Get In-Demand Finance Certifications

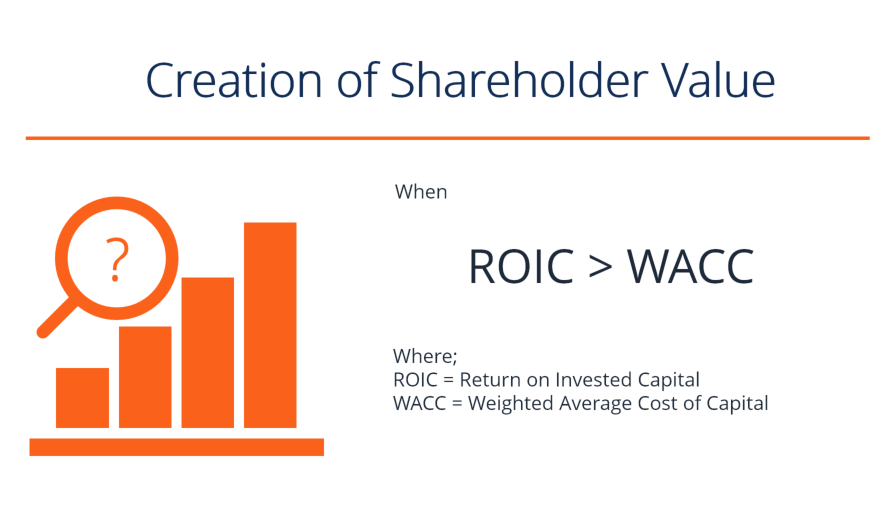

Value is created when ROIC > WACC

Shareholder value is the financial worth owners of a business receive for owning shares in the company. An increase in shareholder value is created when a company earns a return on invested capital (ROIC) that is greater than its weighted average cost of capital (WACC). Put more simply, value is created for shareholders when the business increases profits.

Since the value of a company and its shares are based on the net present value of all future cash flows, that value can be increased or decreased by changes in cash flow and changes in the discount rate. Since the company has little influence over discount rates, its managers focus on investing capital effectively to generate more cash flow with less risk.

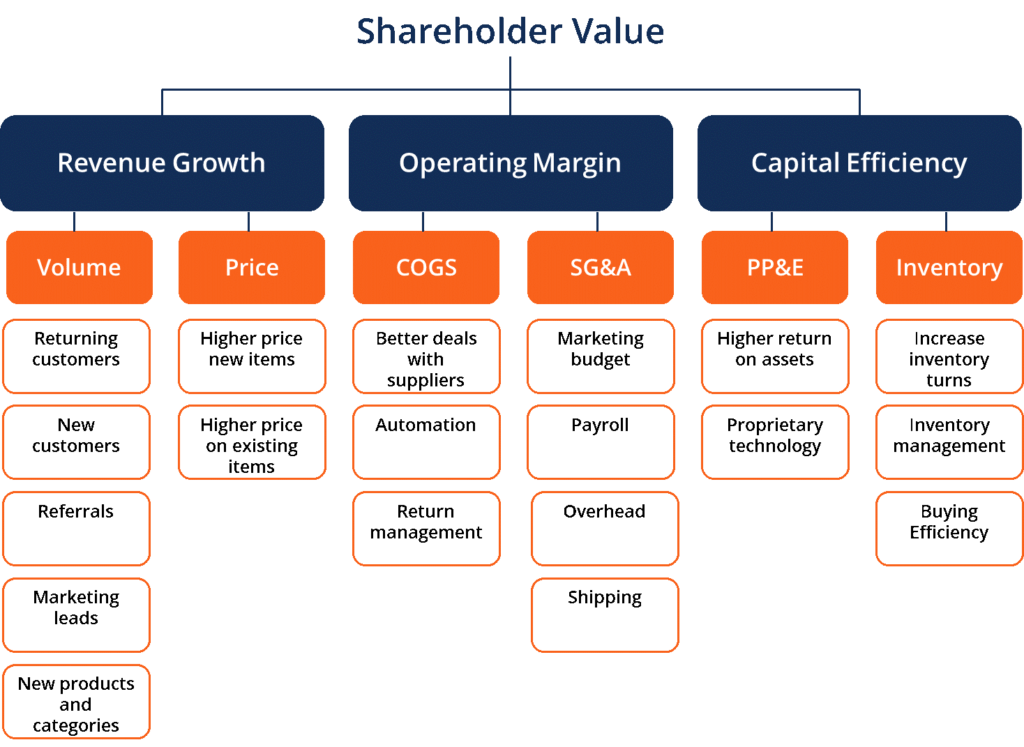

In order to maximize shareholder value, there are three main strategies for driving profitability in a company: (1) revenue growth, (2) increasing operating margin, and (3) increasing capital efficiency. We will discuss in the following sections the major factors in boosting each of the three measures.

For any goods and services businesses, sales revenue can be improved through the strategies of sales volume increase or sales price inflation.

Increasing Sales Volume

A company would want to retain its current customers and keep them away from competitors to maintain its market share. It should also attract new customers through referrals from existing customers, marketing and promotions, new products and services offerings, and new revenue streams.

Raising Sales Price

A company may increase current product prices as a one-time strategy or gradual price increases throughout several months, quarters, or years to achieve revenue growth. It can also offer new products with advanced qualities and features and price them at higher ranges.

Ideally, a business can combine both higher volume and higher prices to significantly increase revenue.

Besides maximizing sales, a business must identify feasible approaches to cost reductions leading to optimal operating margins. While a company should strive to reduce all its expenses, COGS (Cost of Goods Sold) and SG&A (Selling, General, and Administrative) expenses are usually the largest categories that need to be efficiently managed and minimized.

Cost of Goods Sold (COGS)

When a company builds a good relationship with its suppliers, it can possibly negotiate with suppliers to reduce material prices or receive discounts on large orders. It may also form a long-term agreement with the suppliers to secure its material source and pricing.

Many companies use automation in their manufacturing processes to increase efficiency in production. Automation not only reduces labor and material costs, but also improves the quality and precision of the products and, thus, largely reduces defective and return rates.

Return management is the process by which activities associated with returns and reverse logistics are managed. It is an important factor in cost reduction because a good return management process helps the company manage the product flow efficiently and identify ways to reduce undesired returns by customers.

Selling, General, and Administrative (SG&A) Expenses

SG&A is usually one of the largest expenses in a company. Therefore, being able to minimize them will help the company achieve an optimal operating margin. The company should tightly control its marketing budget when planning for next year’s spending. It should also carefully manage its payroll and overhead expenses by evaluating them periodically and cutting down on unnecessary labor and other costs.

Shipping cost is directly associated with product sales and returns. Therefore, good return management will help reduce the cost of goods sold as well as logistics costs.

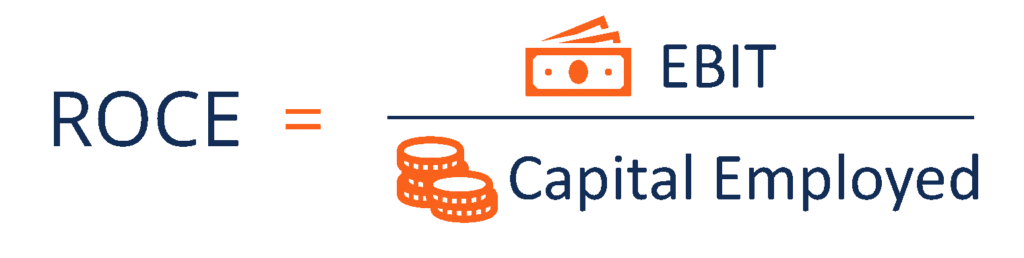

Capital efficiency is the ratio between dollar expenses incurred by a company and dollars that are spent to make a product or service, which can be referred to as ROCE (Return on Capital Employed) or the ratio between EBIT (Earnings Before Interest and Tax) over Capital Employed. Capital efficiency reflects how efficiently a company is deploying its cash in its operations.

Capital employed is the total amount of capital a company uses to generate profit, which can be simplified as total assets minus current liabilities. A higher ROCE indicates a more efficient use of capital to generate shareholder value, and it should be higher than the company’s capital cost.

Property, Plant, and Equipment (PP&E)

To achieve high capital efficiency, a company would first want to achieve a high return on assets (ROA), which measures the company’s net income generated by its total assets.

Over time, the company might also shift to developing proprietary technology, which is a system, application, or tool owned by a company that provides a competitive advantage to the owner. The company can then profit from utilizing this asset or licensing the technology to other companies. Proprietary technology is an optimal asset to possess because it increases capital efficiency to a great extent.

Inventory

Inventory is often a major component of a company’s total assets, and a company would always want to increase its inventory turnover, which equals net sales divided by average inventory. A higher inventory turnover ratio means that more revenues are generated given the amount of inventory. Increasing inventory turnover also reduces holding costs, consisting of storage space rent, utilities, theft, and other expenses. It can be achieved by effective inventory management, which involves constant monitoring and controlling of inventory orders, stocks, returns, or obsolete items in the warehouse.

Inventory buying efficiency can be greatly improved by using the Just-in-time (JIT) system. Costs are only incurred when the inventory goes out and new orders are being placed, which allows companies to minimize costs associated with keeping and discarding excess inventory.

There are many factors that influence shareholder value and it can be very difficult to accurately attribute the causes in its rise or fall.

Managers of businesses constantly speak of “generating shareholder value” but it is often more of a soundbite than an actual practice. Due to a host of complications, including executive compensation incentives and principal-agent issues, the primacy of shareholder value can sometimes be called into question.

Businesses are influenced by many outside forces, and thus the impact of management vs external factors can be very hard to measure.

Read more from Harvard about strategies for creating shareholder value.

Connect what you just learned to a clear career path with CFI’s role‑based courses and certification programs.

Thank you for reading CFI’s explanation of Shareholder Value. To continue learning and advancing your career, the additional CFI resources below will be helpful: