IB Pitchbook – Valuation Analysis

Download our free Investment Banking Pitchbook Template

Valuation Analysis Template

The valuation component is generally the most important piece of information for a company that is seeking to pursue an M&A transaction. Both parties in a potential deal perform a thorough valuation analysis to maximize their gains from the transaction. On the acquirer’s side, investment bankers will seek to sell their recommendations by highlighting the impact on valuation following an accretive transaction and an attractive valuation of the target.

For a company looking to sell, investment bankers will seek to show the most attractive valuation possible to the selling company and list any potential buyers to win the deal. The valuation analysis component can vary greatly in length, as well as the level of detail. The following points are some of the common denominators often found in the valuation analysis section of a typical M&A pitchbook.

Download the Template

Transaction Rationale

The transaction rationale is a textual summary of the merits of pursuing a transaction. For M&A, the key points to highlight are any synergies to be gained, accretion/dilution, proforma financial metrics, and any other strategic considerations. For an IPO, the summary should cover key valuation assumptions, timing considerations, key financial sponsors, and high-level rationale for going public. Regardless of the type of corporate finance transaction, preparing a concise transaction summary helps focus attention and communicate the most important considerations for pursuing your bank’s recommendation.

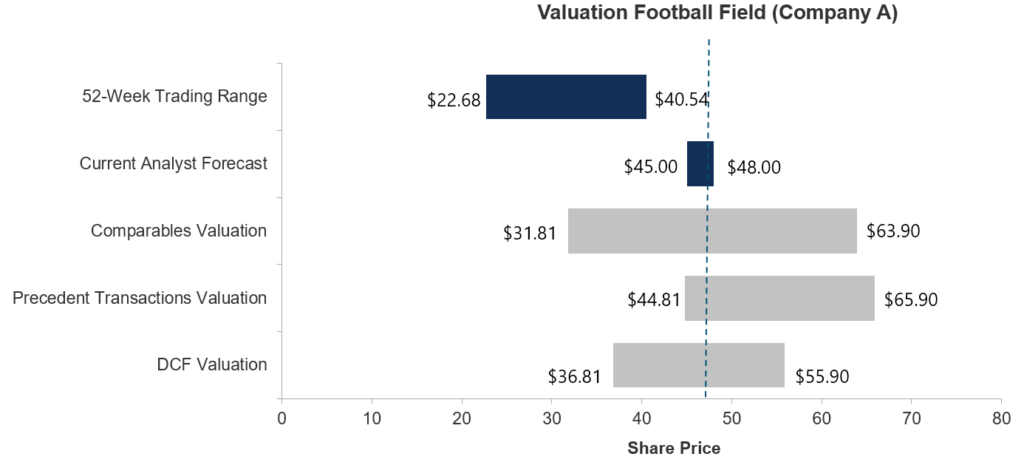

The Football Field Graph

The football field graph is a summary of the company’s valuation that utilizes different methodologies. This is typically an average of the company’s trading range (if public), analyst consensus (if public), comparable multiples valuation, precedent transaction valuation, and the discounted cash flow valuation. The graph will ultimately allow the senior bankers to decide which method to use to achieve the most attractive valuation to display. The ranges for each valuation method derives from the median, best- and worst-case scenarios. Once a blended average valuation is reached, it is best practice to show the valuation in both price format as well as multiple formats, using the multiples that are most appropriate to the industry. Each individual valuation method will be discussed in greater detail in this teaching series.

Analyst Consensus

Relatively speaking, equity research analysts that publish earnings estimates and target prices have the most expertise and the most extensive resources available to study the companies in their coverage universe. Therefore, it is prudent to consider these estimates with the other valuation outputs to form a holistic conclusion. Equity research reports will frequently include tear sheets of analysts’ models, and we can see further granularity in the relevant financial and operating metrics. Investment bankers will often include analyst consensus averages in the forecast periods when building financial models for their client companies.

Sell-Side vs. Buy-Side M&A Pitchbooks

A sell-side M&A pitchbook is typically constructed when a company solicits an investment bank with the intent of selling themselves, looking for potential buyers. A buy-side M&A pitchbook is the inverse scenario, where a company solicits an investment bank with the intent of purchasing another company. In the former situation, the valuation overview will display the client’s valuation, whereas the latter will display the valuations of potential acquisition targets.

In a sell-side M&A pitchbook, it is significantly more important to showcase the client’s valuation in the most attractive light possible. Intuitively, there is an implicit trade-off associated with this deal. As an investment bank, the primary objective of a winning business must be balanced with the capacity to fulfill the company’s objective of selling themselves. An overly rich valuation may win your bank the business, but the ability to materialize the transaction is constrained. An overly conservative valuation may result in the company choosing a different bank to represent them. This is the balancing act that investment bankers constantly perform.

Additional Resources

Thank you for downloading CFI’s free pitchbook template. To keep learning and advancing your career, the following resources will be helpful:

Analyst Certification FMVA® Program

Below is a break down of subject weightings in the FMVA® financial analyst program. As you can see there is a heavy focus on financial modeling, finance, Excel, business valuation, budgeting/forecasting, PowerPoint presentations, accounting and business strategy.

A well rounded financial analyst possesses all of the above skills!

Additional Questions & Answers

CFI is the global institution behind the financial modeling and valuation analyst FMVA® Designation. CFI is on a mission to enable anyone to be a great financial analyst and have a great career path. In order to help you advance your career, CFI has compiled many resources to assist you along the path.

In order to become a great financial analyst, here are some more questions and answers for you to discover:

- What is Financial Modeling?

- How Do You Build a DCF Model?

- What is Sensitivity Analysis?

- How Do You Value a Business?