Loan Life Coverage Ratio (LLCR)

The net present value of available cash divided by the total debt outstanding

What is the Loan Life Coverage Ratio (LLCR)?

The Loan Life Coverage Ratio (LLCR) is a metric used to gauge the ability of a project to completely cover its debt obligations. The LLCR is a very commonly used ratio to assess the potential risks of projects in project finance. This coverage ratio can be taken at any point in time of the project. It can be calculated by taking the net present value of all cash flow available for debt service (CFADS) up until the time of debt maturity and dividing it by the total outstanding debt at this given point in time.

Summary

The Loan Life Coverage Ratio (LLRC) is a commonly used metric in project finance.

- The LLRC is used to gauge a project’s ability to pay the total debt outstanding at a given point in time.

- The ratio is calculated by taking the net present value of cash flow available for debt service and dividing it by the total outstanding debt at the chosen time.

Why is the Loan Life Coverage Ratio (LLCR) Important?

Similar to the debt service coverage ratio (DSCR), the LLCR is an important ratio used in project finance. In any project finance undertaking, calculating both ratios is a standard step in assessing the project. However, unlike the DSCR, which measures the project’s ability to pay debt period-on-period, the LLCR takes into account multiple periods of cash flow available for debt service, as well as the entire amount of debt outstanding.

LLCR assesses the project’s ability to pay off all debt obligations based on the discounted projected cash flows. It gives a better estimation of the risk profile of the project as a whole.

How Do You Calculate the Loan Life Coverage Ratio (LLCR)?

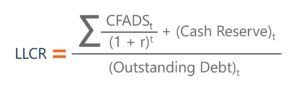

The loan life coverage ratio is calculated by taking the net present value of cash flow available for debt service and adding any available cash in the cash reserve. We then take the number and divide it by the total outstanding debt in the given time.

The LLCR can be calculated at any time; however, the remaining CFADS must be discounted to the chosen point in time. The total outstanding debt used in the calculation must also correspond to this point in time.

Following is the equation for calculating the LLCR:

When calculating the LLCR, the ratio is generally calculated either annually, semi-annually, or quarterly over the remaining lifetime of the loan.

Loan Life Coverage Ratio (LLCR) – Worked Example

Let us take a look at a simple loan life coverage ratio example question. Shown below is the hypothetical cash available for debt service over the period of a project. The projected cash flows are discounted to a specific period in time each year and then totaled. The number divided by the total debt outstanding at the given time gives the LLCR.

If you would like to learn more about financial modeling, check out CFI’s Financial Modeling Courses.

Additional Resources

CFI is the official provider of the Financial Modeling and Valuation Analyst (FMVA)® certification program, designed to transform anyone into a world-class financial analyst.

In order to help you become a world-class financial analyst and advance your career to your fullest potential, these additional resources will be very helpful:

Analyst Certification FMVA® Program

Below is a break down of subject weightings in the FMVA® financial analyst program. As you can see there is a heavy focus on financial modeling, finance, Excel, business valuation, budgeting/forecasting, PowerPoint presentations, accounting and business strategy.

A well rounded financial analyst possesses all of the above skills!

Additional Questions & Answers

CFI is the global institution behind the financial modeling and valuation analyst FMVA® Designation. CFI is on a mission to enable anyone to be a great financial analyst and have a great career path. In order to help you advance your career, CFI has compiled many resources to assist you along the path.

In order to become a great financial analyst, here are some more questions and answers for you to discover:

- What is Financial Modeling?

- How Do You Build a DCF Model?

- What is Sensitivity Analysis?

- How Do You Value a Business?