NOPLAT

A company’s operating profit after adjusting to normalize for the impact of capital structure and deferred taxes

What is NOPLAT?

NOPLAT stands for Net Operating Profit Less Adjusted Taxes. It represents a company’s operating profit after adjusting to normalize for the impact of capital structure and deferred taxes.

![]()

The NOPLAT metric represents the earnings generated by a company after subtracting income taxes related to core operations and adding back overpaid taxes over the course of an accounting period. Both management and investors commonly use NOPLAT to calculate unlevered free cash flow or profit after taxes.

How to Calculate NOPLAT

The calculation of net operating profit less adjusted taxes can be done in various ways. For reference, some common formulas are seen below:

Uses of NOPLAT

NOPLAT is broadly used in corporate finance as an adjustment to the net income to represent the after-tax cash flows available to all capital providers of a company. NOPLAT is preferred instead of net income in discounted cash flow (DCF) models and leveraged buyout (LBO) models because it normalizes the effects of capital structure.

NOPLAT is an essential component of calculating free cash flows for DCF valuations in merger analysis. Especially when valuing target companies. Since it is a before-interest and after-tax metric, NOPLAT is an income measure that excludes the impact of debt financing, incorporating the cost of debt and the tax-shield benefit. As a result, it can be seen as a better measure of operating efficiency than net income. Simply put, NOPLAT represents how a company’s core operations performed, net of adjusted taxes.

Using NOPLAT, earnings can be measured without the impact of debt servicing or leverage on a company. In other words, the performance of different companies can be compared without being clouded by different capital structures. It makes NOPLAT useful in deriving the unlevered free cash flows of a company and allows the valuation of target companies without the impact of capital structure.

Also, using NOPLAT is beneficial in merger analysis, since the capital structure of target companies is irrelevant, especially if the entire company is being acquired. It should be noted that the nature of some industries involves higher operating costs, so comparing NOPLAT between companies is more meaningful among companies within the same industry.

NOPAT vs. NOPLAT

Net operating profit after tax (NOPAT) and net operating profit less adjusted taxes (NOPLAT) are similar and are easily confused with one another, but they are not exactly the same. NOPAT is equivalent to the after-tax operating profit referred to earlier. It is a measure of profit that excludes tax benefits. NOPAT is commonly used in economic value added (EVA) calculations.

The key difference between the two profitability measures is that NOPLAT includes changes in deferred taxes so that NOPAT is essentially NOPLAT without the deferred taxes. Where deferred taxes are present, NOPLAT uses the actual tax paid to tax authorities and leaves out deferred tax.

Deferred taxes are essentially either taxes owed or overpaid that represent either an asset or liability on a company’s balance sheet. NOPLAT can give a clearer picture of operating earnings than NOPAT, as it adjusts for non-operating tax expenses as well.

In many cases, both NOPAT and NOPLAT may turn out to be very similar for many companies but will differ in companies that incur significant deferred taxes.

To summarize, NOPLAT does not include capital structure impact and adjusts for changes in deferred taxes.

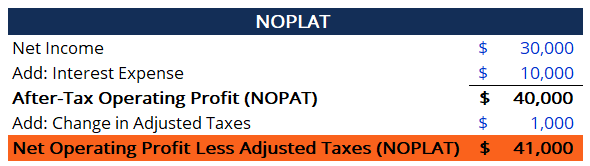

Practical Example

Consider a company with the following income statement:

Find the NOPLAT given the income statement. The calculation is shown below:

In the example above, not all of the tax expenses come as a result of operations. $1,000 of the tax expense is attributed to an increase in deferred taxes. So, the $1,000 was essentially overaccrued taxes.

In calculating NOPAT, the increase in deferred taxes can be ignored. However, when calculating net operating profit less adjusted taxes, the change in deferred taxes must be added to arrive at the correct amount.

From the calculation above, ABC Company realized $41,000 in operating profit in the accounting period, after adjusting for capital structure impact and changes in deferred taxes.

Additional Resources

CFI offers the Commercial Banking & Credit Analyst (CBCA)™ certification program for those looking to take their careers to the next level. To keep learning and developing your knowledge base, please explore the additional relevant resources below:

Analyst Certification FMVA® Program

Below is a break down of subject weightings in the FMVA® financial analyst program. As you can see there is a heavy focus on financial modeling, finance, Excel, business valuation, budgeting/forecasting, PowerPoint presentations, accounting and business strategy.

A well rounded financial analyst possesses all of the above skills!

Additional Questions & Answers

CFI is the global institution behind the financial modeling and valuation analyst FMVA® Designation. CFI is on a mission to enable anyone to be a great financial analyst and have a great career path. In order to help you advance your career, CFI has compiled many resources to assist you along the path.

In order to become a great financial analyst, here are some more questions and answers for you to discover:

- What is Financial Modeling?

- How Do You Build a DCF Model?

- What is Sensitivity Analysis?

- How Do You Value a Business?

Accounting Crash Courses

Learn accounting fundamentals and how to read financial statements with CFI’s online accounting classes.

These courses will give you the confidence to perform world-class financial analyst work. Start now!

Boost your confidence and master accounting skills effortlessly with CFI’s expert-led courses! Choose CFI for unparalleled industry expertise and hands-on learning that prepares you for real-world success.