Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

The net income of a company relative to the value of its equity

Return on Equity (ROE) is the measure of a company’s annual return (net income) divided by the value of its total shareholders’ equity, expressed as a percentage (e.g., 12%). Alternatively, ROE can also be derived by dividing the firm’s dividend growth rate by its earnings retention rate (1 – dividend payout ratio).

Return on Equity is a two-part ratio in its derivation because it brings together the income statement and the balance sheet, where net income or profit is compared to the shareholders’ equity. The number represents the total return on equity capital and shows the firm’s ability to turn equity investments into profits. To put it another way, it measures the profits made for each dollar from shareholders’ equity.

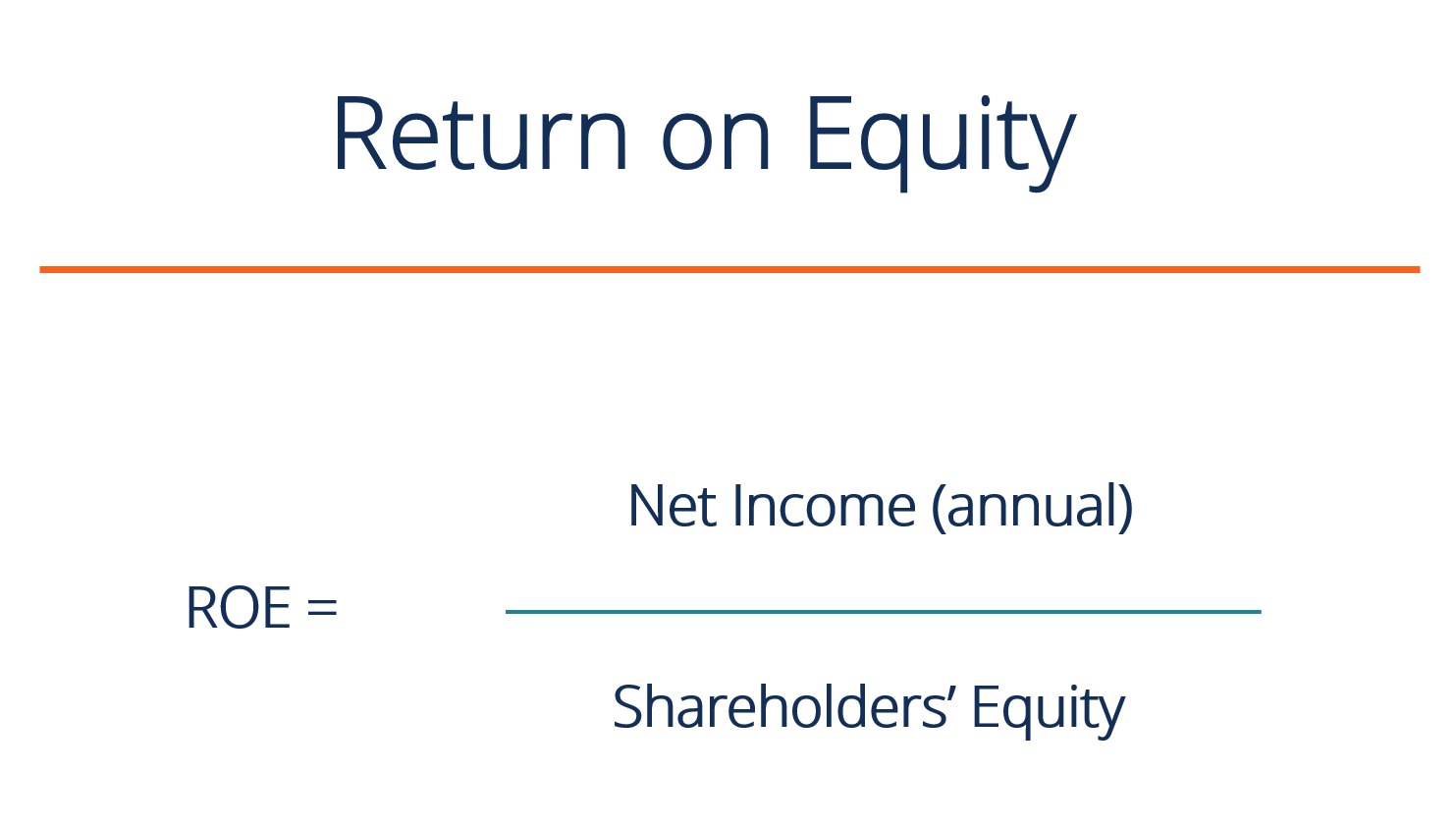

The following is the ROE equation:

ROE = Net Income / Shareholders’ Equity

ROE provides a simple metric for evaluating investment returns. By comparing a company’s ROE to the industry’s average, something may be pinpointed about the company’s competitive advantage. ROE may also provide insight into how the company management is using financing from equity to grow the business.

A sustainable and increasing ROE over time can mean a company is good at generating shareholder value because it knows how to reinvest its earnings wisely, so as to increase productivity and profits. In contrast, a declining ROE can mean that management is making poor decisions on reinvesting capital in unproductive assets.

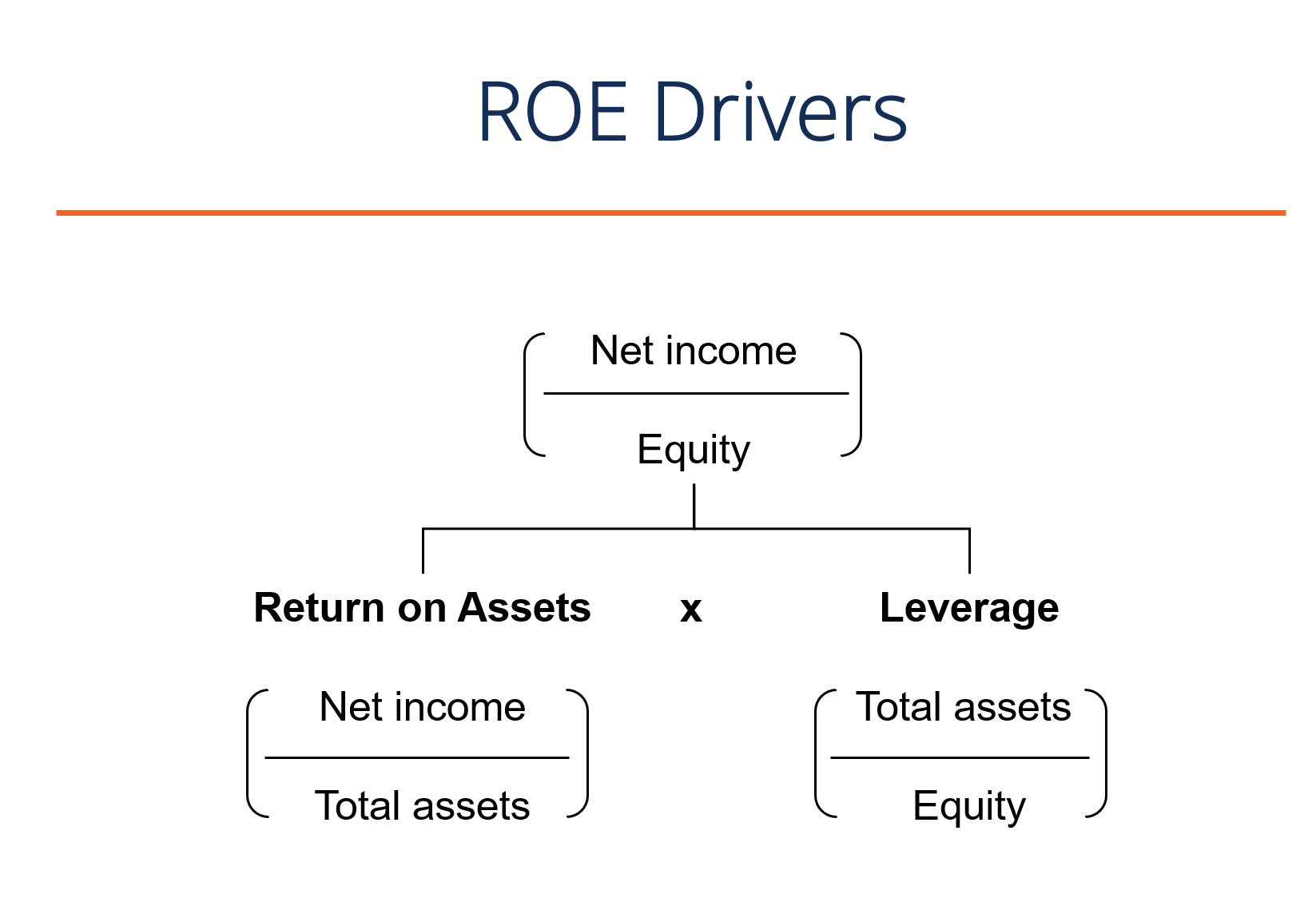

While the simple return on equity formula is net income divided by shareholder’s equity, we can break it down further into additional drivers. As you can see in the diagram below, the return on equity formula is also a function of a firm’s return on assets (ROA) and the amount of financial leverage it has. Both of these concepts will be discussed in more detail below.

Learn more in CFI’s Financial Analysis Fundamentals Course.

With net income in the numerator, Return on Equity (ROE) looks at the firm’s bottom line to gauge overall profitability for the firm’s owners and investors. Stockholders are at the bottom of the pecking order of a firm’s capital structure, and the income returned to them is a useful measure that represents excess profits that remain after paying mandatory obligations and reinvesting in the business.

Simply put, with ROE, investors can see if they’re getting a good return on their money, while a company can evaluate how efficiently they’re utilizing the firm’s equity. ROE must be compared to the historical ROE of the company and to the industry’s ROE average – it means little if merely looked at in isolation. Other financial ratios can be looked at to get a more complete and informed picture of the company for evaluation purposes.

In order to satisfy investors, a company should be able to generate a higher ROE than the return available from a lower risk investment.

A high ROE could mean a company is more successful in generating profit internally. However, it doesn’t fully show the risk associated with that return. A company may rely heavily on debt to generate a higher net profit, thereby boosting the ROE higher.

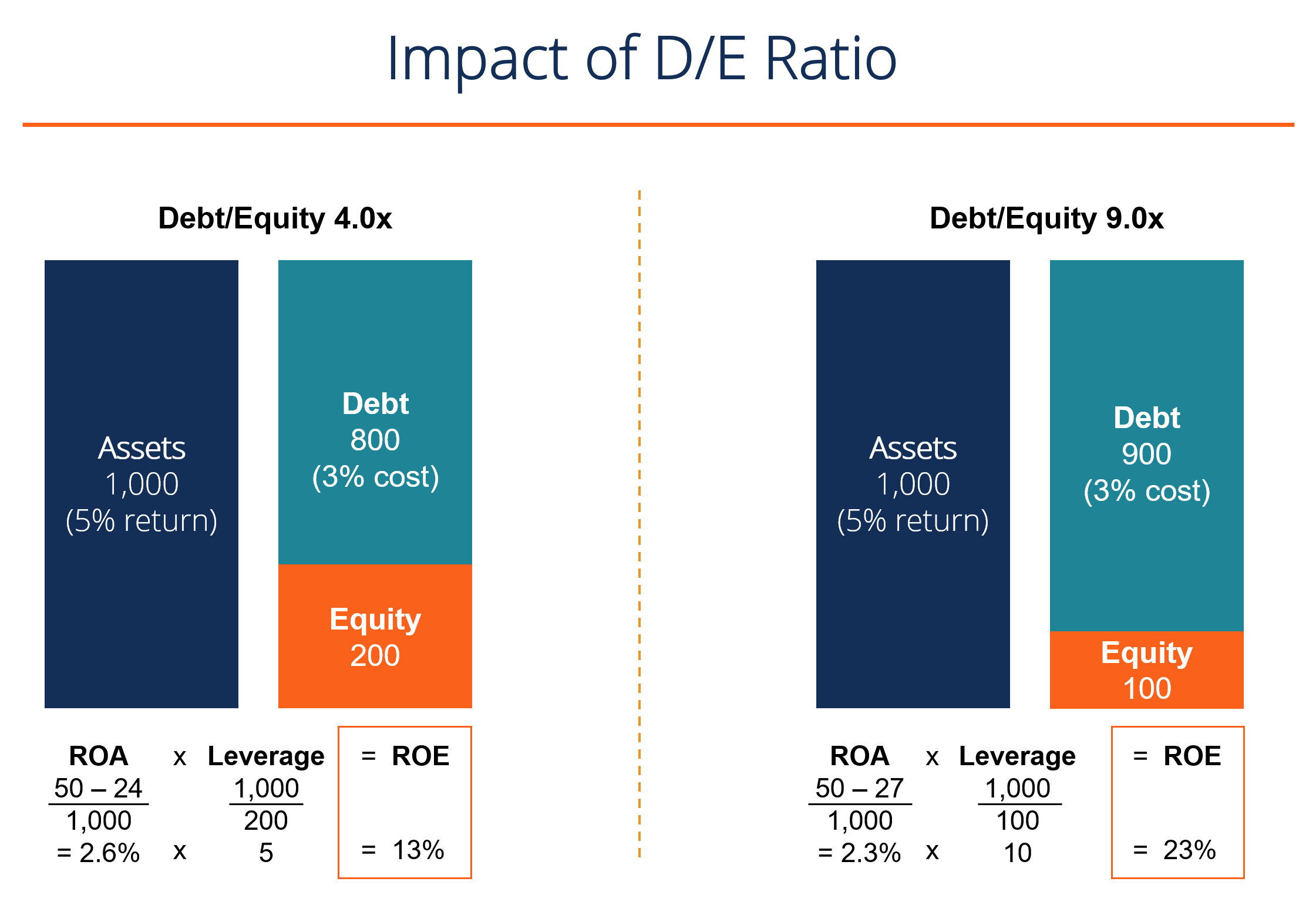

As an example, if a company has $150,000 in equity and $850,000 in debt, then the total capital employed is $1,000,000. This is the same number of total assets employed. At 5%, it will cost $42,000 to service that debt, annually.

If the company manages to increase its profits before interest to a 12% return on capital employed (ROCE), the remaining profit after paying the interest is $78,000, which will increase equity by more than 50%, assuming the profit generated gets reinvested back. As we can see, the effect of debt is to magnify the return on equity.

The image below from CFI’s Financial Analysis Course shows how leverage increases equity returns.

Learn more in CFI’s Financial Analysis Fundamentals Course.

The return on equity ratio can also be skewed by share buybacks. When management repurchases its shares from the marketplace, this reduces the number of outstanding shares. Thus, ROE increases as the denominator shrinks.

Another weakness is that some ROE ratios may exclude intangible assets from shareholders’ equity. Intangible assets are non-monetary items such as goodwill, trademarks, copyrights, and patents. This can make calculations misleading and difficult to compare to other firms that have chosen to include intangible assets.

Finally, the ratio includes some variations on its composition, and there may be some disagreements between analysts. For example, the shareholders’ equity can either be the beginning number, ending number, or the average of the two, while Net Income may be substituted for EBITDA and EBIT, and can be adjusted or not for non-recurring items.

Some industries tend to achieve higher ROEs than others, and therefore, ROE is most useful when comparing companies within the same industry. Cyclical industries tend to generate higher ROEs than defensive industries, which is due to the different risk characteristics attributable to them. A riskier firm will have a higher cost of capital and a higher cost of equity.

Furthermore, it is useful to compare a firm’s ROE to its cost of equity. A firm that has earned a return on equity higher than its cost of equity has added value. The stock of a firm with a 20% ROE will generally cost twice as much as one with a 10% ROE (all else being equal).

The DuPont formula breaks down ROE into three key components, all of which are helpful when thinking about a firm’s profitability. ROE is equal to the product of a firm’s net profit margin, asset turnover, and financial leverage:

If the net profit margin increases over time, then the firm is managing its operating and financial expenses well and the ROE should also increase over time. If the asset turnover increases, the firm is utilizing its assets efficiently, generating more sales per dollar of assets owned.

Lastly, if the firm’s financial leverage increases, the firm can deploy the debt capital to magnify returns. DuPont analysis is covered in detail in CFI’s Financial Analysis Fundamentals Course.

Below is a video explanation of the various drivers that contribute to a firm’s return on equity. Learn how the formula works in this short tutorial, or check out the full Financial Analysis Course!

While debt financing can be used to boost ROE, it is important to keep in mind that overleveraging has a negative impact in the form of high interest payments and increased risk of default. The market may demand a higher cost of equity, putting pressure on the firm’s valuation. While debt typically carries a lower cost than equity and offers the benefit of tax shields, the most value is created when a firm finds its optimal capital structure that balances the risks and rewards of financial leverage.

Furthermore, it is important to keep in mind that ROE is a ratio, and the firm can take actions such as asset write-downs and share repurchases to artificially boost ROE by decreasing total shareholders’ equity (the denominator).

Connect what you just learned to a clear career path with CFI’s role‑based courses and certification programs.

This has been CFI’s guide to return on equity, the return on equity formula, and the pros and cons of this financial metric. To keep learning and expanding your financial analyst skills, see these additional valuable CFI resources:

Below is a break down of subject weightings in the FMVA® financial analyst program. As you can see there is a heavy focus on financial modeling, finance, Excel, business valuation, budgeting/forecasting, PowerPoint presentations, accounting and business strategy.

A well rounded financial analyst possesses all of the above skills!

CFI is the global institution behind the financial modeling and valuation analyst FMVA® Designation. CFI is on a mission to enable anyone to be a great financial analyst and have a great career path. In order to help you advance your career, CFI has compiled many resources to assist you along the path.

In order to become a great financial analyst, here are some more questions and answers for you to discover: