Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

Learn about the similarities and differences between ROIC and ROCE

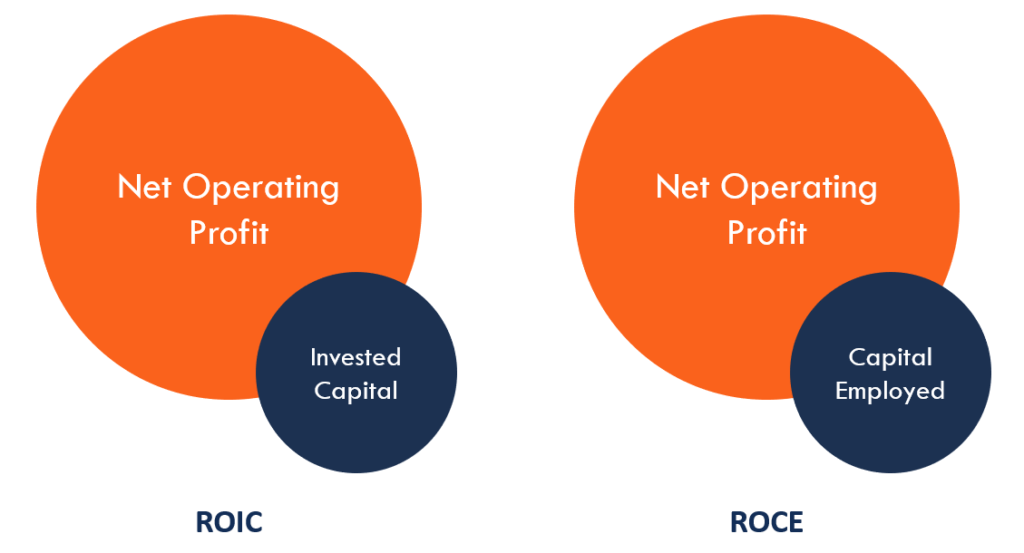

Understanding financial ratios such as ROCE vs ROIC is important to investors in determining the viability of an investment. ROIC is the net operating income divided by invested capital. ROCE, on the other hand, is the net operating income divided by the capital employed.

The two ratios come with identical numerators in their formulae, which infers that the denominator is what differentiates their values. ROIC uses invested capital as the denominator, while ROCE uses capital employed as the denominator.

Invested capital is the amount of capital that is circulating in the business while capital employed is the total capital it has. Invested capital is, therefore, a subset of capital employed. Capital employed includes every aspect of capital in the entity, such as debts and shareholders’ capital. Invested capital includes the active capital in circulation, and it excludes non-active assets, especially those outside the business, such as securities held in other companies.

ROIC is an abbreviation for Return on Invested Capital. ROIC is a profitability ratio that measures the returns that investors earn from the capital they’ve invested in a company. It shows how efficiently the company is using the funds provided by the investors to generate income for the business.

The invested capital is a subset of employed capital, and it is the percentage of capital that is actively invested in the business. ROIC is calculated by obtaining the Net Profit After Tax (Net income – Dividends) divided by invested capital.

ROCE stands for Return on Capital Employed. ROCE is a profitability ratio that calculates the profits that a business can generate using the capital employed. ROCE is calculated by dividing earnings before interest and tax (EBIT) by the capital employed.

When a company’s ROCE is higher than the cost of capital, it means that the company has utilized the capital in an efficient manner to generate profits. Companies should strive to achieve an ever-increasing ROCE over the years since it indicates that the business is stable and is an attractive investment option for investors.

ROCE and ROIC are used by investors to analyze profitable companies for investment. Both ratios inform investors how a company is performing and how much of the net reported profits are returned to investors as dividends. The ratios also inform the investors how the company uses its invested capital, as well as its ability to generate additional revenues in the future.

ROCE is based on capital employed, which is broader than invested capital on which ROIC is anchored. Therefore, the scope of ROCE is more extensive than ROIC, since the former considers the total capital employed, which is a total of debt and equity financing less short-term liabilities. ROIC is more refined, and it calculates the return of a company according to the capital that is actively circulating in the business.

A company is said to be profitable or utilizing the capital effectively if the ROCE is greater than the cost of capital. In the case of ROIC, a company can be described as profitable if the ROIC value is greater than zero. When ROCE is below the cost of capital or the ROIC is negative, it shows that the company has not used invested capital effectively.

Another key difference between ROIC and ROCE is that ROCE is based on pre-tax figures while ROIC is based on after-tax figures. Thus, ROCE is more relevant from the company’s perspective, while ROIC is more relevant from the investor’s perspective because it gives them an indication of what they are likely to get as dividends. ROCE becomes most suitable for use in comparison purposes between companies in different countries or tax systems. ROIC, nonetheless, can be used in comparison for companies under similar tax regimes for easy inferences.

Making investment decisions is a rigorous process that requires investors to make various considerations before making the final decision. Key profitability ratios such as ROIC and ROCE help determine the viability of an investment based on the profitability of the company and the proper use of invested capital to grow the business.

ROIC vs ROCE shows the ratio of the returns compared to the amount of capital applied, hence giving the investor an outlook of the profitability of a venture beforehand. Investors get an overview of the profitability, management, and future prospects of the business. The ratios can also help in the comparison between different ventures to determine the venture with the highest returns possible.

Connect what you just learned to a clear career path with CFI’s role‑based courses and certification programs.

Thank you for reading CFI’s guide on ROIC vs ROCE. To keep learning and developing your knowledge of financial analysis, we highly recommend the additional CFI resources below: