Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

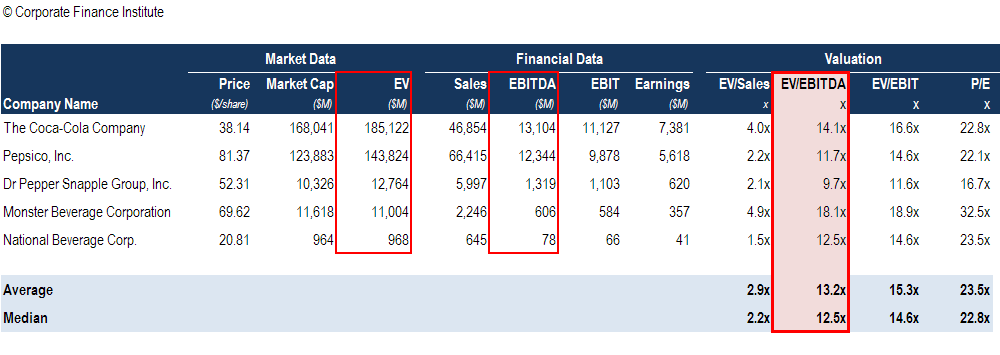

Facilitating an “apples to apples” comparison between EV and Total Sales, EBIT, or EBITDA

When a company owns more than 50% (but less than 100%) of a subsidiary, the company records all 100% of the subsidiary’s revenue, costs, and other income statement items, even though the company doesn’t own 100% of the subsidiary. Therefore, when you look at a company’s EV/EBITDA multiple, minority interest (the value of the subsidiary not owned by the parent) has to be added to EV since EBITDA includes 100% of the revenue and expenses from that subsidiary.

To learn more, launch CFI’s financial modeling and valuation courses now!

Enterprise Value or EV is a measure of a company’s worth. As a measure of company worth, it is superior to other measures, such as just Equity Market Capitalization, and also includes the Market Value of Debt and Minority Interest (now known as Noncontrolling Interest). Enterprise Value is often termed as the takeover price because, in the event of a takeover, EV is the effective selling price of the company.

The formula for Enterprise Value is as follows:

Enterprise Value = Market Value of Common Stock + Market Value of Preferred Equity + Market Value of Ddebt + Minority Interest – Cash

Minority interest, or noncontrolling interest (NCI), represents an ownership stake of less than 50% in a company (hence the term minority, or noncontrolling). For accounting purposes, noncontrolling interest is classified as equity and shows up on the balance sheet of the company that owns the majority interest in the subsidiary.

To learn more, launch CFI’s financial modeling and valuation courses now!

Per various accounting rules, when a company owns more than 50% of another company, then the parent company must usually consolidate its financial statements.

If company XYZ owns more than 50% (say 80%) of company ABC, then the financial statements of XYZ reflect all the assets and liabilities of ABC and 100% of the financial performance of ABC.

Thus, whether XYZ owns 50.1% or 100% of ABC, the financial statements of XYZ will show 100% of the assets and liabilities of ABC and 100% of the Sales, Revenue, Costs, Profits/Loss, etc. of ABC.

However, since the parent company (XYZ) does not own 100% of the subsidiary (ABC), XYZ’s income statement will specify the amount of net income that belongs to the minority shareholders. This account is called Noncontrolling Interest and is also reflected on the balance sheet, as the book value (not market value) of the subsidiary (ABC), the portion of which the parent (XYZ) does not own.

Enterprise Value is primarily used in Valuation Ratios such as EV/Total Sales, EV/EBIT, and EV/EBITDA.

Consider the example given above where XYZ owns 80% of ABC. As discussed above, because of accounting regulations, the consolidated financial statements of XYZ will reflect 100% of the Total Sales, EBIT, and EBITDA, etc. of the subsidiary ABC even though XYZ only owns 80% of ABC.

For these ratios to be meaningful, the numerator must be adjusted to allow for an “apples to apples” comparison between EV and Total Sales, EBIT, and EBITDA, etc. This is done by adding to Enterprise Value the equity value of the subsidiary that the parent company does not own (the noncontrolling interest). This results in both the numerator and denominator of the various valuation ratios accounting for 100% of the subsidiary company in terms of equity, Total Sales, EBIT, and EBITDA.

To learn more, read:

Another way in which we could arrive at a similar result is if we were to only include that proportion of Total Sales, EBIT, and EBITDA in the valuation ratios that the parent company (XYZ) owns in ABC.

If we do not wish to add the minority interest to Enterprise Value, we would only include 80% of ABC’s Total Sales, EBIT, and EBITDA in the calculation of the various valuation ratios.

The problem with this second method lies in the fact that companies are only required to supply one consolidated Financial Statement and do not provide separate financial statements of all their subsidiaries.

To learn more, launch CFI’s financial modeling and valuation courses now!

Connect what you just learned to a clear career path with CFI’s role‑based courses and certification programs.

We hope this has been a helpful guide to minority interest in enterprise value calculations. CFI is the official global provider of the Financial Modeling and Valuation Analyst (FMVA)® certification, designed to transform anyone into a world-class financial analyst.

If you’re interested in advancing your career in corporate finance, these articles will help you on your way: