Get Certified for

Commercial Banking (CBCA®)

Stand out and gain a competitive edge as a commercial banker, loan officer, or credit analyst with advanced knowledge, real-world analysis skills, and career confidence.

A reserve account used to pay debt

The Debt Service Reserve Account (DSRA), which is a component of a debt service fund, is a reserve account used to pay interest and principal amounts of debt. The DSRA is very important when the cash flow available for debt services (CFADS) is below the necessary amount to make the payments.

In the case of a credit agreement, the lender will more than likely impose a clause that requires a DSRA, with a balance that must be periodically restored to a minimum amount. The minimum amount is often contingent on the amount of interest and principal remaining.

The Debt Service Reserve Account acts as a safety measure to ensure that the necessary payments to lenders can be met. It is an important part of project financing and is commonly used to ensure the borrower gets the flexibility to resolve problems or restructure their debt during times where the debt service coverage ratio is below 1. The DSRA can be very important to lenders who are worried about borrowers defaulting on payments.

The Debt Service Reserve Account commonly exists in project finance. It is especially true for non-recourse project financing, where the lender is only entitled to repayments of profits from the funded project. The DSRA is often created once the loan becomes repayable, such as after the construction of a project.

If the project’s cash flows available for debt servicing are not enough to meet the debt obligations, the debt service reserve account is credited. Often, within the credit agreement, the debt service account is required by the borrower for the benefit of the agent.

The DSRA target balance can be determined in several ways and accounts for both interest and principal payments. In general, the DSRA must maintain a required minimum balance and will be restored in accordance with the terms of the credit agreement.

The funding method can be set as periodic intervals dependent on the debt servicing time span, or it can be a fixed amount on a set date. You can generally find the funding method stated in the project term sheet.

Examples of different clauses within a credit agreement pertaining to the DSRA follow:

Note: The example clauses above are only for educational purposes and should not be used for any other purpose.

The DSRA and funding method are important to consider when creating a financial model for a project. The funding of the DSRA, as well as the use of this reserve account, will affect cash inflows and outflows.

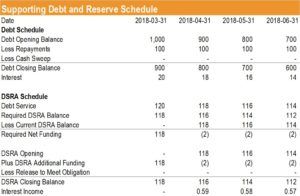

Building out a debt and reserve schedule can be very useful in determining how the DSRA will affect the cash flows of a project. Following is an example of a debt and reserve schedule:

If you would like to learn more about financial modeling, check out CFI’s Financial Modeling Courses.

Connect what you just learned to a clear career path with CFI’s role‑based courses and certification programs.

CFI is the official provider of the global Commercial Banking & Credit Analyst (CBCA®) certification program, designed to help anyone become a world-class financial analyst. To keep advancing your career, the additional resources below will be useful: