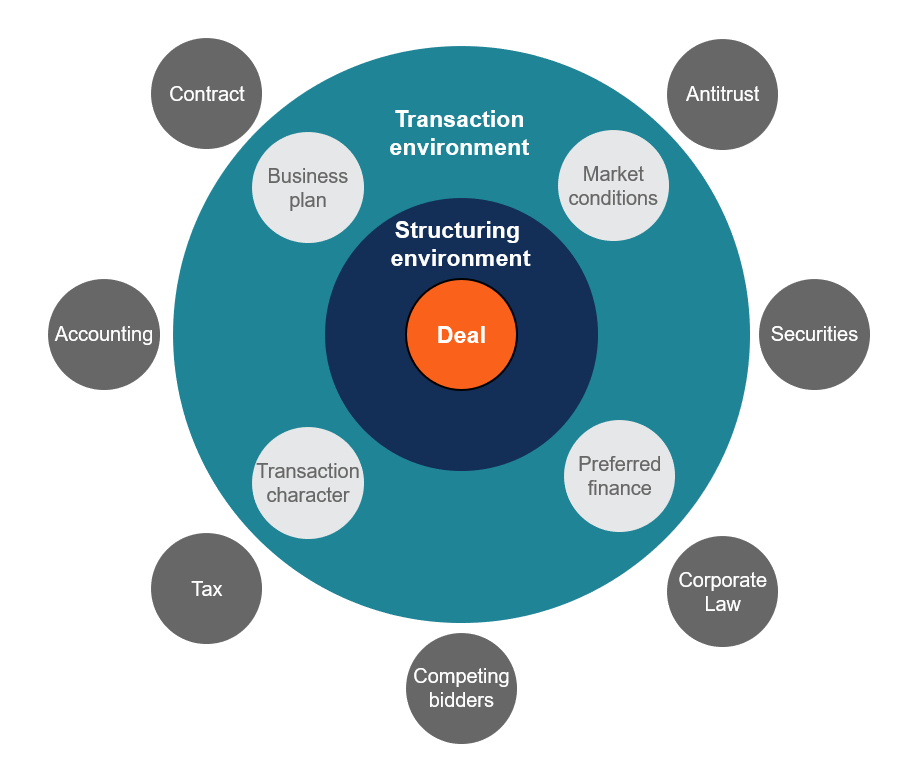

One of the most complicated steps in the M&A process is properly structuring the deal. There are many factors to be considered, such as antitrust laws, securities regulations, corporate law, rival bidders, tax implications, accounting issues, market conditions, forms of financing, and specific negotiation points in the M&A deal itself.

Important documents when structuring deals are the Term Sheet (used for raising money) and a Letter of Intent (LOI), which lays out the basic terms of the proposed deal.

To learn more, watch CFI’s free Corporate Finance 101 course.

The vast majority of acquisitions are competitive or potentially competitive. Companies normally have to pay a “premium” to acquire the target company, and this means having to offer more than rival bidders.

To justify paying more than rival bidders, the acquiring company needs to be able to do more with the acquisition than the other bidders in the M&A process can (i.e., generate more synergies or have a greater strategic rationale for the transaction).

In M&A deals, there are typically two types of acquirers: strategic and financial. Strategic acquirers are other companies, often direct competitors or companies operating in adjacent industries, such that the target company would fit in nicely with the acquirer’s core business. Financial buyers are institutional buyers, such as private equity firms, that are looking to own, but not directly operate the acquisition target. Financial buyers will often use leverage to finance the acquisition, performing a leveraged buyout (LBO).

We discuss this in more detail in the M&A section of our Corporate Finance course.

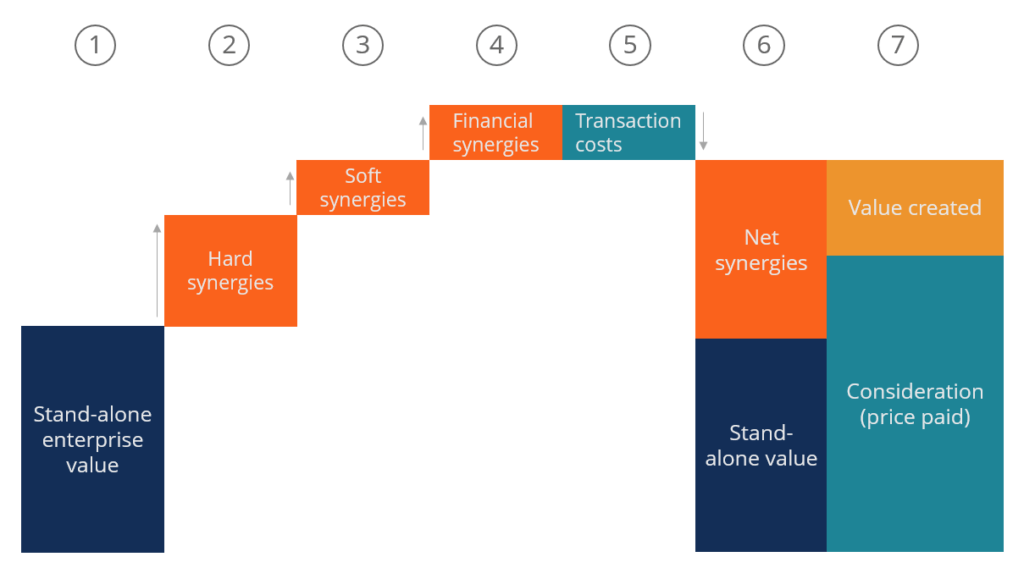

One of the biggest steps in the M&A process is analyzing and valuing acquisition targets. This usually involves two steps: valuing the target on a standalone basis and valuing the potential synergies of the deal. To learn more about valuing the M&A target see our free guide on DCF models.

When it comes to valuing synergies, there are two types of synergies to consider: hard and soft. Hard synergies are direct cost savings to be realized after completing the merger and acquisition process. Hard synergies, also called operating or operational synergies, are benefits that are virtually sure to arise from the merger or acquisition – such as payroll savings that will come from eliminating redundant personnel between the acquirer and target companies.

Soft synergies, also called financial synergies, are revenue increases that the acquirer hopes to realize after the deal closes. They are “soft” because realizing these benefits is not as assured as the “hard” synergy cost savings. Learn more about the different types of synergies.

To learn more, check out CFI’s Introduction to Corporate Finance course.

The most common career paths to participate in M&A deals are investment banking and corporate development. Investment bankers advise their clients on either side of the acquisition, either the acquirer (buy-side) or the target (sell-side).

The bankers work closely with the corporate development professionals at either company. The Corp Dev team at a company is like an in-house investment banking department, and sometimes is referred to internally as the M&A team. They are responsible for managing the M&A process from start to finish.

To learn more, explore our Interactive Career Map.

Connect what you just learned to a clear career path with CFI’s role‑based courses and certification programs.

We hope this has been a helpful overview of the various steps in the M&A process. CFI has created many more useful resources to help you more thoroughly understand mergers and acquisitions. Among our most popular resources are the following articles: