Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

An increase or decease in money over a period of time

Cash Flow (CF) is the increase or decrease in the amount of money a business, institution, or individual has. In finance, the term is used to describe the amount of cash (currency) that is generated or consumed in a given time period. There are many types of CF, with various important uses for running a business and performing financial analysis. This guide will explore all of them in detail.

There are several types of Cash Flow, so it’s important to have a solid understanding of what each of them is. When someone refers to CF, they could mean any of the types listed below, so be sure to clarify which cash flow term is being used.

Types of cash flow include:

Cash Flow has many uses in both operating a business and in performing financial analysis. In fact, it’s one of the most important metrics in all of finance and accounting.

The most common cash metrics and uses of CF are the following:

Investors and business operators care deeply about CF because it’s the lifeblood of a company. You may be wondering, “How is CF different from what’s reported on a company’s income statement?” Income and profit are based on accrual accounting principles, which smooths-out expenditures and matches revenues to the timing of when products/services are delivered. Due to revenue recognition policies and the matching principle, a company’s net income, or net earnings, can actually be materially different from its Cash Flow.

Companies pay close attention to their CF and seek to manage it as carefully as possible. Professionals working in finance, accounting, and financial planning & analysis (FP&A) functions at a company spend significant time evaluating the flow of funds in the business and identifying potential problems.

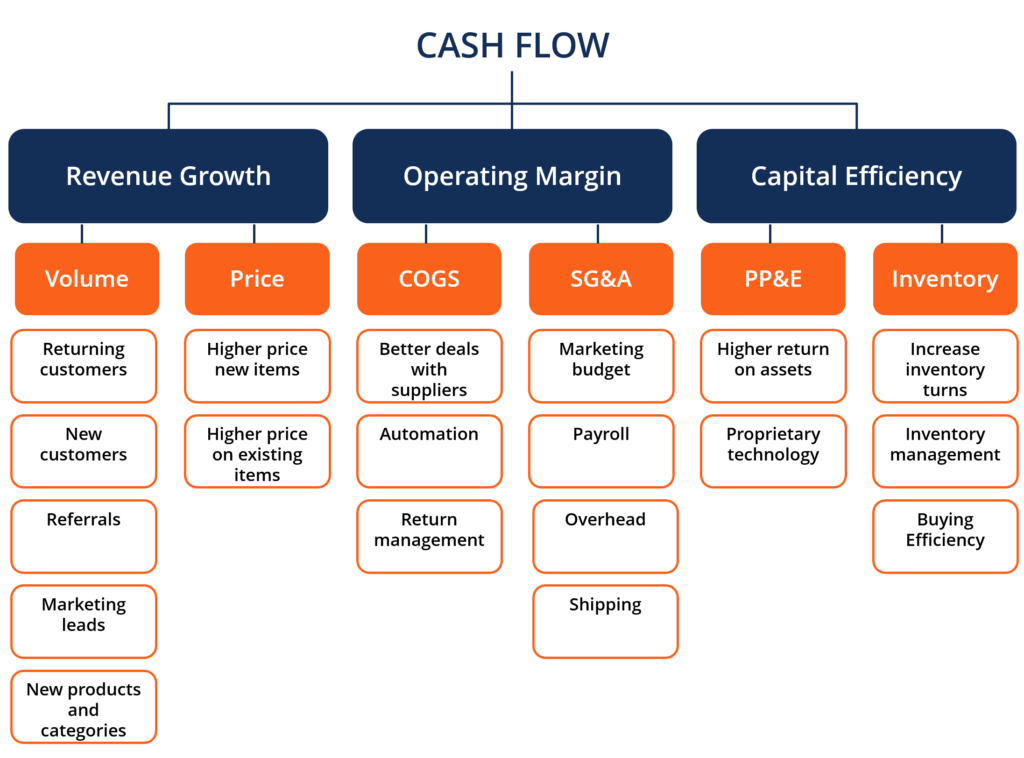

Since CF matters so much, it’s only natural that managers of businesses do everything in their power to increase it. In the section below, let’s explore how operators of businesses can try to increase the flow of cash in a company. Below is an infographic that demonstrates how CF can be increased using different strategies.

Managers of business can increase CF using any of the levers listed above. The strategies for improving CF fall into one of three categories: revenue growth, operating margins, and capital efficiency. Each of those can then be broken down into higher volume, higher prices, lower cost of goods sold, lower SG&A, more efficient property plant & equipment (PP&E), and more efficient inventory management.

Connect what you just learned to a clear career path with CFI’s role‑based courses and certification programs.

Thank you for reading CFI’s guide to Cash Flow. To keep learning and developing your knowledge of financial analysis, we highly recommend the additional CFI resources below: