Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

Current Assets / Current Liabilities

The current ratio, also known as the working capital ratio, measures the capability of a business to meet its short-term obligations that are due within a year. The ratio considers the weight of total current assets versus total current liabilities.

It indicates the financial health of a company and how it can maximize the liquidity of its current assets to settle debt and payables. The current ratio formula (below) can be used to easily measure a company’s liquidity.

The Current Ratio formula is:

Current Ratio = Current Assets / Current Liabilities

If a business holds:

Current assets = 15 + 20 + 25 = 60 million

Current liabilities = 15 + 15 = 30 million

Current ratio = 60 million / 30 million = 2.0x

The business currently shows a current ratio of 2, meaning it can easily settle each dollar on loan or accounts payable twice. A rate of more than 1 suggests financial well-being for the company. There is no upper end on what is “too much,” as it can be very dependent on the industry, however, a very high current ratio may indicate that a company is leaving excess cash unused rather than investing in growing its business.

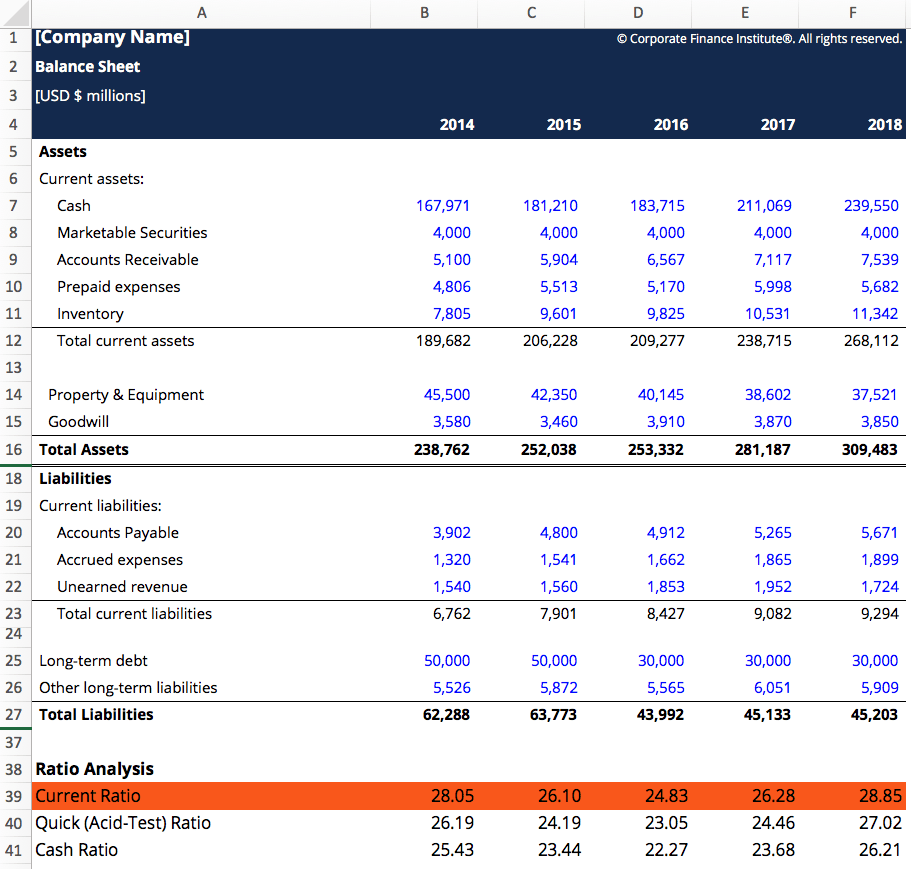

Image: CFI’s Financial Analysis Fundamentals Course

The current ratio measures liquidity using all current assets, but it differs from a company’s actual cash position—making liquidity vs cash position an important distinction.

Click the button below to download our free Current Ratio Formula template!

Current assets are resources that can quickly be converted into cash within a year’s time or less. They include the following:

Current liabilities are business obligations owed to suppliers and creditors, and other payments that are due within a year’s time. This includes:

This current ratio is classed with several other financial metrics known as liquidity ratios. These ratios all assess the operations of a company in terms of how financially solid the company is in relation to its outstanding debt. Knowing the current ratio is vital in decision-making for investors, creditors, and suppliers of a company. The current ratio is an important tool in assessing the viability of their business interest.

Other important liquidity ratios include:

Connect what you just learned to a clear career path with CFI’s role‑based courses and certification programs.

Thank you for reading CFI’s guide to understanding the Current Ratio Formula. To keep educating yourself and advancing your finance career, these CFI resources will be helpful: