Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

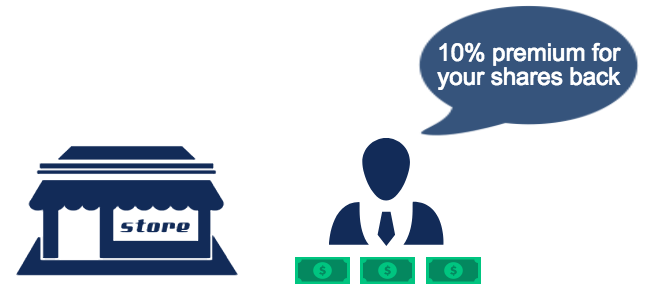

A share buyback by the target company in a hostile takeover

Committing Greenmail involves buying a significant number of shares in a target company, threatening a hostile takeover, and then using the threat to force the target company to buy back the shares at a higher price. Similar to blackmail, greenmail is money that is paid to another company to prevent aggressive behavior (i.e., an unwanted takeover).

There are four basic steps to committing Greenmail:

The practice was significantly prominent in the 1980s. Between April 1983 and April 1984 alone, companies paid over US$4 billion in greenmail.

Carl Icahn is widely considered one of the most notorious greenmailers of all time, due to several transactions he was behind in the ’80s.

Greenmail, which is a challenging situation for target companies, presents two choices:

Often, target companies will purchase back the shares at a premium to prevent a hostile takeover.

For example, Company A buys 20% shares of Company B and then threatens a takeover. The management of Company B, without any other options, buys back the shares at a premium in order to avoid being taken over. Company A makes a significant gain through the resale of the shares at a premium back to Company B and Company B loses a significant amount of money.

Due to the wave of greenmails in the 1980s, several states in the US adopted statutes that prohibit companies from paying greenmail.

For example:

In addition, under Section 5881 of the Internal Revenue Code, a 50% excise tax is payable from the profit generated from a greenmail. However, since the practice is not well-defined, the excise tax is easily avoided.

One famous example involved Goodyear Company and Sir James Goldsmith. In 1986, Sir James Goldsmith held an 11.5% stake (at an average of $42.20 per share) in Goodyear Company and threatened to take over the company for $4.7 billion ($49 per share).

In response, Goodyear agreed to repurchase the existing shares from Sir James for $49.50 per share ($620.7 million) contingent that Sir James refrain from purchasing any Goodyear stock for 5 years. In the end, Sir James made about $93 million in profit.

Additionally, to prevent another takeover attempt in the future, Goodyear offered to repurchase 40 million shares, with 109 million shares outstanding, at $50 per share, in an open offer to all shareholders. Ultimately, the purchase of 40 million shares cost Goodyear $2.6 billion.

To continue learning and advance your career, see the following free CFI resources:

Below is a break down of subject weightings in the FMVA® financial analyst program. As you can see there is a heavy focus on financial modeling, finance, Excel, business valuation, budgeting/forecasting, PowerPoint presentations, accounting and business strategy.

A well rounded financial analyst possesses all of the above skills!

CFI is the global institution behind the financial modeling and valuation analyst FMVA® Designation. CFI is on a mission to enable anyone to be a great financial analyst and have a great career path. In order to help you advance your career, CFI has compiled many resources to assist you along the path.

In order to become a great financial analyst, here are some more questions and answers for you to discover: