Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

"Statement of Owner’s Equity" or "Statement of Changes in Equity"

An equity statement – also referred to as a statement of owner’s equity or statement of changes in equity – is a financial statement that a company is required to prepare along with other important financial documents at the end of a reporting period. In the United States, the statement of changes in equity is also called the statement of retained earnings.

The statement of owner’s equity reports the changes in company equity. The changes that are generally reflected in the equity statement include the earned profits, dividends, inflow of equity, withdrawal of equity, net loss, and so on.

Equity, in the simplest terms, is the money shareholders have invested in the business. It constitutes a part of the total capital invested in the business, which doesn’t belong to debt holders.

On the company’s balance sheet, shareholders’ equity is represented under the heading “Shareholders’ Equity” or “Stockholders’ Equity.” The section usually comprises three components:

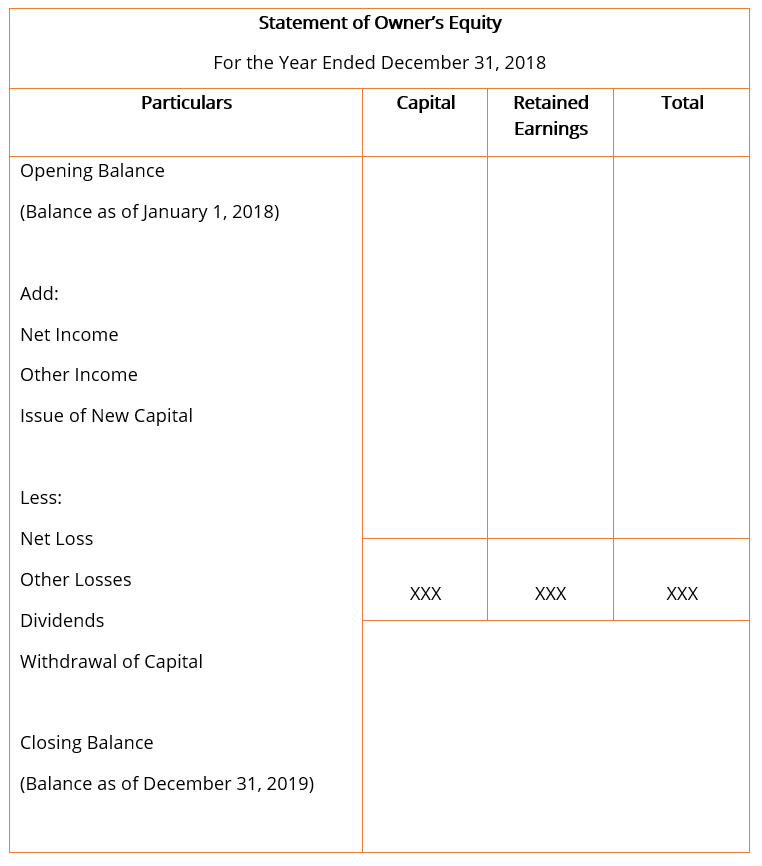

The general format for the statement of owner’s equity, with the most basic line items, usually looks like the one shown below.

Line Items

Line ItemsConnect what you just learned to a clear career path with CFI’s role‑based courses and certification programs.

Thank you for reading CFI’s guide to Equity Statement. To keep learning and advancing your career, the following resources will be helpful: