Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

An Analyst's Guide to IRR

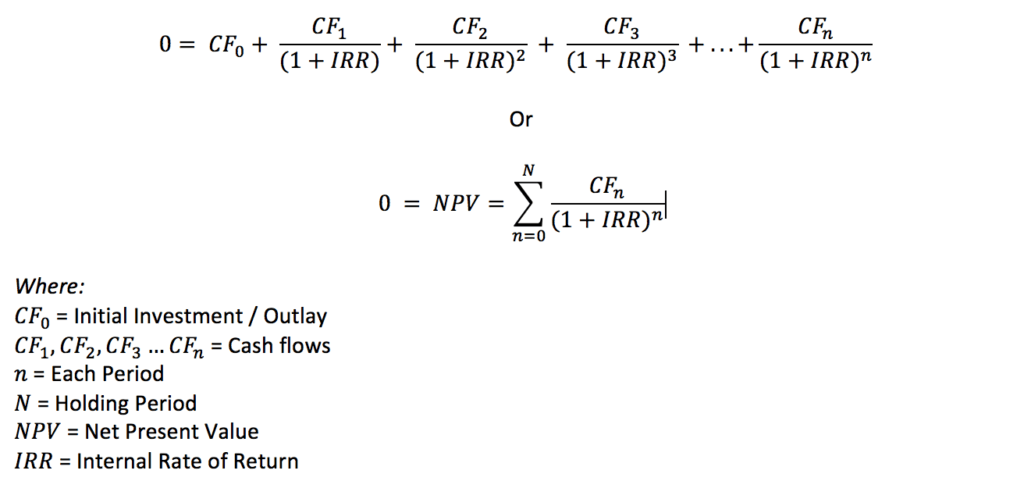

The Internal Rate of Return (IRR) is the discount rate that makes the net present value (NPV) of a project zero. In other words, it is the expected compound annual rate of return that will be earned on a project or investment.

When calculating IRR, expected cash flows for a project or investment are given and the NPV equals zero. Put another way, the initial cash investment for the beginning period will be equal to the present value of the future cash flows of that investment. (Cost paid = present value of future cash flows, and hence, the net present value = 0).

Once the internal rate of return is determined, it is typically compared to a company’s hurdle rate or cost of capital. If the IRR is greater than or equal to the cost of capital, the company would accept the project as a good investment. (That is, of course, assuming this is the sole basis for the decision.

In the example below, an initial investment of $50 has a 22% IRR. That is equal to earning a 22% compound annual growth rate.

In reality, there are many other quantitative and qualitative factors that are considered in an investment decision.) If the IRR is lower than the hurdle rate, then it would be rejected.

The IRR formula is as follows:

Calculating the internal rate of return can be done in three ways:

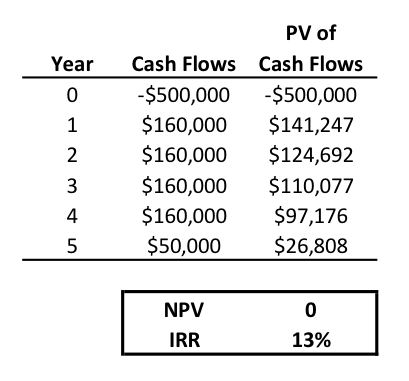

Here is an example of how to calculate the Internal Rate of Return.

A company is deciding whether to purchase new equipment that costs $500,000. Management estimates the life of the new asset to be four years and expects it to generate an additional $160,000 of annual profits. In the fifth year, the company plans to sell the equipment for its salvage value of $50,000.

Meanwhile, another similar investment option can generate a 10% return. This is higher than the company’s current hurdle rate of 8%. The goal is to make sure the company is making the best use of its cash.

To make a decision, the IRR for investing in the new equipment is calculated below.

Excel was used to calculate the IRR of 13%, using the function, =IRR(). From a financial standpoint, the company should make the purchase because the IRR is both greater than the hurdle rate and the IRR for the alternative investment.

Enter your name and email in the form below and download the free calculator/template now!

* By submitting your email address, you consent to receive email messages (including discounts and newsletters) regarding Corporate Finance Institute and its products and services and other matters (including the products and services of Corporate Finance Institute's affiliates and other organizations). You may withdraw your consent at any time.

This request for consent is made by Corporate Finance Institute, #1392 - 1771 Robson Street, Vancouver, BC V6G 3B7, Canada. www.corporatefinanceinstitute.com. [email protected]. Please click here to view CFI`s privacy policy.

Companies take on various projects to increase their revenues or cut down costs. A great new business idea may require, for example, investing in the development of a new product.

In capital budgeting, senior leaders like to know the estimated return on such investments. The internal rate of return is one method that allows them to compare and rank projects based on their projected yield. The investment with the highest internal rate of return is usually preferred.

Internal Rate of Return is widely used in analyzing investments for private equity and venture capital, which involves multiple cash investments over the life of a business and a cash flow at the end through an IPO or sale of the business.

Thorough investment analysis requires an analyst to examine both the net present value (NPV) and the internal rate of return, along with other indicators, such as the payback period, in order to select the right investment. Since it’s possible for a very small investment to have a very high rate of return, investors and managers sometimes choose a lower percentage return but higher absolute dollar value opportunity.

Also, it’s important to have a good understanding of your own risk tolerance, a company’s investment needs, risk aversion, and other available options.

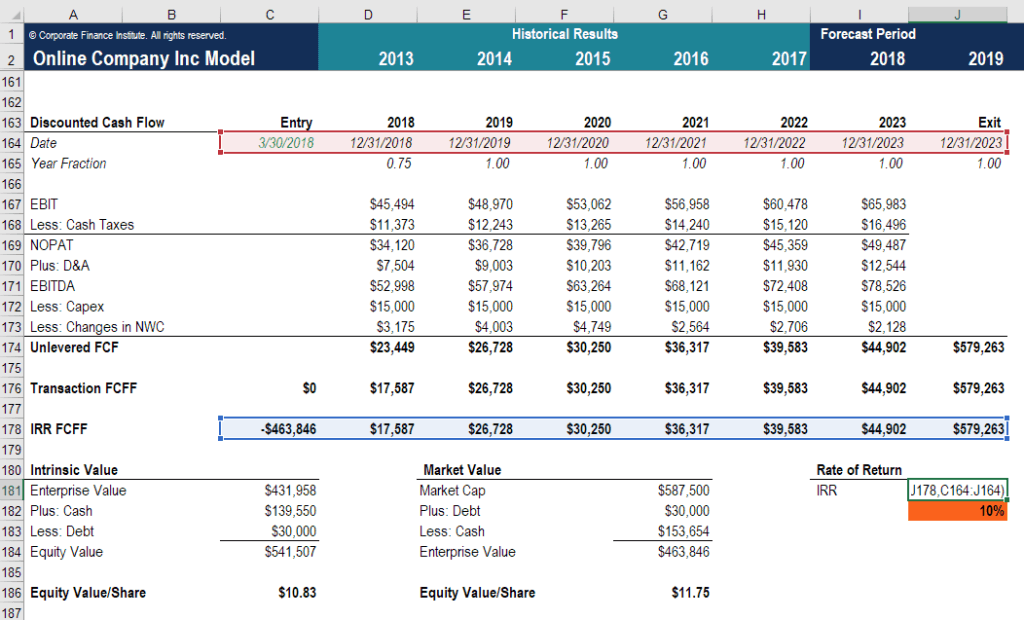

Let’s look at an example of a financial model in Excel to see what the internal rate of return number really means.

If an investor paid $463,846 (which is the negative cash flow shown in cell C178) for a series of positive cash flows as shown in cells D178 to J178, the IRR they would receive is 10%. This means the net present value of all these cash flows (including the negative outflow) is zero and that only the 10% rate of return is earned.

If the investors paid less than $463,846 for all the same additional cash flows, then their IRR would be higher than 10%. Conversely, if they paid more than $463,846, then their IRR would be lower than 10%.

The above screenshot is from CFI’s M&A Modeling Course.

Unlike net present value, the internal rate of return doesn’t give you the return on the initial investment in terms of real dollars. For example, knowing an IRR of 30% alone doesn’t tell you if it’s 30% of $10,000 or 30% of $1,000,000.

Using IRR exclusively can lead you to make poor investment decisions, especially if comparing two projects with different durations.

Let’s say a company’s hurdle rate is 12%, and one-year project A has an IRR of 25%, whereas five-year project B has an IRR of 15%. If the decision is solely based on IRR, this will lead to unwisely choosing project A over B.

Another very important point about the internal rate of return is that it assumes all positive cash flows of a project will be reinvested at the same rate as the project instead of the company’s cost of capital. Therefore, the internal rate of return may not accurately reflect the profitability and cost of a project.

A smart financial analyst will alternatively use the modified internal rate of return (MIRR) to arrive at a more accurate measure.

Thank you for reading CFI’s explanation of the Internal Rate of Return metric. CFI is the official global provider of the Financial Modeling & Valuation Analyst (FMVA)® designation. To learn more and help advance your career, see the following free CFI resources:

CFI is a global provider of financial modeling courses and of the FMVA Certification. CFI’s mission is to help all professionals improve their technical skills. If you are a student or looking for a career change, the CFI website has many free resources to help you jumpstart your Career in Finance. If you are seeking to improve your technical skills, check out some of our most popular courses. Below are some additional resources for you to further explore:

CFI is a global provider of financial modeling courses and of the FMVA Certification. CFI’s mission is to help all professionals improve their technical skills. If you are a student or looking for a career change, the CFI website has many free resources to help you jumpstart your Career in Finance. If you are seeking to improve your technical skills, check out some of our most popular courses. Below are some additional resources for you to further explore:

Below is a break down of subject weightings in the FMVA® financial analyst program. As you can see there is a heavy focus on financial modeling, finance, Excel, business valuation, budgeting/forecasting, PowerPoint presentations, accounting and business strategy.

A well rounded financial analyst possesses all of the above skills!

CFI is the global institution behind the financial modeling and valuation analyst FMVA® Designation. CFI is on a mission to enable anyone to be a great financial analyst and have a great career path. In order to help you advance your career, CFI has compiled many resources to assist you along the path.

In order to become a great financial analyst, here are some more questions and answers for you to discover: