Get Certified for

Commercial Banking (CBCA®)

Stand out and gain a competitive edge as a commercial banker, loan officer, or credit analyst with advanced knowledge, real-world analysis skills, and career confidence.

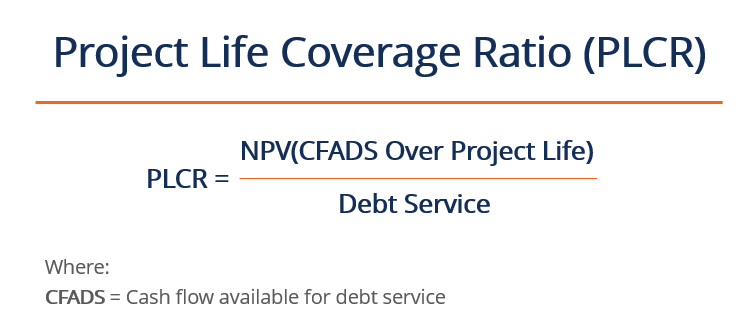

A financial ratio used to determine the repayment ability of a project’s cash flows to its debt obligations

The project life coverage ratio (PLCR) refers to a financial ratio that is used to determine the repayment ability of a project’s cash flows to its debt obligations. Lenders set a minimum PLCR to constrain the borrower’s maximum loan amount, thus reducing the risk of default.

In project finance deals, the project life coverage ratio constrains the borrower’s maximum debt service (loan amount) based on the project’s expected cash flows. It ensures the borrower’s ability to pay back the debt. The PLCR is one of many ratios used by lenders; other ratios include the debt service coverage ratio (DSCR) and the loan life coverage ratio (LLCR).

The first component to examine in the PLCR is the net present value (NPV). The NPV essentially sums up all future cash flows available to service the debt discounted by the cost of debt. By doing so, it takes into account the time value of money and is a useful tool for determining the profitability of a project.

With the NPV calculated, the next step is to divide it by the debt service amount. Note that the cash flow available for debt service refers to cash flows that the borrower is able to repay debt with.

The project life coverage ratio represents how many times the borrower can repay the debt over the life of the project. A PLCR of 1 means that the cash flow available is just enough to cover the debt service.

However, the minimum required PLCR is always more than 1 because lenders require a cushion to ensure the borrower’s ability to repay debt. The cushion is important because the actual project cash flows may fall short of the predicted cash flows, causing the numerator to decrease.

If the PLCR falls below 1, then the borrower will not have enough cash to repay the debt. Therefore, the higher the PLCR, the less likely the borrower will default on the debt.

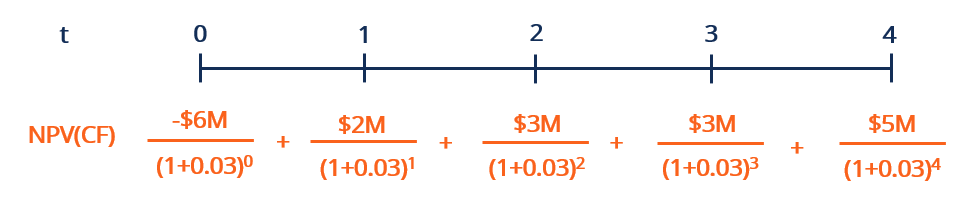

Consider the following example: a project manager is seeking funding for his upcoming project. His estimated cash flows are illustrated in the diagram above. The project requires an initial investment of $6M, with positive cash flow every year until it wraps up in Year 4.

The project manager finds a lender with the following terms:

Based on the project cash flows, how much can the project manager borrow?

In this example, we are looking to find the maximum debt service the project manager can take out given his project. First, we must determine the NPV(CFADS over the project life). Assuming that the project is the manager’s only source of cash, it means that his CFADS is all from the project’s future cash flows.

Using the NPV formula, we discount the project’s cash flows to present value. The sum of the discounted cash flows equals $5.78M.

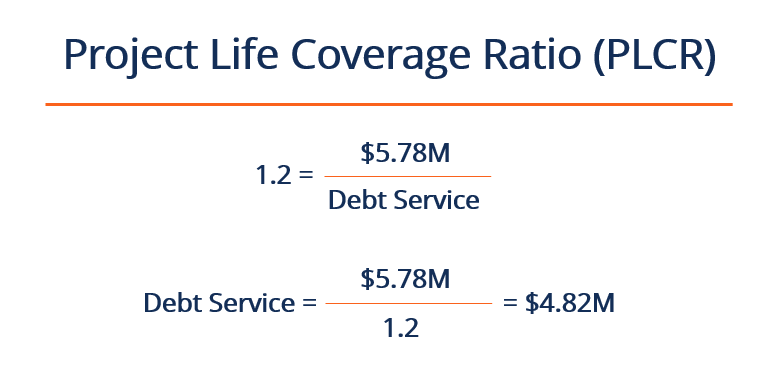

Next, we determine the maximum debt service by rearranging the PLCR formula. Given that the minimum required PLCR is 1.2, the largest debt service that the project manager can take out with the net present value of the project’s cash flows is $4.82M.

The difference between the initial investment of $6M and the maximum debt service of $4.82M is up to the manager to obtain through equity.

CFI is the official provider of the global Certified Banking & Credit Analyst (CBCA)® certification program, designed to help anyone become a world-class financial analyst. To keep advancing your career, the additional CFI resources below will be useful:

Learn accounting fundamentals and how to read financial statements with CFI’s online accounting classes.

These courses will give you the confidence to perform world-class financial analyst work. Start now!

Boost your confidence and master accounting skills effortlessly with CFI’s expert-led courses! Choose CFI for unparalleled industry expertise and hands-on learning that prepares you for real-world success.