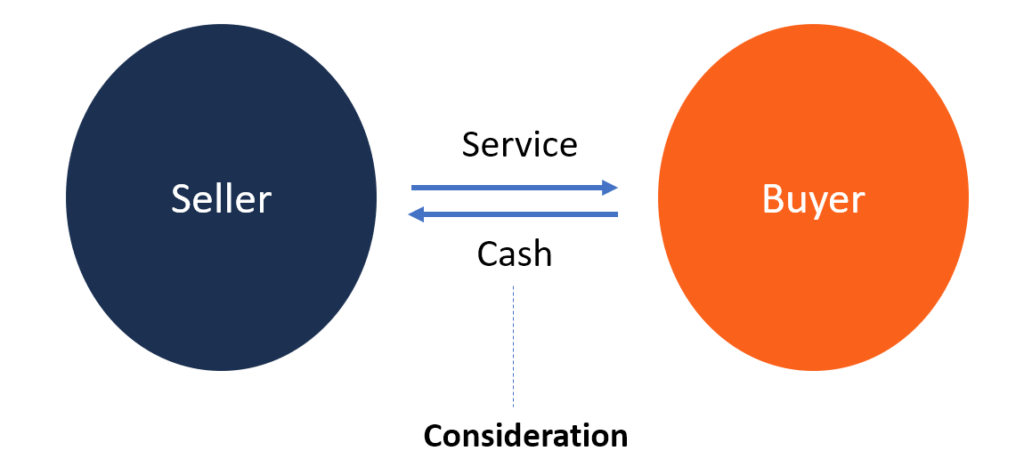

Consideration

The price paid in exchange for the fulfillment of a promise

What does Consideration mean?

The term “consideration” is a concept in English law that refers to the price paid in exchange for the fulfillment of a promise. The court in the case of Currie v Misa defined consideration as a right, interest, profit, detriment, loss, or responsibility. Its main characteristic is that the promissor must give a promise of something that is of value, and the promisee must give something of value in exchange. In simple terms, anything of value that is promised by one party to another can be viewed as a consideration. In finance, this term is commonly used in mergers & acquisitions (M&A).

For a contract to be valid, there must be an offer, acceptance, and consideration. If a person makes an offer to another person without any consideration, the contract is not binding. The law does not offer a reprieve to a contract that does not include an exchange of promise without offering any consideration in return. The promisor must offer a consideration in order to acquire something of value that is being offered by the promisee. The promisee must accept the consideration being offered before the exchange takes place.

Is consideration always money?

There are many writings and court judgments on what constitutes consideration. Most contracts use money, but it does not mean that other objects or services cannot be accepted. Most legal cases and writings agree that it must be something of value and can vary from money to items of art or other objects.

The monetary value of consideration

Fairness

When two parties enter into a valid contract, the courts do not typically question whether the consideration offered was fair in monetary terms. The courts are only concerned with its presence rather than its fairness. The parties in the transaction must be competent to execute the transaction for the courts to uphold the transaction. For example, both parties must have attained the majority age and be of sound mind. The contract must also constitute an offer and acceptance.

Nominal consideration

In the United States, some contracts allow the parties to pass nominal amounts of consideration that only cite $1. This is most common with contracts that do not involve any money as part of the consideration. Other forms of consideration can include stocks of the company, assets, or other accepted objects. However, some US courts may not be amenable to such contracts or those with virtually no monetary component. Some courts have ruled that such a practice is not a sufficient legal duty and, therefore, does not constitute a valid contract.

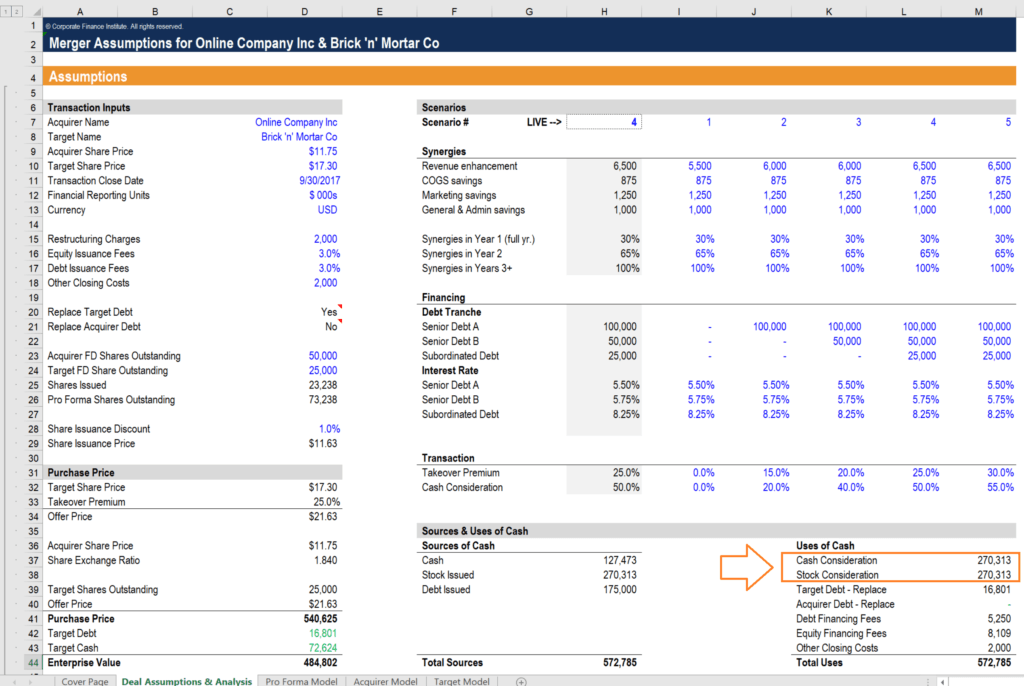

Example in Financial Modeling

Below is a screenshot from CFI’s M&A Financial Modeling Course which shows the total consideration provided to the seller of a business. In this case, the buyer offers the seller a combination of cash and stock to complete the deal.

Pre-existing legal duties in consideration

A party that has already entered into a contract has a legal duty to provide money, objects, or service, does not provide consideration for the sole reason of upholding that duty. The legal duty arises from an agreement in a previous contract, or from legal requirements of the contract.

For example, assume that two parties, A and B, enter into a contract for the renovation of a house. A offers to renovate B’s house for $1,000, which includes painting, replacing doorknobs, and replacing the kitchen shelves. B agrees to the terms of the contract and gives the green light for B to proceed with the contract.

However, halfway through the contract, A raises the price to $1,500 after he realizes that the renovation will take longer than he had expected. B agrees to the new terms and A goes ahead with the work. When A has finished the work, B only needs to pay A the $1,000 that they had initially agreed since A has a legal duty in the previous contract to renovate the house at that agreed price.

U.S. legislation

For a contract to be legally enforceable under U.S. laws, it must fulfill three characteristics. First, there must be a bargain on the subject of the contract where both parties agree to a common understanding. Second, there must be a mutual exchange where each party in the contract gets something out of the contract. Lastly, the subject of the contract must be something of value.

The elements of consideration can be demonstrated in the tenant-landlord agreement. First, these parties must discuss the terms of the agreement such as price, the condition of the apartment, deposits, etc. Secondly, each of the parties in the tenant-landlord agreement must benefit from the contract. The tenant provides rental payments and gets an apartment to live in, while the landlord provides the apartment and gets regular rental payments. Lastly, the apartment must be worth the amount that the tenant pays on a regular basis.

More resources

CFI is a global provider of financial analyst training and career advancement for finance professionals, including the global Financial Modeling & Valuation Analyst (FMVA)™ certification program. To keep advancing your career, the additional CFI resources below will be useful:

Analyst Certification FMVA® Program

Below is a break down of subject weightings in the FMVA® financial analyst program. As you can see there is a heavy focus on financial modeling, finance, Excel, business valuation, budgeting/forecasting, PowerPoint presentations, accounting and business strategy.

A well rounded financial analyst possesses all of the above skills!

Additional Questions & Answers

CFI is the global institution behind the financial modeling and valuation analyst FMVA® Designation. CFI is on a mission to enable anyone to be a great financial analyst and have a great career path. In order to help you advance your career, CFI has compiled many resources to assist you along the path.

In order to become a great financial analyst, here are some more questions and answers for you to discover:

- What is Financial Modeling?

- How Do You Build a DCF Model?

- What is Sensitivity Analysis?

- How Do You Value a Business?