Get Certified for

Commercial Banking (CBCA®)

Stand out and gain a competitive edge as a commercial banker, loan officer, or credit analyst with advanced knowledge, real-world analysis skills, and career confidence.

CFADS is the cash flow available to pay debt obligations

Cash Flow Available for Debt Service (CFADS), also commonly referred to as cash available for debt service (CADS), is the amount of cash available to service debt obligations. It takes into account several cash inflows and outflows to give an accurate representation of a project’s ability to generate cash flows and service debt. Financial analysts will often determine CFADS to use as one of the most important metrics in project finance models.

CFADS is an important metric and acts as a highly accurate gauge of a project’s ability to take on debt and pay it off. CFADS can replace EBITDA and can be used as a component of key financial ratios such as the debt service coverage ratio (DSCR), the loan life coverage ratio (LLCR), and the project life coverage ratio (PLCR). Together, the three coverage ratios determine a project’s ability to cover debt over both the period of the project and over the entire lifetime of a project.

Determining CFADS is especially important in project finance, where predicted cash flows must be as accurate as possible. In corporate finance, a commonly referenced ratio to measure the ability to service debt is the times-interest-earned ratio. The metric, however, uses EBIT as an estimate of cash flow, making this ratio less accurate to use than a coverage ratio that uses CFADS.

Cash flows available for debt service are a better indicator of a project’s ability to repay debt because they take into account the timing of cash flows and the effects of taxes.

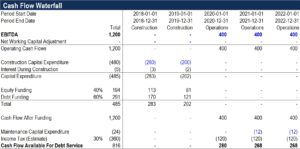

CFADS can be calculated in more than one way. One way in which it is calculated is in a cash flow waterfall model. The cash flow waterfall can start with revenue or EBITDA and will net out all cash outflows and inflows in the order that they occur. They can include items such as operating revenues, operating expenses, capital expenditures, taxes, and funding. Alternatively, you can start with receipts from customers and net this against any outflows to arrive at CFADS.

The following shows two common ways to calculate CFADS:

As mentioned before, CFADS is often calculated using a cash flow waterfall model. The waterfall model is important in determining an accurate amount of cash flow available for debt servicing. From there, CFADS can be further analyzed in the waterfall model and broken down into cash flow available for senior debt, junior debt, and equity.

After calculating CFADS, it can be graphed against interest and principal repayments to determine if there is sufficient cash flow available to pay this debt obligation. CFADS can also be input into several coverage ratios and used to analyze the project. Assessing a coverage ratio, such as the debt service coverage ratio, over a period of time can give insight as to whether there is enough cash to settle debt obligations in each period of the project.

The following shows an example of how CFADS might be calculated using a cash flow waterfall model starting with EBITDA:

If you would like to learn more about financial modeling, check out CFI’s Financial Modeling Courses.

Connect what you just learned to a clear career path with CFI’s role‑based courses and certification programs.

CFI offers the Commercial Banking & Credit Analyst (CBCA®) certification program for those looking to take their careers to the next level. To keep learning and developing your knowledge base, please explore the additional relevant resources below