Get Specialized with our Financial Planning & Analysis (FP&A) Program

Support business leaders in their decision-making with best-in-class financial models to evaluate and forecast the financial performance of a company.

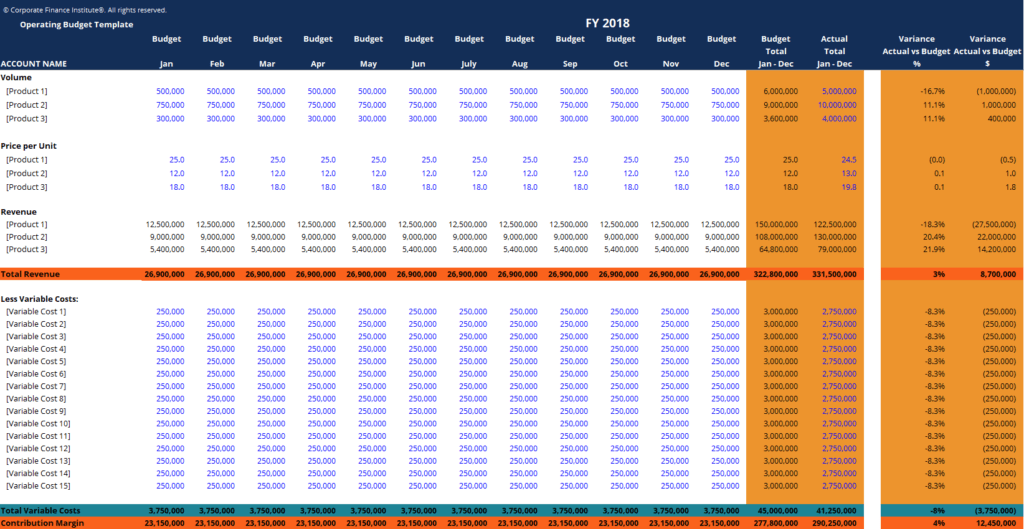

Download an operating budget template

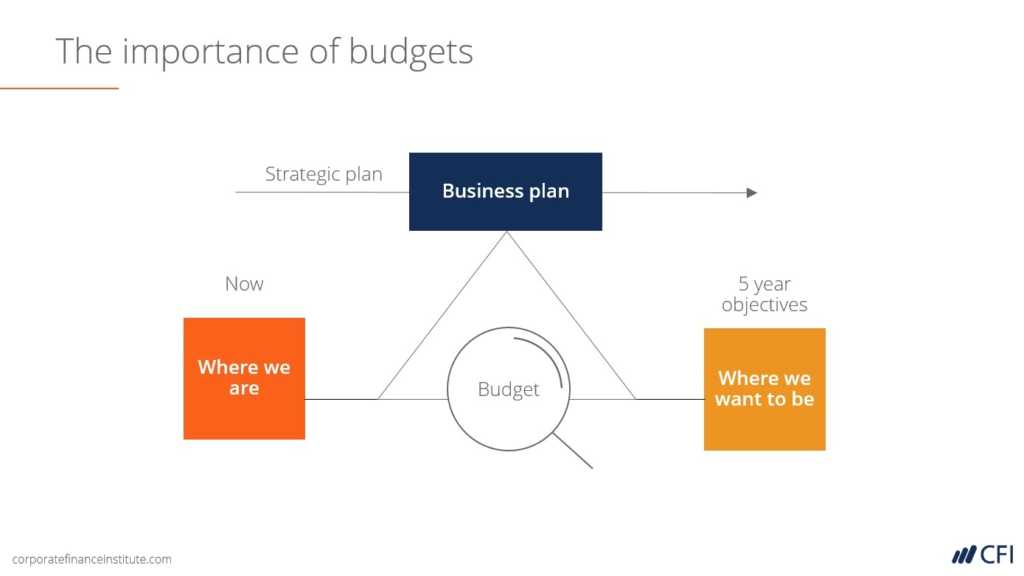

An operating budget consists of all revenues and expenses over a period of time (typically a quarter or a year) that a corporation, government (see the U.S. 2017 Budget), or organization uses to plan its operations.

An operating budget is prepared in advance of a reporting period as a goal or plan that the business expects to achieve. Below is an example of a downloadable budget template and an explanation of how to prepare one.

Download the free Excel template now to advance your finance knowledge.

The main components of an operations budget are outlined below. Each business is unique and every industry has its nuances, but these items are general enough to apply to most industries.

Revenue is usually broken down into its drivers and components. It’s possible to forecast revenue on a year-over-year basis, but usually, more detail is required by breaking revenue down into its underlying components.

Revenue drivers typically include:

After revenue, variable costs are determined. These costs are called “variable” because they depend on revenue and are often calculated as a percentage of sales.

Variable costs often include:

Read more about variable and fixed costs.

After variable costs are deducted, fixed costs are usually next. These expenses typically do not vary with changes in revenue and are mostly constant, at least within the time frame of the operating budget.

Examples of fixed costs include:

An operating budget often includes non-cash expenses, such as depreciation and amortization. Even though these expenses don’t impact cash flow (other than taxes), they will impact financial reporting performance (i.e., the figures a company reports at the end of the year on its income statement).

Non-operating expenses are those that fall below Earnings Before Interest and Taxes (EBIT) or Operating Income. Examples of expenses that may be included in a budget are:

Capital costs are usually excluded from an operating budget. The term operating refers to a statement of operations (income statement) that excludes capital expenditures.

Most companies prepare a separate budget for capital investments.

Below is a short video that explains the various types of budgets, what they’re used for, and why they matter to corporations. You’ll quickly learn the differences between the three main types of budgets (operating, capital, and cash).

Connect what you just learned to a clear career path with CFI’s role‑based courses and certification programs.