Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

The price paid for a company as a function of a financial metric

An entry multiple, commonly used in leveraged buyouts, refers to the price paid for a company as a function of a financial metric. The entry multiple is crucial for private equity firms to know, as it helps them determine the purchase price of a company relative to a financial metric. It is ideal to purchase companies at a low entry multiple.

A multiple, also known as a multiplier, is a valuation technique that calculates the value of a business relative to a financial metric. Multiples are used to compare businesses operating in similar environments to determine whether a company is reasonably priced, compared to peers. There are numerous types of multiples that can be used, including EV/EBITDA, EV/Sales, EV/EBIT, EV/UFCF, and P/E multiples.

For example, if two companies operating in the same industry with similar business operations trade at P/E multiples of 10x and 4x respectively, ignoring other factors, the company with a 4x P/E multiple is deemed undervalued by investors.

Private equity firms use multiples to understand the price that they are paying for a company relative to a financial metric. For example, when a private equity firm is looking to purchase a company, they would want to compare the purchase price of the company relative to a financial metric – This is termed the “entry multiple.”

The most commonly used multiple for an entry multiple is EV/EBITDA. EV is enterprise value and typically represents the total value of a company. EBITDA is the earnings of a company before interest, taxes, depreciation, and amortization – the company’s operating income.

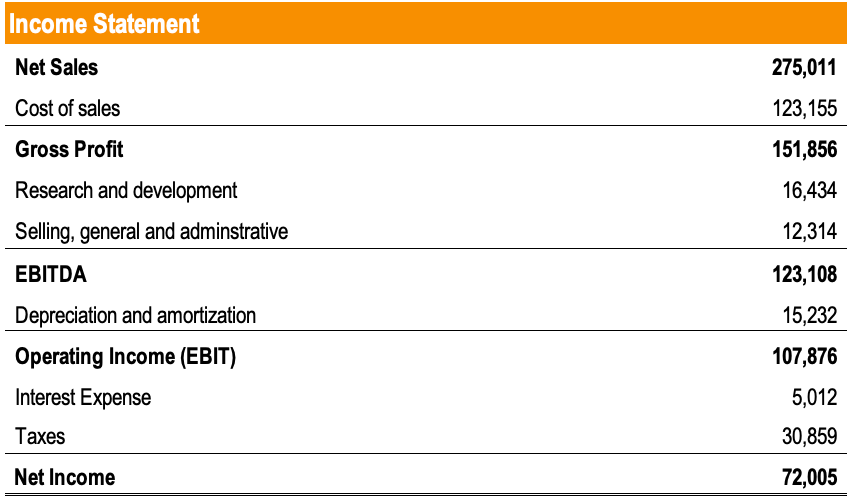

A private equity firm is looking to generate a 25% IRR in a leveraged buyout of a company. The firm must pay $500,000 to purchase the company. The income statement of the company is as follows:

Using the EV/EBITDA multiple, what is the implied entry multiple of this company?

The implied entry multiple of this company is $500,000/$123,108 = 4.06x.

An entry multiple is commonly used to compare to an exit multiple. Understanding that an entry multiple is the price paid for a company relative to a financial metric, an exit multiple is simply the sale price of a company relative to a financial metric.

For private equity firms, it is desirable to achieve a low entry multiple and a high exit multiple. Essentially, this means that the firm is purchasing the company at a low price relative to a financial metric and selling the company at a higher price relative to a financial metric.

For example, if a firm purchases a company with an EBITDA of $10M at a purchase price of $100M, and sells the company five years later at a sale price of $200M when the company has an EBITDA of $15M, the entry multiple is 10x (100M/10M), and the exit multiple is 13.3x (200M/15).

When the entry multiple is the same as the exit multiple, it means that the firm is purchasing and selling the company at the same relative value. In leveraged buyout models, a stable multiple is assumed.

For example, if a firm purchases a company at a purchase price of $100M with an EBITDA of $10M and sells the company five years later at a sale price of $200M with an EBITDA of $20M, the entry multiple is 10x (100M/10M), and the exit multiple is 10x (200M/20).

When the entry multiple is higher than the exit multiple, it means that the firm is purchasing the company at a higher price relative to a financial metric and is selling the company at a lower price relative to a financial metric. This is undesirable and compromises the IRR of the investment.

For example, if a firm purchases a company at a purchase price of $100M with an EBITDA of $10M and sells the company five years later at a sale price of $100M with an EBITDA of $20M, the entry multiple is 10x (100M/10M), and the exit multiple is 5x (100M/20).

CFI is the official provider of the global Financial Modeling & Valuation Analyst (FMVA)™ certification program, designed to help anyone become a world-class financial analyst. To keep advancing your career, the additional CFI resources below will be useful:

Below is a break down of subject weightings in the FMVA® financial analyst program. As you can see there is a heavy focus on financial modeling, finance, Excel, business valuation, budgeting/forecasting, PowerPoint presentations, accounting and business strategy.

A well rounded financial analyst possesses all of the above skills!

CFI is the global institution behind the financial modeling and valuation analyst FMVA® Designation. CFI is on a mission to enable anyone to be a great financial analyst and have a great career path. In order to help you advance your career, CFI has compiled many resources to assist you along the path.

In order to become a great financial analyst, here are some more questions and answers for you to discover: