Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

The fiduciary duty of the board of directors of securing the highest value for their shareholders

The Revlon Rule addresses conflicts of interest where the interests of the board of directors conflict with their fiduciary duty. Specifically, the Revlon Rule arose out of a hostile takeover. Prior to the takeover itself, the duty of the board of directors is to protect the company against the takeover. Once the takeover is considered imminent, however, their fiduciary duty switches to one of assuring the highest value for their stakeholders.

In most cases, after a hostile takeover, a majority of the directors lose their jobs. As a result, they continue to oppose efforts of a hostile takeover. They try to look for friendlier takeover terms, perhaps attempting to secure a white knight offer. That practice, however, may conflict with their fiduciary duty of securing the highest value for their shareholders.

In an effort to protect their welfare, the directors might reject an offer with high returns on the stock investment in favor of a lower bidder who promises them a secure job package or a golden parachute. While, historically, the law protected the actions of the directors, the Revlon Rule set the legal precedent for where a director’s fiduciary duty lies in such situations.

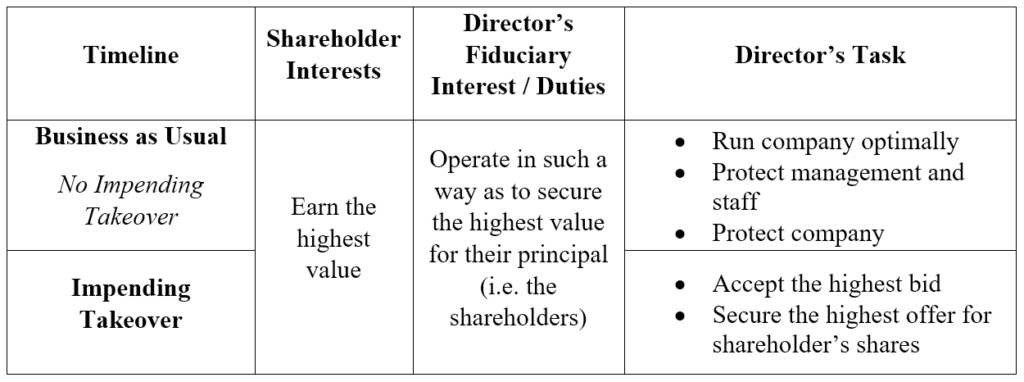

To demonstrate the Revlon Rule, directors can take on two specific roles. The first role is that of a custodian, where directors are tasked with a duty of care towards the company, its management, and staff. The duty of directors is to always ensure shareholders are earning their highest value. When it’s “business as usual” and no takeovers are impending, it means ensuring that the company is operating at its best and that the company is shielded from any such takeovers.

The second role is that of an auctioneer. When a takeover is all but guaranteed, the duty of the directors switches to literally finding the highest value for the company’s shareholders. Directors must try to sell the company to the highest bidder.

Revlon, Inc. v. MacAndrews & Forbes Holding, Inc.

The famous Revlon Rule case made clear the actions that directors should take as custodians and as auctioneers. In a hostile takeover, the decisions of the directors are subject to scrutiny since they can put the shareholders’ wealth at stake. Specifically, directors face conflicting duties of acting as auctioneers (highest value for the company) and custodians (best condition of the company).

In the 1985 case, Pantry Pride (MacAndrews & Forbes Holding, Inc) was interested in buying out Revlon, Inc. The takeover process was negotiated, but there was no concrete decision reached. As a result, Pantry Pride began a hostile takeover, but Revlon’s directors responded with a stock repurchase plan at a higher value than what the acquirer was offering. In the meantime, Revlon directors had started negotiating a friendly takeover with Forstmann Little & Co.

Pantry Pride became aggrieved by the actions of the directors and sued for an injunction against their actions. The company’s main point of argument was based on the fact that the directors initially refused to take a tender offer that would’ve benefitted the shareholders with a premium. At that time, Pantry Pride was offering to buy Revlon shares at $58, more than $10 above their market value.

In its ruling, the court concluded that the directors acted in the best interest of shareholders by initiating the stock repurchase. However, once they started negotiating for a friendly takeover, they acted for their own personal welfare and denied the shareholders the opportunity to get a premium return on their stocks.

The directors were initially properly performing their fiduciary duty, taking any actions necessary to protect against the hostile takeover. However, once a sale was imminent, the directors should have ensured that they maximize the welfare of the shareholders by getting the highest bidder with the best terms. In attempting to secure a friendlier takeover that would secure their own positions, the directors violated what is now known as the Revlon Rule.

The bottom line of the Revlon case is that in some cases the fiduciary duty for a director may be to actually accept the takeover. The Revlon Rule asserts that directors should act in the best interest of the shareholders, even if that means accepting the takeover. The current management may not be making full use of all available resources and are, thus, foregoing value to the shareholder should they choose to resist the takeover.

The target may face limited resources and is unable to exploit its full potential. Accepting a takeover may allow the company (and thus the shareholders) to earn more value.

The target company may be facing difficulties bailing itself out of its accumulated debt. A company may accept a takeover to ease its leverage.

The acquiring company might be doing well in the current market while the target is still using legacy systems (older, outdated). Digitization of operations increases profits.

Reducing the competition is more applicable if the acquiring company is in the same industry as the target. After merging operations, it will be one larger company serving the whole market.

Both the acquired and the acquirer might be involved in different sectors, and this creates diversification. For example, a company that sells umbrellas merging with a company that sells ice cream reduces seasonality risk and therefore secures additional value.

The Revlon Rule does not deter directors from taking any steps to protect the company from a hostile takeover. The directors are allowed to even employ a poison pill strategy, but they should only adopt it when success is probable.

If a hostile takeover becomes almost unavoidable, then at that point the directors should shift their efforts to negotiating a deal that will pay the highest amount to the company’s shareholders. The Revlon Rule outlines the impending hostile takeover as a time when directors should switch from the role of a custodian to that of an auctioneer.

CFI offers the Financial Modeling & Valuation Analyst (FMVA)™ certification program for those looking to take their careers to the next level. To keep learning and advancing your career, the following CFI resources will be helpful: