Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

How to make a "comps table"

Comparable company analysis (or “comps” for short) is a valuation methodology that looks at ratios of similar public companies and uses them to derive the value of another business. Comps is a relative form of valuation, unlike a discounted cash flow (DCF) analysis, which is an intrinsic form of valuation.

In this guide, we will break down all the steps necessary to perform comparable company analysis, as required in most financial analyst jobs.

In the next section of this guide, we will go through a detailed list of how to build your own comps table. This type of work will be routine for anyone working as an analyst in investment banking, equity research, corporate development, or private equity.

This is the first and probably the hardest (or most subjective) step in performing a ratio analysis of public companies. The very first thing an analyst should do is look up the company you are trying to value on CapIQ or Bloomberg so you can get a detailed description and industry classification of the business.

The next step is to search either of those databases for companies that operate in the same industry and that have similar characteristics. The closer the match, the better.

The analyst will run a screen based on criteria that include:

To learn more about this process, see CFI’s Business Valuation Course.

Once you’ve found the list of companies that you feel are most relevant to the company you’re trying to value, it’s time to gather their financial information.

Once again, you will probably be working with Bloomberg Terminal or Capital IQ and you can easily use either of them to import financial information directly into Excel.

The information you need will vary widely by industry and the company’s stage in the business lifecycle. For mature businesses, you will look at metrics like EBITDA and EPS, but for earlier stage companies you may look at Gross Profit or Revenue.

If you don’t have access to an expensive tool like Bloomberg or Capital IQ you can manually gather this information from annual and quarterly reports, but it will be much more time-consuming.

Learn more: list of Bloomberg functions.

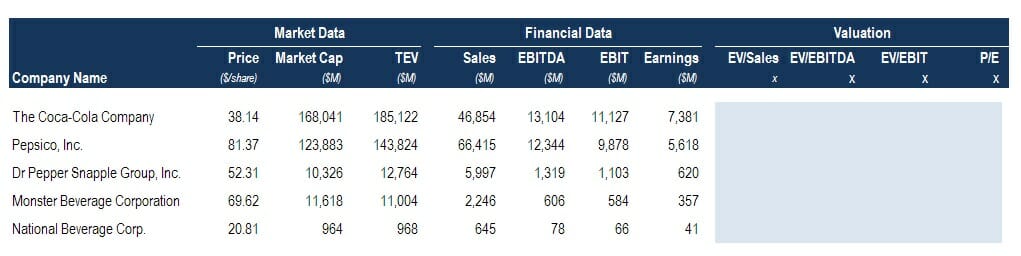

In Excel, you now need to create a table that lists all the relevant information about the companies you’re going to analyze.

The main information in comparable company analysis includes:

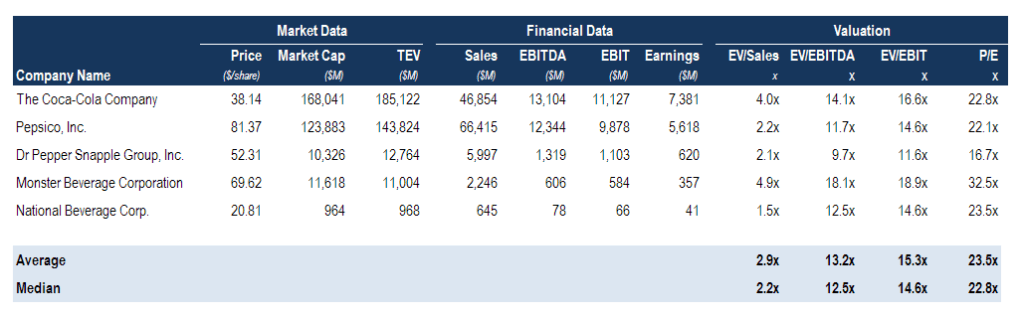

The above information can be organized as shown in our example comparable companies analysis shown below.

To learn more about this process, see our Business Valuation Course.

With a combination of historical financials and analyst estimates populated in the comps table, it’s time to start calculating the various ratios that will be used to value the company in question.

The main ratios included in a comparable company analysis are:

Analysts will typically take the average or median of the comparable companies’ multiples and then apply them to the revenue, gross profit, EBITDA, net income, or whatever metrics they included in the comps table.

In order to come up with a meaningful average, they often remove or exclude outliers and continually massage the numbers until they seem relevant and realistic.

For example, if the average P/E ratio of the group of comparable companies is 12.5 times, then the analyst will multiply the earnings of the company they are trying to value by 12.5 times to arrive at their equity value.

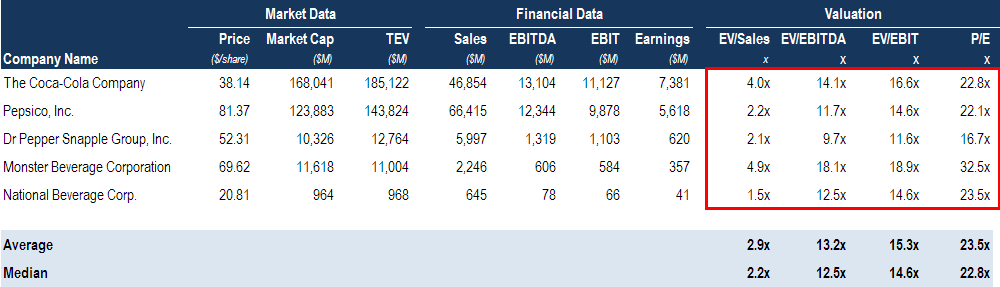

For a good financial analyst, formatting matters a lot! In the tables shown above, you can see what type of formatting is recommended.

It’s important to clearly separate market data, financial data, and the multiples into separate sections, so the reader can easily follow the information.

Multiples should have an “x” next to them (which we explain how to do in our free Excel Crash Course) and should be to one decimal place.

The average or median section should be clearly separated at the bottom of the table and indicate if any adjustments have been made.

Once the numbers are complete and the comps table is finalized, it’s time to start interpreting the results. One way to use the information is to look for companies that are overvalued or undervalued. Comps can help you uncover the opportunities, but the results need to be interpreted carefully as they don’t include any qualitative factors whatsoever.

To properly evaluate the numbers in the comps table you have to understand why numbers are what they are. Why does Company A trade at a discounted EV/EBITDA multiple to Company B?

Is it because it’s undervalued and a good buying opportunity?

Or, is it because it has a much lower growth rate and requires more CapEx spending?

Even though Company A trades at a lower multiple, it might actually be “more expensive” than Company B!

This is where the art of being a great financial analyst comes into play.

Complete the form below to download CFI’s free Comparable Company Analysis template!

There are many uses for comps (or comparable companies analysis, or market multiples, or whatever name you use for them). Typically performed by financial analysts and associates, the most common uses include:

Multiples play a significant role in financial modeling. They are commonly used as the terminal value assumption in a Discounted Cash Flow (DCF) model, with the most common assumption being an EV/EBITDA multiple based on currently observable prices in the market.

Multiples can also be used to tie the results of the financial model back to reality. If the result that comes out of the financial model implies a 30x EV/EBITDA multiple, and none of the comps are currently trading about 12x, the model may require some adjusting.

For more on the art of financial modeling, please check out CFI’s wide range of financial modeling courses.

Thank you for reading CFI’s guide to Comparable Company Analysis. At CFI, we’re on a mission to help you advance your career. Some of our most popular free resources include: